On March 23, 2009, the Treasury Department (Treasury) announced the long awaited details of the Public-Private Investment Program, the prong of the new Administration's Financial Stability Plan designed to address "legacy" assets. Legacy assets are those previously known as "troubled" or "toxic," the assets the values of which have declined due to the residential mortgage meltdown and the many ripple effects that followed. The Public-Private Investment Program (Program) has two components, one for legacy loans (Loans Program) and the other for legacy securities (Securities Program). Treasury will provide up $100 billion of capital to the two programs. The Federal Deposit Insurance Corporation (FDIC) will support funding for the Loans Program, and the Federal Reserve Board (Federal Reserve) will authorize funding for the Securities Program through the existing Term Asset-backed securities Loan Facility (TALF).

The goals of the Program are to restart the market for legacy loans and securities, clear up the balance sheets of financial institutions and encourage the extension of credit. Additionally, enhanced confidence in financial institutions' balance sheets should reduce uncertainty, restore investor confidence and encourage private capital investment in financial institutions.

The Program follows a series of Treasury, FDIC and Federal Reserve programs and policy decisions to facilitate resumption of more normalized extensions of credit and economic activity. Please see our coverage of these coordinated efforts and the current financial crisis at Financial Crisis Legal Updates and News. Additionally, Treasury publishes information at www.financialstability.gov, the FDIC has launched a dedicated Loans Program site at www.fdic.gov/llp/index.html and the Federal Reserve Bank of New York (New York Fed) maintains a TALF site at www.newyorkfed.org/markets/talf.html.

BACKGROUND

Beginning in 2007, financial institutions began an unprecedented series of announcements reporting write-downs of balance sheet assets. First, subprime residential mortgage loans, and the asset-backed securities into which they had been packaged, experienced losses that had not been forecast. Quickly, more complex securities and instruments the value and returns of which were based on the residential mortgage market experienced losses. Continued and spreading market disruption led to increasingly lower trading prices for a growing class of assets as investors liquidated holdings to raise cash. Exacerbating the problem, application of Financial Accounting Standard 157, or mark-to-market accounting, resulted in financial institutions valuing their balance sheet assets using increasingly lower distressed market prices.1 In a seemingly endless cycle, markets continued to weaken, fire sales of assets by investors seeking cash set lower "market" prices and financial institutions marked down similar assets on their balance sheets resulting in quarterly announcements of write-downs and losses. Investors, counterparties and market participants no longer felt confident that they could accurately assess the health of individual institutions, and concerns spread to the broader financial system.

By the fall of 2008, Federal Reserve efforts were underway to provide liquidity to the credit markets. The failure of Lehman Brothers, sudden sale of Merrill Lynch and continued worsening of the financial sector led Treasury to request authority to address the troubled assets continuing to plague financial institutions. Signed into law on October 3, 2008, the Emergency Economic Stabilization Act (Stabilization Act) authorizes Treasury to spend $700 billion purchasing or insuring the mortgage-related assets held by financial institutions.2 By mid-October, Treasury altered its plan and, rather than purchase troubled mortgage-related assets, launched a program to provide capital injections to financial institutions. Treasury noted that development of a program to purchase mortgage-related assets posed too many challenges, most notably establishing a pricing mechanism satisfactory to both the financial institution sellers and the U.S. taxpayer purchaser. Prices set too low would further harm financial institutions, and could result in further write-downs by non-participating institutions holding the same or similar assets. Prices set too high put taxpayer funds at risk.

Proposals to include private partners in the price setting process address these concerns, but private purchasers also need to minimize the risk of overpaying for troubled assets. Private good-bank bad-bank structures are an alternative considered by many private investors and financial institutions.3 In a good-bank bad-bank structure, the financial institution transfers troubled assets to a new entity capitalized by private investors interested in managing the distressed assets. However, financial institutions believe that application of FAS 157 has artificially lowered the current valuation of troubled assets below their long-term economic value. As a result, financial institutions have been unwilling to sell troubled assets at current market prices. Absent liquid markets and given the overall economic uncertainty, private investors have been unwilling to provide the capital necessary to purchase troubled assets at prices acceptable to the financial institutions. As described below, the Program's risk-sharing and government-supported financing components attempt to address these concerns.

PUBLIC-PRIVATE INVESTMENT PROGRAM

The Program is a joint effort by Treasury, the FDIC and the Federal Reserve. The Program's goal is to improve the health of the financial institutions currently holding legacy assets, which, in turn, is intended to lead to increasing the flow of credit. Treasury will contribute $100 billion of funds available under the Stabilization Act. Treasury's investment is expected to be allocated equally among the Loans Program and the Securities Program. Although Treasury will contribute half of the capital for each purchase of a legacy loan or legacy security, the Loans Program and Securities Program are structured differently and will be developed independently in the coming weeks.

