The unprecedented economic dislocation caused by the COVID-19 pandemic has prompted comprehensive legislative and administrative responses. The Coronavirus Aid, Relief, and Economic Security Act (CARES Act or Act), signed into law on March 27, 2020, is the largest single piece of recovery legislation in US history. It is the third piece of federal legislation enacted in response to the COVID-19 crisis. Since then, a fourth bill has been passed to provide additional funding and relief, and still more legislation is in the works.

Unlike many industries that are largely shut down or sharply curtailed due to the pandemic, the financial services sector is generally seen by policymakers as a critical component of the solution. Many of the CARES Act's primary avenues for assistance to the business community are through loan and loan guarantee programs that rely on financial institutions to extend the credit and provide the liquidity needed by affected businesses. Loan programs such as the $500 billion U.S. Department of the Treasury (Treasury Department) loan/guarantee/investment program make up a substantial portion of the CARES Act. Even before the legislation was enacted, the Board of Governors of the Federal Reserve System (Federal Reserve) had begun expanding its efforts, in the form of a wave of financing facilities. In acting on the present crisis, both the Treasury Department and the Federal Reserve are drawing on experience gained in the aftermath of the 2008 financial melt-down.1

General Financial Relief Under the CARES Act

Title IV of the CARES Act provides $500 billion to the Treasury Department for loans, loan guarantees, and other investments, including: (1) $25 billion for passenger air carriers and related businesses; (2) $4 billion to cargo air carriers; (3) $17 billion to businesses critical to maintaining national security; and (4) the remaining $454 billion (plus any amounts not used in (1) through (3)) in support of Federal Reserve emergency lending facilities to eligible businesses, states, and municipalities. Requirements for categories (1) and (2) are described in a separate section for air carrier financial relief, and the requirements for category (3) are the same as categories (1) and (2). This section therefore focuses on the different set of requirements that applies to category (4).

The $454 billion in category (4) will be made available through the Federal Reserve's emergency lending authority under section 13(3) of the Federal Reserve Act. Multiple programs and facilities are expected to be established in this category. Eligible businesses are those that did not receive "adequate economic relief" in other parts of CARES Act. The following requirements and conditions apply:

- For direct loans, until one year after the loan is paid off, no stock buybacks unless contractually obligated, and no dividends on common stock;

- For direct loans, restrictions on employee compensation (summarized further below);

- Eligible business must be created or organized in the US or under the laws of the US, and must have significant operations in and majority of employees based in the US;

- No loan forgiveness;

- No conflicts of interest (certification that President, Vice President, executive department head, member of Congress, or their immediate families do not own 20% or more of outstanding equity); and

- All the requirements of section 13(3)

of the Federal Reserve Act apply, including:

- Loan collateralization requirement: The relevant statute and regulations provide that all credit extended under 13(3) must be "indorsed or otherwise secured to the satisfaction of the lending Federal Reserve Bank." In practice the Federal Reserve has typically required investment grade collateral even if not statutorily required. It remains to be seen whether Treasury will continue the same practice for the programs and facilities established under the CARES Act.

- Not being insolvent

- Certification by the applicant, audited financials, or other information as the Federal Reserve may determine to be relevant.

- Solvency defined in Federal Reserve regulations as (1) being in bankruptcy, (2) generally not paying undisputed debts as they become due during the 90 days preceding the date of borrowing, or (3) Federal Reserve otherwise determines the applicant is insolvent.

Relief for Mid-Sized Businesses: Within this general $454 billion fund, the CARES Act provides that the Treasury "shall endeavor to implement" a program that provides financing to banks and other lenders that would make direct loans (no higher than 2% interest rate and no payment first six months) to midsize businesses (including nonprofit organizations to the extent practicable) with between 500 and 10,000 employees, subject to additional criteria, including criteria related to workforce retention, workforce restoration, prohibition on outsourcing or offshoring, maintenance of collective bargaining agreements, and remaining neutral in union organizing. These additional criteria do not necessarily apply to other programs and facilities established in this general $454 billion fund. This relief, including these criteria, does not appear to have been implemented yet.

Employee Compensation Limit: There are two prongs that apply until one year after the loan is paid off:

- For those employees who made over $425,000 in 2019, (1) no pay increase and (2) severance pay capped at twice the total compensation in 2019.

