With the imposition of a new 3.8% "net investment income tax" (the "NIIT") pursuant to Section 1411 of the Internal Revenue Code of 1986, as amended (the "Code") on passive income and the imposition of an additional .9% on the uncapped Medicare portion of the self-employment tax under Section 1401 of the Code (the "SET") beginning in 2013, individuals who act as private equity and hedge fund managers or advisors have been searching for ways to prevent the application of the NIIT and the SET to their distributive shares of the income from the fund. While certain fund managers may be able to escape the imposition of the SET on partnership income, the analysis is complex, and there is significant uncertainty with respect to how the Internal Revenue Service ("IRS") and courts will interpret the relevant statutory provisions. However, it is clear that if income is subject to the SET, it will not be subject to the NIIT and vice versa. The following is a general overview of how the NIIT and SET could apply to individual fund managers, and does not purport to be an exhaustive analysis of the subject.1

TAX ON SELF-EMPLOYMENT INCOME

The SET has two components: a 12.4% tax on income from self-employment up to a cap, and a 2.9% tax on self-employment income that is uncapped. Self-employed individuals can deduct one-half of their SET in calculating adjusted taxable income. Starting in 2013, the SET applies to self-employment income at a rate of 3.8% for income over a "threshold amount." The threshold amount is $250,000 for a joint return, $125,000 for a married taxpayer filing separately, and $200,000 for a single return. Notably, the additional .9% tax is not deductible for income tax purposes.

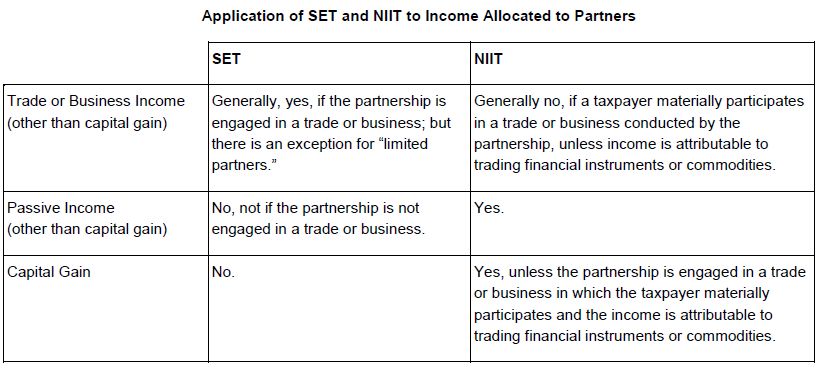

"Self-employment income" is broadly defined. Self-employment income includes income from "services" (other than as an employee), as well as income from a "trade or business" that is received by an individual directly or through a partnership engaged in a trade or business, with a significant exception for "limited partners."2 "Guaranteed payments" made to a limited partner, however, are subject to SET even though income allocated to such partner from the partnership is not. Notably, SET does not apply to income allocated to shareholders by an S corporation.

In spite of the seemingly clear statutory exemption from SET for income derived by limited partners, there is significant uncertainty regarding the meaning of "limited partner" for self-employment tax purposes. In 1997, the IRS issued proposed Treasury Regulations3 that have not yet been adopted addressing the meaning of "limited partner" for SET purposes. The proposed Treasury Regulations treat partners (including members of a limited liability company) as limited partners for this purpose only if (among other requirements) they work less than 500 hours per year in the business of the partnership, regardless of their status as a limited partner for state law purposes.

Individuals who are "limited partners" for state law purposes should be able take the position that the distributions they receive from the partnership would not be subject to self-employment tax based on the statutory exemption for limited partners under Section 1402(a)(13) of the Code. It is not clear whether members of a limited liability company are "limited partners" for purposes of the SET. Since members of an LLC are generally treated in the same manner as limited partners for all other tax purposes, it would be reasonable to conclude that they should be treated as limited partners for purposes of the SET. However, there is no definitive guidance on the issue. Accordingly, given this uncertainty, a limited partnership structure may be preferable to an LLC structure for purposes of minimizing SET.

Nevertheless, the IRS could assert that the limited partners are not "limited partners" for purposes of the self-employment tax, based on Renkemeyer, Campbell & Weaver, LLP v. Comm'r.4 The Tax Court reasoned that members of a law firm operating as an LLP were not "limited partners" for purposes of the SET because substantially all of the law firm's revenues were derived from legal services performed by the partners, and each partner contributed only a nominal amount of capital. The court noted that the LLP's income did not represent "earnings of an investment nature." Although Renkemeyer addresses whether a partner of an LLP, as opposed to a limited partnership, is a limited partner, the factors that the Tax Court considered in its decision demonstrate some support for the position of the IRS in the proposed Treasury Regulations.

Interestingly, if the IRS does adopt final regulations that contain a material-participation standard, a fund manager's share of fund income from the fund that includes carried interest income from the fund arguably should not be subject to SET, even though the manager is engaged in a trade or business. This is because the question of whether the income is trade or business income should depend on whether the fund itself (as opposed to the manager) is engaged in a trade or business. For funds that adopt a "hold and sell" strategy and therefore do not conduct enough activity to be engaged in a trade or business, the income that includes carried interest income should be exempt from SET. However, this will depend on how the Treasury Regulations are drafted.