LEGACY LOANS PROGRAM

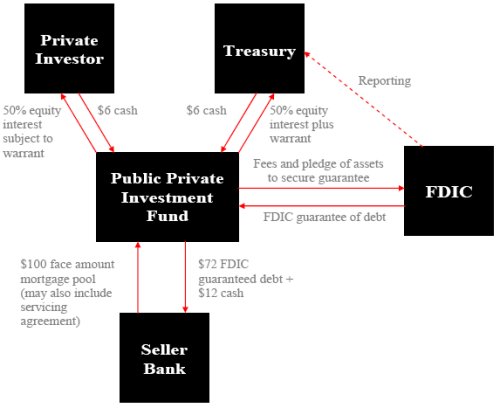

Treasury and the FDIC will establish a series of funds with private investors for the purchase of troubled loans and other assets. Each fund is referred to as a Public Private Investment Fund, or PPIF. As described in more detail below, an interested financial institution will offer loans for sale. The FDIC will determine the ratio of debt to equity for the pool of loans, with no more than a 6-to-1 debt-t0-equity ratio. Private investors will bid on the portfolio through an auction process and, after the FDIC selects a winning bid, the financial institution seller can accept or reject the purchase offer. If a bid is accepted, Treasury and the successful bidder will each provide 50% of the equity required for the purchase. The remaining financing will be in the form of FDIC-guaranteed debt issued by the PPIF. The FDIC-guaranteed debt is expected to be initially placed with the selling banking entity as partial satisfaction of the purchase price. In summary, the banking entity will be selling its legacy loans for cash and a debt instrument guaranteed by the FDIC. Term sheets are currently available at www.financialstability.gov, but detailed terms will be developed through the rulemaking process and as the initial transaction documentation and operational aspects are finalized. Launch of the program is not expected for several weeks, as the comment process should produce significant and potentially material input in the design of the Loans Program.

In its press release, Treasury provided the following sample transaction to describe the Loans Program:

|

Sample Investment Under The Legacy Loans Program Step 1: If a bank has a pool of residential mortgages with $100 face value that it is seeking to divest, the bank would approach the FDIC. Step 2: The FDIC would determine, according to the above process, the appropriate leverage (up to a 6-to-1 debt-to-equity ratio). Step 3: The pool would then be auctioned by the FDIC, with several private sector bidders submitting bids. The highest bid from the private sector – in this example, $84 – would be the winner and the bidder would form a Public-Private Investment Fund to purchase the pool of mortgages. Step 4: Of this $84 purchase price, the FDIC would provide guarantees for $72 of financing, leaving $12 of equity. Step 5: The Treasury would then provide 50% of the equity funding required on a side-by-side basis with the investor. In this example, Treasury would invest approximately $6, with the private investor contributing $6. Step 6: The private investor would then manage the servicing of the assets and the timing of the disposition of assets on an ongoing basis – using asset managers approved by, and subject to oversight by, the FDIC. |

Sample Legacy Loans Investment

Eligibility: Sellers And Assets

Eligible Sellers. Only insured U.S. banks or U.S. savings associations4 are eligible to sell loans under the Loans Program. Foreign owned or controlled entities are not eligible to participate. The Loans Program is unique among federal crisis programs in limiting participants to FDIC-insured banks and savings associations. Another FDIC program, the Temporary Liquidity Guarantee Program (TLGP), limits participants to insured depository institutions and many of their holding companies. The TLGP program is funded through a special assessment. Any shortfall in the TLGP will result in an emergency assessment of all insured depository institutions but not their holding companies. The FDIC has been criticized for the inequity between the beneficiaries of the program and those with responsibility for its funding. In response to these concerns the FDIC has taken a number of actions, including requesting legislative changes to permit fee assessments on holding companies, imposing TLGP program surcharges on many participating holding companies and most recently creating a new surcharge which will not fund the TLGP but will be deposited in the Deposit Insurance Fund (DIF). Limiting Loans Program eligible entities to insured banks and savings associations, rather than a broader group of financial institutions, may have been a response to, and an effort to avoid a repeat of, the perceived inequities of the TLGP.

An interested eligible seller must consult with its primary federal banking regulator to identify loans and assets for the Loans Program. Treasury and the FDIC recommend that potential sellers consider transactions that maximize confidence for depositors, creditors, investors and other counterparties. Once loans are identified, the seller contacts the FDIC. The FDIC will consult with Treasury, who will make the ultimate determination of eligibility, after consulting with the seller's primary federal banking regulator. Sellers will work with the FDIC and the FDIC's valuation firm to complete due diligence and preparation of marketing materials. Once the FDIC has selected a winning bid, the seller will be required to accept or reject the bid by the FDIC's deadline.