- For those employees who made over $3 million in 2019, total compensation to be capped at $3 million plus 50% of the excess over $3 million (e.g., if total compensation was $4 million in 2019, it will be capped at $3.5 million ($3 million plus 50% of the $1 million in excess of $3 million).

Financial Agents: Treasury is authorized to designate financial institutions—including but not limited to depositories, brokers, dealers, and other institutions—as financial agents of the United States for the purpose of performing the Secretary's duties under Title IV of the CARES Act.

US Warrant Provisions: The requirement that the US government will share in any gains made pursuant to such loans would continue to apply for the three-sector specific industries, but not for the broader general business loan pool. Additionally, there is a new provision requiring the Treasury Department to liquidate its interest in any authorized loan programs in Title IV as soon as soon as reasonably practical, while maximizing the US government's interest.

New Inspector General: Section 4018 establishes, within the Treasury Department, the Office of the Special Inspector General for Pandemic Recovery who will oversee implementation of the CARES Act. The President will be responsible for nominating this individual "as soon as practicable after any loan, loan guarantee, or other investment is made" under the program. The Special IG will be subject to the removal provisions in Section 3(b) of Inspector General Act. The Special IG will have authority to conduct, supervise, and coordinate audits and investigations of "the making, purchase, management, and sale of loans, loan guarantees, and other investments made by the Secretary," in addition to the Secretary's management of the program. In doing so, the Special IG will have the authorities provided in section 6 of the Inspector General Act of 1978 and will be considered exempt from termination by the Attorney General. The bill authorizes $25 million to fund the Special IG's activities.

Congressional Oversight Commission: The CARES Act creates a Congressional Oversight Commission to oversee the execution of Subtitle A of Title IV of the CARES Act (which includes the emergency relief programs) by the Treasury and the Federal Reserve. The Commission must submit regular reports to Congress and review the implementation of the program. Membership in the Commission will consist of one member appointed by the Speaker of the House, the House Minority Leader, the Senate Majority Leader, and the Senate Minority Leader, respectively. The fifth member, Commission's Chair, will be jointly appointed by the Speaker and the Senate Majority Leader. The first report of the Congressional Oversight Commission can be found here.

Exchange Stabilization Fund: Section 4015 of the Act suspends the Dodd-Frank Act prohibition on using the Exchange Stabilization Fund (ESF) to establish guarantee programs for money market funds until the end of 2020. It also provides for appropriations to reimburse the ESF after 2020 if claims exceed fees collected.

AIR CARRIER FINANCIAL RELIEF UNDER THE CARES ACT

Air Carrier Loans and Loan Guarantees

As described above, the Act has allocated up to $29 billion for loans and loan guarantees to air carriers and related businesses. This targeted financing recognizes both the dislocations affecting these businesses and their critical economic and social function. In reviewing the following summary, it is important to keep in mind that, while loans and loan guaranties to air carriers and related businesses are subject to some of the same requirements that apply generally under the Act, there are other specific requirements that need to be followed. The deadline to apply for air carrier loans was April 17, 2020.

Eligible Businesses: The CARES Act allocates up to $25 billion of its loan facility to make loans and loan guarantees to (1) passenger air carriers; (2) "eligible businesses" that are certified and approved to perform inspections, repair, replace, or overhaul services; and (3) ticket agents. Up to an additional $4 billion is allocated to make loans and loan guarantees to cargo air carriers. The loans and loan guarantees are to be provided only to applicants that are eligible businesses for which credit is not reasonably available at the time of the transaction, and are available only if the obligation of the applicant is "prudently incurred." An "eligible business" includes any air carrier and any United States business that has not otherwise received adequate economic relief in the form of loans or loan guarantees provided under the CARES Act. The eligible business must have incurred, or be expected to incur, "covered losses" such that the continued operations of the business are jeopardized, as determined by the Treasury Secretary. A "covered loss" is defined as a loss "incurred directly or indirectly as a result of coronavirus, as determined by the Secretary."

Eligible business will need to certify that they were created or are organized in the United States or under the laws of the United States and have significant operations in, and a majority of employees based in, the United States. In addition, each business's principal executive officer and the principal financial officer will need to certify that the proposed borrower is eligible to enter into the transaction, including in particular that it is not a "covered entity," which is an entity "controlled" (by virtue of owning, controlling or holding not less than 20%, by vote or value, of the outstanding amount of any class of equity interests in the entity) by identified "covered individuals," which include the President, the Vice President, the head of any Executive department, any member of Congress, and specified relatives of such persons.