NET INVESTMENT INCOME TAX

The NIIT is a 3.8% tax imposed on certain income ("net investment income") of individuals, estates, and trusts (other than tax-exempt trusts and grantor trusts). The NIIT applies to the lesser of: (i) net investment income; or (ii) adjusted gross income in excess of a "threshold amount." For individuals, the threshold amount is the same as for the SET. Net investment income includes investment income such as dividends, interest, annuities, royalties, and rents that are not derived in the ordinary course of a trade or business. Notably, however, net investment income does not include income that is subject to the SET.5

Net investment income also includes (i) passive activity income under Section 469 of the Code; (ii) all income attributable to trading in "financial instruments" or commodities, even if the income is not passive activity income under Section 469 of the Code and (iii) net gain attributable to the disposition of property, unless the property is held in a trade or business of the seller in which the taxpayer materially participates and which is not trading in financial instruments or commodities. Thus, net gain from the disposition of property will not be subject to the NIIT only if the partnership is engaged in a trade or business in which the taxpayer materially participates and is not income from trading in financial instruments or commodities. However, as noted in more detail below, in the case of a fund following a buy-and-hold strategy and therefore not engaged in any trade or business, net gains from the disposition of property will be subject to the NIIT because neither of the two exceptions will apply.

Passive activity income under Section 469 of the Code generally includes rental income and all other income from a trade or business if the recipient does not "materially participate" with respect to the trade or business. Under Treasury Regulations under Section 469 of the Code, there are safe harbors for determining when an individual "materially participates" in a trade or business of the entity generating such income, one of which applies to individuals who work more than 500 hours per year in the trade or business generating the income.6 The IRS has issued proposed regulations under Section 1411 of the Code providing additional guidance on the application of the material-participation tests.7 Thus, if a partner "materially participates" in the trade or business of the partnership generating such income, his or her income from the partnership will not be subject to NIIT attributable to trading financial instruments or commodities.

The proposed Treasury Regulations under Section 1411 of the Code indicate that the underlying partnership generating the income needs to be engaged in a trade or business in which the taxpayer materially participates. It is not sufficient for the taxpayer to materially participate in a partnership that provides services to the underlying fund. The proposed Treasury Regulations provide an example in which a lower-tier partnership is not engaged in a trade or business but the upper-tier partnership is, and the lower-tier partnership earns dividend income that is allocated to the upper-tier partnership.8 The example concludes that the income allocated from the lower-tier partnership is ineligible for the trade or business exception. Once the income is classified at the lower-tier partnership level as not derived from a trade or business, it will not be recharacterized merely because a partner, the upper-tier partnership, is itself engaged in a trade or business. For managers of funds that do not engage in a trade or business such as private equity funds with a buy-and-hold strategy where all activity is undertaken by an upper-tier management company, their income attributable to the fund, including capital gain, will be subject to NIIT, assuming that the proposed Treasury Regulations are adopted in current form.

As noted above, although net investment income specifically excludes all income with respect to which a taxpayer materially participates in the trade or business, the NIIT will apply to all income not attributable to trading in "financial instruments" or commodities ("trading income"). Proposed Treasury Regulations define "financial instruments" as including stocks, equity and debt instruments, options, derivatives, and commodities. Hedge funds and other funds that enter into the activity of buying and selling securities for their own accounts to generate profit from daily market swings would be considered to generate "trading income." Accordingly, managers of hedge funds would appear to be subject to the NIIT on income derived from such funds, even though such individuals materially participate in the business.

CONCLUSION

As demonstrated by the foregoing discussion, the application of the SET and NIIT to income of an individual investment manager of a fund is complex. In very narrow situations, such as where an individual materially participates in the trade or business of an investment manager that has an interest in a fund that is not engaged in trading in financial instruments or commodities but is engaged in a trade or business, it may be possible, with favorable statutory interpretation, to conclude that neither the SET nor the NIIT apply to such income. One thing that is clear is that an individual cannot be subject to both the SET and the NIIT. It is also clear that an individual who is a limited partner in a limited partnership under state law should not be subject to SET (which may make a limited partnership structure preferable as compared to an LLC structure), but both limited partners and members of LLCs could be subject to NIIT. Managers who receive management fees as well as income from the fund as a carried interest or otherwise could be subject to SET on the management fees and to NIIT on the fund income. Given the numerous factors that apply in determining whether the SET or the NIIT are applicable, investment managers should consult their tax advisors to address their own unique circumstances.

Footnotes

1 Note that somewhat different considerations apply with respect to managers of real estate funds that are beyond the scope of this alert.

2 Code Section 1402(a)(13).

3 Prop. Treas. Reg. Section 1.1402(a)-2. However, following the release of the Proposed Regulations, Congress imposed a one-year moratorium in August 1997 preventing the Treasury from adopting regulations dealing with the employment tax treatment of limited partners. The moratorium expired on July 1, 1998. The 1997 Proposed Regulations were never adopted, even after the moratorium expired.

4 136 TC 137 (2011) (Renkemeyer).

5 Code Section 1411(c)(6).

6 Treas. Reg. Section 1.469-5T(a).

7 The IRS is seeking comment on the proposed regulations; the deadline for written or electronic comments was March 5, 2013.

8 Prop. Treas. Reg. Section 1.1411-4(b)(3), Example 1.

Because of the generality of this update, the information provided herein may not be applicable in all situations and should not be acted upon without specific legal advice based on particular situations.

© Morrison & Foerster LLP. All rights reserved