Eligible Assets. The program initially targets real estate-related assets, including residential and commercial real estate loans. Although the term sheets list both loans and "other assets," limited information has been provided about asset eligibility and more detail is expected through the rulemaking process. Although the FDIC has ongoing conversations with potential sellers, input through the comment process will be essential for the FDIC to develop clear guidelines and to identify the appropriate assets for inclusion. Loans and any collateral supporting the loans must be "situated predominantly in the United States." Rulemaking will also need to define what constitutes a loan being situated predominantly in the United States.

Affiliated transactions are prohibited. A PPIF cannot purchase an asset if any private investor representing 10% or more of the private equity capital of the PPIF is affiliated with the seller of the asset. Detailed additional limitations and eligibility requirements are expected in the FDIC's proposed rule.

Private Investors

The Program is designed to encourage participation by private investors. The term sheet provides a non-exclusive list of potential investor types, including financial institutions, individuals, insurance companies, mutual funds, publicly-managed investment funds and pension funds. Investors and groups of private investors must prequalify with the FDIC for participation in auctions. TALF, another federal crisis program, permits participation by newly-formed investor funds or entities, provided the potential investor fund and its owners comply with standard know-your-customer, customer identification procedures, anti-money laundering and similar requirements. We expect comparable standards will be applied as part of the FDIC's approval process.

While joint bids are permitted, once an auction has commenced, investors may not form groups or share information with new entrants.

Capital And Debt Structure Of Investments; Fees

Purchases will be made through separately formed PPIFs. Although Treasury has not indicated a specific legal form for the PPIFs, they will need to be structured to permit multiple equity owners, to issue warrants and to issue debt guaranteed by the FDIC. Potential investors will be interested in ensuring the PPIFs are not subject to securities reporting or registration requirements to minimize the costs associated with a Loans Program investment.

Once a pool of assets is identified, the FDIC will obtain a valuation from an independent valuation firm. The valuation will be used exclusively to inform the FDIC's determination of the appropriate level of leverage and its assessment of the structure and value of bids. We do not expect the FDIC valuation to be directly disclosed during the auction process, but the FDIC will disclose the debt-to-equity ratio for a given pool when soliciting bids from approved investors. Based on various debt-to-equity ratios assigned to pools, potential investors will be able to compare pools based on the valuation firm's credit assessment of the pool assets. The leverage ratio for each pool of assets will not exceed a 6-to-1 debt-to-equity ratio. The valuation firm report will also provide input based upon which the FDIC may assess the adequacy of the bids received, but the valuation firm assessment will not establish the price for the asset pool.

Capital Investments

Successful bidders are expected to make their capital investments on a 50/50 basis with Treasury. Alternative arrangements are possible, subject to any minimum investment set by Treasury and protecting the FDIC's security interest in the pool of assets, as collateral for the guarantee on the PPIF debt.

The Stabilization Act requires that Treasury receive a warrant in the PPIF.5 The terms of the warrant and the instrument underlying the warrant have not been described and potential investors will need to consider carefully any potentially dilutive impact of Treasury's warrant.

Debt Financing

If debt financing is used to accompany the capital investment of private investors and Treasury, the FDIC will guarantee debt issued by the PPIF to the financial institution. The amount of debt will be based on the leverage ratio. The FDIC will publish an FDIC Guaranteed Secured Debt for PPIF Term Sheet with more information about the proposed debt terms. Additionally, FDIC staff is developing a rule proposal which will be open for a comment period. We expect material terms of the Loans Program will be developed through the comment process and that the Loans Program FDIC guarantee will include many of the TLGP debt guarantee program terms, including (1) a clear statement that the guarantee is backed by the full faith and credit of the United States, (2) a guarantee structured to cover timely payment of interest and principal and (2) a 20% risk weighting for the FDIC-guaranteed debt.

The FDIC-guaranteed debt will be non-recourse to the PPIF and collateralized by the PPIF's assets, which will consist exclusively of loans and assets acquired through the Loans Program. Although issuance to the seller is planned, the debt may be also sold to third-party investors, either initially by the PPIF or by the seller. Potential investors and sellers should carefully consider the FDIC's proposed rules to evaluate the terms of the FDIC guarantee and the implications for the structure and marketability of the debt. Issues to consider are required disclosure, investment suitability for purchasers of the debt, potential liability of the PPIF as issuer, necessary transfer restrictions and securities law considerations, required minimum denomination and similar requirements and potential debt-holders rights. We expect these issues will be addressed in the rulemaking process, along with treatment of the debt upon failure of the seller institution, if that institution is holding the FDIC-guaranteed debt when the FDIC is appointed receiver.