Key Loan Terms: The terms of the loans and loan guarantees are to be determined by the Secretary, but are required to (1) be secured or bear an interest rate that reflects the risk of the loan or loan guarantee and, to the extent practicable, not be less than an interest rate based on market conditions for comparable obligations prevalent prior to the outbreak of the coronavirus disease, and (2) be for a term "as short as practicable and in any case not longer than 5 years." No such loan is eligible for loan forgiveness.

In addition, the Secretary must, as part of the terms of the loan or loan guarantee, receive (a) if the eligible business has issued securities that are traded on a national securities exchange, a warrant or equity interest in the eligible business receiving the loan or the benefit of the loan guarantee, or (b) for other businesses, a warrant or equity interest in the eligible business or a senior debt instrument issued by the eligible business. For eligible businesses in the first category, the Secretary is authorized to take a senior debt instrument upon concluding that the eligible business cannot feasibly issue warrants or equity interests. For the benefit of the American taxpayer, any such warrant or equity interest is to provide an equity appreciation, and any such senior debt instrument is to provide a reasonable interest rate premium. It is indicated that the Secretary would not exercise any voting power with respect to any equity so acquired, but the Secretary is free to sell such interests, and it is unclear whether the intent is that such securities, once sold, could be voting securities.

Additional Conditions: Any business receiving a loan is restricted in its activities for a period through the date 12 months after the loan or loan guarantee is no longer outstanding. During that period, the business (1) may not pay dividends or make other capital distributions with respect to its common stock, and (2) may not (directly or through an affiliate) purchase any of its equity securities (or equity securities of a parent) that are listed on a national securities exchange, unless pursuant to a contract in place before adoption of the CARES Act.

In addition, the borrower must, through September 30, 2020, maintain its employment levels at the same levels that existed as of March 24, 2020, to the extent practicable, and in any case shall not reduce its employment levels by more than 10% from the levels as of such date.

Further, from the date the loan agreement is executed through the date one year after the date on which the loan or loan guarantee is no longer outstanding, executive compensation is restricted as follows: (i) Except as otherwise mandated pursuant to a collective bargaining agreement entered into prior to March 1, 2020, no officer or employee receiving "total compensation" (including salary, bonuses, awards of stock and other financial benefits) in excess of $425,000 in 2019 may receive compensation in excess of such amount received in 2019 during any 12-month period while such restrictions are in place, or receive severance payments in excess of twice that amount; and (ii) no officer or employee whose total compensation exceeded $3,000,000 in 2019 may receive, during any such 12-month period, compensation in excess of $3,000,000 plus 50% of the excess over $3,000,000 received in 2019. The Secretary of Transportation is authorized, through March 1, 2022, to require any air carrier receiving a loan or the benefit of a loan guarantee to maintain scheduled air transportation service as the Secretary of Transportation deems necessary to ensure services to any point serviced by such air carrier prior to March 1, 2020. A similar requirement regarding the maintenance of air transportation service applies to air to air carriers receiving the support grants described under "Air Carrier Worker Support" below. On April 7, 2020, the Department of Transportation issued an order prescribing the minimum flight requirements that will apply through September 30, 2020.

Applicable Procedures: Preliminary procedures and requirements for loans for air carriers were announced on March 30, 2020, with a statement that such procedures and requirements will be supplemented with additional procedures and a loan application form, and such procedures may be modified at any time. The requirements identified in the announcement merely set out those already included in the statute as described above, but the announcement provided a preview of information that would be required to obtain a loan. Loan guarantees were not addressed.