Fees

The PPIF will pay the FDIC an administrative fee to cover the FDIC's costs of managing the program. Additionally, the PPIF will pay the FDIC an annual fee for the guarantee on debt.6 Bids must be accompanied by a refundable cash deposit equal to 5% of the bid value. Return of the deposit to an unsuccessful bidder will be conditioned on the bidder's compliance with the material terms of the auction process.

In addition to fees, the PPIF will be required to maintain a debt service coverage ratio. Any income received by the PPIF from the assets is subject to capture in an escrow account should the coverage ratio fall below the minimum requirement. It is not expected that private investors will be required to fund a debt coverage account other than from pool cash flows and proceeds from asset sales. Additional details will be provided in the FDIC Guaranteed Secured Debt for PPIF Term Sheet.

Operations And Management

Most of the operational and technical elements of the Loans Program will be developed through the rulemaking and comment process. We summarize below the publicly available information.

- Servicing Of Assets. Initially focused on residential and commercial real estate loans, private investors and the seller are currently expected to negotiate servicing agreements; assets may be sold servicing retained or servicing released.

- Mortgage Modification. PPIFs will be required to comply with the Financial Stability Plan's Making Home Affordable program.7

- Compliance Program. PPIFs will be required to provide information to the FDIC and Treasury upon request, comply with Stabilization Act requirements, including inspection by the Special Inspector General of the TARP and agree to risk management and business conduct standards established for the Program.

Roles Of The FDIC And Treasury

Treasury and the FDIC will enter into an agreement governing allocation of costs and their respective responsibilities for oversight and management of the Loans Program. The FDIC will be reimbursed for expenses incurred in its oversight role, but the term sheet doesn't indicate whether reimbursement will be from Treasury's Stabilization Act funds or from another source, such as the administrative fee.

FDIC. The FDIC is responsible for overseeing formation of the PPIFs and has oversight and management responsibility for funding and operations of each PPIF. As noted, the formal structure for each PPIF has not been described and we expect additional details through the rulemaking process. We expect structures will be modelled after those used for other private equity investments. The FDIC's responsibilities include obtaining detailed pool information on assets in the PPIFs and ongoing information sharing with Treasury.

Treasury. Treasury is responsible for overseeing and managing its equity contributions to the PPIFs.

Considerations For Participants

Considerations For Sellers (Financial Institutions):

- Transparency. Potential sellers should consider carefully the disclosure and confidentiality provisions of the Loans Program. Although the FDIC has extensive experience conducting auctions and managing the sale and transfer of loans through the receivership process, the Loans Program is designed for healthy institutions with ongoing lending relationships and investors and counterparties that may be potential bidders. Banking regulators will encourage institutions to participate in the program. Potential sellers should provide input to the FDIC to ensure program guidelines that achieve desired levels of confidentiality through the bidding process.

- Accounting. Sellers, potential sellers and market participants will need to evaluate whether the Loans Program's auction pricing mechanism establishes new "market" prices for fair value accounting. Assuming multiple bidders for assets and transparency of pricing, this is likely to be a concern. Although the FDIC is optimistic that the affordable financing and co-investment by Treasury will encourage bids above currently depressed market prices, only a successfully concluded auction can determine the ultimate transaction prices.

- Targeted Investment Program.8 Current participants in the Targeted Investment Program are able, with consent, to sell assets currently guaranteed by the FDIC and the Treasury. However, only insured institutions are able to participate in the Loans Program, which may limit the scope of assets eligible for sale.

- FDIC-Guaranteed Debt. As partial compensation, a seller may receive FDIC-guaranteed debt issued by the PPIF. Although we expect the debt to have a low risk-weighting, potential sellers will need to consider the marketability of such an asset and its tenor and terms.

Considerations For Investors:

- Investment Structure. Potential investors will need to carefully consider the investment structure, whether multiple investors join together to form a fund and the rights and responsibilities among those investors, agreements including representations and warranties to Treasury and the FDIC, commitments for fees and expenses, reporting obligations, debt service coverage requirements, books and records requirements for the PPIF and an exit strategy, among other factors.

- Mortgage Modification. Residential real estate loans acquired by a PPIF will be covered by the Financial Stability Plan's Making Home Affordable program. Eligible homeowners will be able to reduce the debt-to-income ratio of their mortgage to 31%. Potential investors will need to carefully evaluate the potential impact of Making Home Affordable on the ultimate value of the loans in a pool as well as the related servicing costs.

- Treasury Warrant. Potential investors will need to review carefully the terms of the warrant issued by the PPIF to Treasury, including the form of the underlying security, exercise rights, term, transferability and economic impact of exercise of the warrant.