As part of the loan application process, a prospective borrower will be required to provide information regarding (1) the borrower's existing secured and unsecured debt, its bank and other credit lines with outstanding maximum balances, and the major classes of existing security holders and creditors; (2) the borrower's scheduled debt service for the next three months; (3) the borrower's employment levels, by head count and total compensation, as of March 24, 2020, and proposed changes thereto during 2020; (4) the borrower's consolidated financial statements for the previous 3 years; (5) the covered losses incurred or expected to be incurred by the borrower; (6) evidence that the borrower cannot obtain credit elsewhere; (7) for passenger air carriers, the available seat miles, revenue per seat mile, and cost per available seat in 2019, and for cargo air carriers, available ton miles, revenue per ton mile, and cost per available ton mile for 2019, and in each case a forecast of the same for 2020; (8) a description of security available to be pledged for the loan, (9) the proposed use of proceeds; (10) quantitative information on the borrower's financial needs for the remainder of 2020; (11) an operating plan for the remainder of 2020; and (12) a description of any plans for restructuring the borrower's obligations, contracts, staffing, or organization to improve its financial condition. The borrower is also expected to present a description of the warrants or equity interests, or the senior debt obligations, it proposes to issue to the Treasury Department.

The Treasury Department is expected to coordinate with the Department of Transportation, and Treasury may reveal any information it receives to the Department of Transportation.

Air Carrier Worker Support

In addition to the loan and loan guarantee provided to air carriers in Subtitle A of Title IV of the CARES Act, Subtitle B of Title IV provides financial assistance in the form of support grants for the exclusive use of employee wages, salaries, and benefits up to the following amounts: (1) $25 billion for passenger air carriers, (2) $4 billion for cargo air carriers, and (3) $3 billion for airline contractors (defined as airport ground support or catering services for the air carrier industry).

The awardable amount equals salaries and benefits reported pursuant to 14 CFR Part 241 for the period from April 1, 2019, through September 30, 2019, and for those who do not report pursuant to 14 CFR Part 241, self-certified amount of wages, salaries, benefits, and other compensation for the same time period. Approved applicants may receive payroll support in multiple payments, with the amounts and timing of such payments to be at Treasury's discretion.

Treasury has published guidelines and application procedures, with applications due April 3, 2020 (applications submitted after that date will be considered but may not be approved as quickly).

To be eligible to receive payments, an applicant must agree to:

- use such payments exclusively for the continuation of employee wages;

- refrain from conducting involuntary layoffs or furloughs, or reducing pay rates and benefits, of employees of the applicant and its subsidiaries until September 30, 2020;

- through September 30, 2021, ensure that neither the applicant nor any subsidiary or affiliate purchases, in any transaction, an equity security of the applicant or the direct or indirect parent company of the applicant that is listed on a national securities exchange; and

- through September 30, 2021, ensure that the applicant does not pay dividends, or make other capital distributions, with respect to common stock (or equivalent interest) of the applicant or any subsidiary thereof.

A number of other conditions apply, including those relating to protecting collective bargaining agreements, limiting employee compensation, and protecting taxpayers by authorizing Treasury to receive financial compensation in the form of warrants, options, preferred stock, debt securities, notes, or other financial instruments issued by recipients of payroll support. On April 10, 2020, the Treasury Secretary announced that Treasury will not require such financial compensation from air carriers receiving $100 million or less in payroll support. However, for those receiving above $100 million, the Treasury would offer 70% in aid as grants that would not need to be repaid, and 30% in low-interest loans for which the air carriers would have to offer warrants. The warrants would give the government the right to buy equity at a pre-set price and time, and would be equal to 10% of the value of the loan.

To be eligible for payroll support, an applicant must complete the Payroll Support Application Form and submit a proposal identifying a financial instrument and proposed terms that would provide appropriate compensation to the government in exchange for payroll support. An applicant must also complete a Payroll Support Agreement, which will be provided by the Treasury Department after an application is received. The Payroll Support Agreement will include terms addressing:

- assurances described above;

- employee compensation limits;

- certain other conditions and covenants: and

- clawback of payments upon the applicant's failure to satisfy its assurances, conditions, or agreements.

With respect to companies seeking access to the $17 billion allocated to companies that are deemed critical to national security under the CARES Act, the Secretary of the Treasury is requiring as part of the loan application that in order to get a loan, borrowers provide the Treasury Department with appropriate financial instruments that in the Secretary's sole determination, provide for a reasonable participation in equity appreciation or a reasonable interest rate premium appropriate for the benefit of taxpayers. In this regard, borrowers that are publicly traded companies will be required to provide warrants or other equity interest unless the Secretary determines that the Borrower cannot feasibly do so. For other borrowers, the Secretary may in its discretion accept senior debt instruments or warrants or other equity interests.