- FDIC-Guaranteed Debt. The PPIF will be able to issue FDIC-guaranteed debt, which will provide affordable financing for the purchase of the legacy loans. As discussed above, when more detailed information is provided by the FDIC, potential investors will need to understand their rights and responsibilities with respect to the debt instrument.

- Government Oversight: The PPIF will be subject to oversight of the FDIC as well as Treasury, including the Special Inspector General of the Troubled Assets Relief Program. Because a PPIF will be established for each investment, the private investor(s) behind the PPIF will be responsible for compliance with, or hiring and asset manager to comply with, all of the Loans Program requirements, including requests for reporting, access to books and records, maintenance of debt coverage ratios and related reporting and ongoing payments of fees. Previously unregulated entities will need to evaluate the time and economic burdens of compliance with multiple federal regulators.

See also "Executive Compensation and Corporate Governance" below.

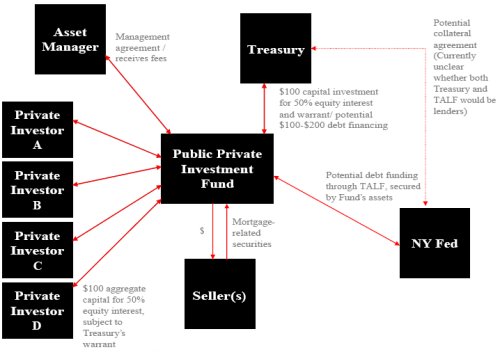

LEGACY SECURITIES PROGRAM

Treasury will authorize asset managers to establish and manage funds to purchase residential and commercial mortgage-backed securities from financial institutions. The funds, each a Public-Private Investment Fund or PPIF, will be capitalized by private investors and Treasury. Additionally, each fund can apply for a non-recourse loan from Treasury and, under terms to be announced, a TALF loan from the New York Fed.

Term sheets are currently available at www.financialstability.gov and detailed terms will be established through the rulemaking process and as initial transaction documentation and operational aspects are finalized. Treasury has also solicited input from potential asset managers, as described below.

In its press release, Treasury provided the following example of a sample investment under the Securities Program:

|

Sample Investment Under The Legacy Securities Program Step 1: Treasury will launch the application process for managers interested in the Legacy Securities Program. Step 2: A fund manager submits a proposal and is pre-qualified to raise private capital to participate in joint investment programs with Treasury. Step 3: The Government agrees to provide a one-for-one match for every dollar of private capital that the fund manager raises and to provide fund-level leverage for the proposed Public-Private Investment Fund. Step 4: The fund manager commences the sales process for the investment fund and is able to raise $100 of private capital for the fund. Treasury provides $100 equity coinvestment on a side-by-side basis with private capital and will provide a $100 loan to the Public-Private Investment Fund. Treasury will also consider requests from the fund manager for an additional loan of up to $100 to the fund. Step 5: As a result, the fund manager has $300 (or, in some cases, up to $400) in total capital and commences a purchase program for targeted securities. Step 6: The fund manager has full discretion in investment decisions, although it will predominately follow a long-term buy-and-hold strategy. The Public-Private Investment Fund would also, if the fund manager so determines, be eligible to take advantage of the expanded TALF program for legacy securities when it is launched. |

Sample Legacy Securities Investment

Eligibility: Sellers, Securities And Investors

Eligible Sellers. Eligible sellers include those institutions from whom Treasury can purchase troubled assets under the Stabilization Act. These "financial institutions" must be established and regulated under the laws of the United States9 and have significant operations in the United States. The definition includes a non-exclusive list of institution types: banks, savings associations, credit unions, security brokers or dealers or insurance companies. Expressly excluded are central banks of or any institution owned by a foreign government. We expect that detailed Treasury guidelines or updated FAQs will provide more information on entity eligibility.

Eligible Securities. To be eligible for purchase by a PPIF, a security must be:

- either a residential or commercial mortgage-backed security;

- originally issued prior to January 1, 2009;

- originally rated in the highest rating category by at least two NRSROs, without ratings enhancement;10

- secured by loans or other eligible assets situated predominantly in the United States;

- backed by loans and not other securities or derivatives (subject to limited exceptions); and

- eligible under other criteria to be established by Treasury.

Investors. There are currently no Securities Program eligibility requirements for investors. However, as described below, a PPIF cannot purchase securities from an investor whose capital contribution equals or exceeds 10% of the PPIF's private equity capital. Treasury indicated that it will consider suggestions from asset managers seeking to raise equity capital for the PPIF from retail investors. We expect participation in TALF may be conditioned on compliance with TALF's borrower eligibility rules.11 Under these rules, the entity obtaining a TALF loan, such as the PPIF, may need to provide information about its significant (10% or more) owners.

Asset Managers

Treasury currently anticipates hiring five asset managers, one for each PPIF, but may increase the number based on the number of applicants.

Qualifications. Asset managers will be evaluated based on (1) demonstrated capacity to raise at least $500 million of private capital, (2) demonstrated experience investing in eligible securities, including through performance track records, (3) a minimum of $10 billion market value of eligible securities under management, (4) demonstrated operational capacity to manage legacy securities in PPIFs in a manner consistent with Treasury's stated objectives for the program12 while also protecting taxpayers and (5) being headquartered in the United States.

Application Process. Interested parties are required to apply to Treasury no later than 5:00 p.m. on April 10, 2009. By May 1, 2009, Treasury will inform applicants of preliminary qualification and will communicate the time period for the asset manager to raise at least $500 million of private equity capital. Applications should include (1) proposed structure of the PPIF, (2) summary of proposed material terms including withdrawal rights and use of realized capital, (3) anticipated debt financing from Treasury and the TALF, (4) proposed fees, (5) tax considerations, (6) asset management strategies, (7) risk management and Securities Program compliance and (8) valuation, monitoring and reporting plans.

Responsibilities. Managers will be responsible for asset selection and pricing as well as asset liquidation, trading and disposition.

Reporting. Managers will be responsible for monthly reporting to Treasury regarding assets purchased and sold, current valuations and profits and losses. Valuation information for reporting purposes must include third party sources and annual audited valuations performed by a nationally recognized accounting firm. The managers must also provide Treasury with access to books and record of the PPIF, and agree to waste, fraud and abuse protections for the PPIF.

Fees. Managers may charge fees to private investors. Proposed fees must be included in the asset manager's application to Treasury and we expect fees will remain competitive to encourage private investment in the asset manager's PPIF. Additionally, during the application process, prospective managers can propose fixed management fees for Treasury. Fees assessed against Treasury will be payable exclusively from any distributions to Treasury as an equity investor. If the manager collects fees other than the fee payable by Treasury and management or incentive fees payable by private investors, those fees must accrue to the benefit of the private investors and Treasury, in proportion to their respective investments. The mechanism for this fee sharing arrangement has not yet been provided.

Capital And Debt Structure

Treasury is expected to match the initial private equity capital investment in each fund. Funding of Treasury's equity investment will be proportional to equity investments by private investors. Asset managers should propose a term for the Treasury investment, which should be no longer than 10 years, subject to extension with Treasury's consent. Treasury will also be issued a warrant by the PPIF, as is required by the Stabilization Act. Potential investors will need to review carefully the warrant terms, when available, to evaluate any potentially dilutive impact.

Debt financing will be available to the PPIF from Treasury and from the TALF program. Limited information is currently available about debt financing from Treasury. Asset managers will be able to obtain non-recourse loans, secured by the PPIF's assets in an amount equal to 50% of its fund's total equity capital. Additional loans, raising the outstanding debt from Treasury up to 100% of the fund's total equity capital, may be available if the fund has satisfied restrictions on asset level leverage, withdrawal rights, disposition priorities and other factors to be established by Treasury. No Treasury debt financing will be available to a fund that has provided its private investors with voluntary withdrawal rights. Any debt financing offered by Treasury will mature concurrent with the term of the Treasury equity investment.

Details are currently unavailable on the extension of the TALF program to include legacy securities. For general information about the TALF's current lending programs, please see our related Client Alerts at Financial Crisis Legal Updates and News and the TALF website maintained by the New York Fed at www.newyorkfed.org/markets/talf.html.

Considerations For Participants

Considerations For Asset Managers:

- Limited Available Information. Applications, due to Treasury by April 10, 2009, require asset managers to define the terms of the Securities Program, including describing their ability to attract significant private investors to a distressed and illiquid market. Program terms, including representations, covenants and liability to Treasury and potentially the New York Fed is unknown. Asset manager applicants will need to carefully consider the models of previously announced Treasury and Federal Reserve programs and provide Treasury with detailed information to facilitate development of an operational feasible program.

- Debt Financing. Limited information has been provided about the terms of available Treasury funding for the program. When available, asset managers need to carefully consider information on how the TALF funding will be provided to the PPIFs. Currently, TALF provides three year loans and requires collateral be held by the New York Fed custodian. While it is anticipated that a mortgage-backed securities program under TALF will provide longer term loans, more details are needed to assess the benefits of the program and market the investment to prospective private investors.

- Mortgage Modification. We expect the asset manager and PPIF will be required to take reasonable steps to apply the Making Home Affordable modification program to the residential mortgages underlying acquired mortgage-backed securities. Asset managers will need to consider the impact of the Making Home Affordable program on securities being considered for purchase by the PPIF.

- Government Oversight: The PPIF will be subject to oversight of the Treasury, including the Special Inspector General of the Troubled Assets Relief Program. The asset manager will be responsible for compliance with all of the Securities Program requirements, including requests for reporting, access to books and records, negotiating disposition or exercise of the warrant and ongoing payments of fees. Previously unregulated entities will need to evaluate the time and economic burdens of compliance with a federal regulator.

Considerations For Investors:

- Role Of Asset Manager. Unlike the private investors in the Loans Program, private investors in a Securities Program PPIF will authorize a third party private asset manager to make the purchase, management and disposition decisions. Potential investors will need to carefully consider the asset manager's investment guidelines, plan and reporting commitments, as well as available exit strategies for the investment.

- Debt Financing. Economic analysis of a potential investment in a Securities Program PPIF cannot be completed without additional details on the funding that will be available under the TALF. Currently, the Loans Program contemplates a debt-to-equity ratio of no more than 6-to-1. Treasury debt funding under the Securities Program, by comparison, is targeted at no more than 100% of the total equity capital. Additionally, the New York Fed will need to establish eligibility criteria, program documentation and terms for TALF loans targeted to mortgage-related securities.

Considerations For Sellers (Financial Institutions):

- Operations. Potential sellers should watch for announcements regarding the process by which securities will be offered to PPIFs to determine required disclosure, pricing mechanisms and eligibility requirements.

- Accounting. Sellers, potential sellers and market participants will need to evaluate whether the Securities Program's yet to be disclosed pricing mechanism will establish new "market" prices under fair value accounting standards.

- Comparison Of Programs. A potential seller may wish to compare the benefits of participating in the Loans Program with participating in the Securities Program. Under the Loans Program, a portion of the consideration paid for the assets sold to the PPIF may be in the form of FDIC-guaranteed debt. Consideration for legacy securities sold to a Securities Program PPIF, on the other hand, is expected to be cash. Additionally, Sellers should evaluate potential accounting impacts, transparency of pricing of loans or securities and pricing mechanisms under each program.

EXECUTIVE COMPENSATION AND CORPORATE GOVERNANCE

Information provided by Treasury on the Loans Program and the Securities Program indicates that "passive" private investors in the Programs will not be subject to the executive compensation and corporate governance requirements of the Stabilization Act, as amended by the Recovery Act. A definition of passive private investor has not been provided. Additionally, information regarding applicability of the executive compensation requirements to active investors, asset managers of the Securities Program PPIFs and financial institution sellers of legacy loans or securities is unknown.

The Stabilization Act imposes executive compensation and governance requirements on recipients of Treasury funds under certain circumstances. Executive compensation rules issued by Treasury last fall closely follow the Stabilization Act's requirements and impose unprecedented, but measured, limits on executive compensation and governance. Widespread media reports of seven figure bonuses for executives at institutions receiving substantial capital from Treasury led to inclusion of stricter executive compensation and governance requirements in the American Recovery and Reinvestment Act of 2009 (Recovery Act). Reflecting the frustration of Congress with perceived misuses of federal funds for executives at poorly performing institutions, the Recovery Act provisions are retroactive. Additionally, the Recovery Act changed the standard under which the executive compensation rules are considered applicable. The Recovery Act imposes restrictions on an institution that "has received or will receive financial assistance" under a Stabilization Act program. Rules interpreting the Recovery Act provisions haven't been released by Treasury and the Recovery Act's application to potential parties in the Program remains unclear. We expect Treasury to release regulations promptly consistent with its goal of encouraging participation in the Program.

CONCLUSION

Financial institutions' balance sheets are burdened with investments the markets for which are distressed and for which prices are available only at fire sale levels. Absent a shift in economic conditions, or a dramatic change in the accounting rules, continued downward pressure on valuations seems likely. Recent guidance from the Financial Accounting Standards Board addressing some of the concerns raised about FAS 157 may provide incremental and forward-looking improvements, but is unlikely to dramatically restore balance sheets. Market forces appear unable to remedy the situation and the government programs announced to date have not resolved the ongoing balance sheet issue. As noted in Treasury's statements, the example of the Japanese banking crisis, where financial institutions worked out loans over a decade, does not provide a promising model. Private and public forces working together may provide the solution. The structure of our regulatory system, however, continues to create artificial distinctions in programs.

The FDIC supported Loans Program is limited to insured banks and savings associations. Recent experience guaranteeing debt issued by holding companies exposed the FDIC to inequity claims by the insured institutions responsible for funding any shortfalls in the program. The FDIC is seeking a legislative remedy to the inequities of its statutory limitations on funding its programs, but it is currently unclear whether such expanded authority will be granted and, if it is granted, whether the Loans Program will be expanded to other institutions such as holding companies of insured banking entities. Treasury is also limited in its ability to fund the Securities Program, as it nears depletion of its Stabilization Act resources.

Although the Federal Reserve may bridge the funding gap for the Securities Program when additional details are released, the differences between the Loans Program and the Securities Program highlight the different roles between partnering with the FDIC and the Federal Reserve. The FDIC, with experienced in-house loan purchase, sale and management teams, is well suited to manage the auction process for numerous pools of loans. The process will permit private investors to conduct diligence and structure bids. The Securities Program, on the other hand, places an asset manager between private investors and pools of legacy securities. While pools of loans securitized into AAA- rated notes were once thought to be fungible assets, the purchase and management of which could be delegated to a fund manager, we have learned the hard way the fallacies of those assumptions. Additional information and transparency into process and guidelines for funds will be needed to attract private investors to provide capital to investments in unknown pools of assets that were initially rated "AAA" and are now considered "toxic" by their current owners.

So, was it worth the wait? We now have rough outlines of two programs that reflect the complexity of the challenge and the limitations of the authorities and roles of various government parties. Guidelines, terms, the comment process and applications need to develop these outlines into workable solutions. If no one else has discovered the magic bullet before now, did we really expect all of the answers handed to us on a silver platter? It is a beginning, and for that alone, it was worth the wait.

Footnotes

1. Financial Accounting Standard 157 (FAS 157) generally requires that a financial institution record the value of certain assets based on the most current market transaction price, assuming a market value is available. FAS 157 provides than an institution can use an internally developed model to assign a value to an asset if a market price is not available or reflects a distressed trading price in an illiquid market. Auditors have not felt comfortable using internal models for assets when any market price is available. Recently the Financial Accounting Standards Board, in response to industry and Congressional feedback, has released additional guidance on distressed transactions and illiquid markets. The impact of this recent guidance on financial institutions' balance sheets is not known at this time. Please see our related Client Alert Mark-to-Market Update: After Congressional Hearing, FASB Proposes New Fair Value Accounting Guidance.

2. In addition to addressing mortgage-related assets, the Stabilization Act considers a "troubled asset" "any other financial instrument that [Treasury], after consultation with the Chairman of the [Federal Reserve], determines the purchase of which is necessary to promote financial stability."

3. For more information about alternative structures, please see our Client Alert Good Bank-Bad Bank: A Clean Break and a Fresh Start.

4. According to the Legacy Loans Program Summary of Terms, "U.S. bank" and "U.S. savings association" means a bank or savings association organized under the laws of the United States or any State of the United States, the District of Columbia, any territory or possession of the United States, Puerto Rico, Northern Mariana Islands, Guam, American Samoa, or the Virgin Islands.

5. Section 113(d) of the Stabilization Act requires that when Treasury purchases any troubled asset, in this case an investment in the PPIF, it must receive a warrant with terms that "provide for reasonable participation . . . in equity participation or a reasonable interest rate premium" and protect against taxpayer losses from sale of assets.

6. The FDIC's participation in the Loans Program was authorized upon a finding of systemic risk, similar to the authority for the establishment of the TLGP. Systemic risk program funding is outside of the DIF, through a special assessment. If the guarantee fees are insufficient to cover the FDIC's costs, an emergency special assessment will be imposed on all insured depository institutions. A portion of the fees collected under the Loans Program will be deposited in the DIF, which is currently experiencing a low reserve rate. It is unclear how any shortfall in the Loans Program would be addressed given deposit of some funds in the DIF and the different assessment processes for DIF funding and systemic risk funding.

7. For more information on federal mortgage modification efforts and the Making Home Affordable program, please see our Client Alert The Rear View Mirror: Mortgage Finance and Mortgage Modification Efforts.

8. For more information on the FDIC and Treasury guarantees on pools of assets, please see our Client Alert Treasury's Asset Guarantee Program.

9. The entity must be established and regulated under "the laws of the United States or any State, territory, or possession of the United States, the District of Columbia, Commonwealth of Puerto Rico, Commonwealth of Northern Mariana Islands, Guam, American Samoa, or the United States Virgin Islands."

10. We expect that the limit on ratings enhancement will mirror the similar current requirement in the TALF that the rating cannot be obtained as a result of a guarantee or insurance policy; it will not limit enhancement such as overcollateralization

11. For more information, please see our most recent TALF Client Alert TALF to Launch with Updated Terms: Can Wall Street Help Main Street?

12. The objective is to generate attractive returns for taxpayers and private investors through long-term opportunistic investments in accordance with following predominantly a long-term buy and hold strategy, subject to limited trading approved by Treasury.

Because of the generality of this update, the information provided herein may not be applicable in all situations and should not be acted upon without specific legal advice based on particular situations.

© Morrison & Foerster LLP. All rights reserved