PAYCHECK PROTECTION PROGRAM

Section 1102 of the Act amends the Small Business Act to create the Paycheck Protection Program (PPP). The PPP is a multibillion expansion of the loan program created under section 7(a) of the Small Business Act that is intended to keep small businesses solvent and workers on payrolls. Under the PPP, private lenders can originate loans of up to $10 million to small businesses, nonprofits, tribal concerns, sole proprietorships, independent contractors, self-employed individuals, and veteran organizations. The loans are fully guaranteed by the Small Business Administration (SBA) and, ultimately, by the US Treasury and may be fully forgiven when used for payroll costs, interest on mortgages, rent, and utilities. For the loan to be fully forgiven, borrowers must maintain (or quickly rehire) staff and their salaries at prescribed levels. Under the terms of the PPP as originally established in the CARES Act, loan payments were to be be suspended for the first six months, although this deferral period has since been extended under the Paycheck Protection Flexibility Act (Flexibility Act), as described below. Despite the payment deferral, interest continues to accrue. In addition, no collateral or personal guarantees are required.

On May 16, the SBA released its PPP loan forgiveness application and related instructions. On May 22, the SBA issued an interim final rule which provides additional guidance regarding the loan forgiveness process and certain aspects of the loan forgiveness calculation. The application is submitted to the lender, and not to the SBA. Although the application and the interim final rule provides detailed instructions regarding the loan forgiveness calculation, questions will inevitably arise that may require further guidance.

On May 21, the SBA released detailed guidance regarding PPP lender processing fee payments and the Form 1502 reporting process. As explained below, the SBA will pay lenders a fixed fee for processing loans based upon the balance of the PPP loan outstanding at the time of full disbursement. Under PPP, lenders have a monthly obligation to report any PPP loans that have been fully disbursed and/or cancelled in the Lender's Fiscal Transfer Agent (FTA) Lender Portal. The SBA will make PPP processing fee payments to Lenders using the Demand Deposit Account ACH information supplied by lenders in the FTA Lender Portal. The lender processing fees are subject to clawback if the SBA determines within one year after the loan was disbursed that a borrower was ineligible to receive the PPP loan. Lenders must electronically submit Form 1502 reporting information to the SBA by the later of: (1) May 29, 2020; or (2) ten calendar days after disbursement or cancellation of a PPP loan.

Originally, Congress allocated $349 billion in funding to the PPP under the Act, to be administered by the SBA and the U.S. Treasury. However, after the program was depleted of funds in under a month, Congress approved an additional $310 billion in funding for the program as part of the total $484 billion rescue package under the Paycheck Protection Program and Health Care Enhancement Act enacted on April 24, 2020.2 The total amount of funding that has been allocated to the PPP to-date is approximately $660 billion. As of June 3, 2020, over $140 billion of funds remained available. On May 28, the SBA and the Treasury Department announced that $10 billion of the second round of PPP funding is being set aside exclusively for lending by Community Development Financial Institutions (CDFIs).

On June 5, 2020, the President signed into law the Flexibility Act (H.R. 7010). As its name implies, the Flexibility Act made a number of amendments to the PPP to liberalize its application in response to claims that many of the PPP's provisions were too restrictive. Amendments in the Flexibility Act:

- Extend the minimum loan term from the SBA-imposed two-year maturity date to five years for PPP loans made after the date of enactment. However, lenders and borrowers would not be prohibited from mutually agreeing to modify the maturity terms of PPP loans disbursed prior to this date;

- Extend the deadline to apply for PPP loans from June 30 to December 31, 2020 (One Senator attempted to retain the original June 30 deadline for new applications by have the Senate Small Committee Chairman and Ranking Member sign a letter reflect this intent, but the letter is not binding);

- Extend the "covered period" for loan forgiveness from eight weeks following disbursement of the loan to 24 weeks or December 31, 2020, whichever is earlier. (A borrower who received a PPP loan before enactment of the Flexibility Act could elect to continue using the eight-week covered period);

- Extend the CARES Act's deadline to rehire employees and reverse salary cuts of greater than 25 percent from June 30 to December 31, 2020;

- Exempt borrowers from the

proportional reduction in loan forgiveness due to a reduction in

employees, if the borrower is able to document in good faith that

for the period of February 15 to December 31, 2020, the borrower

was unable to:

- either rehire employees who were employed on February 15, 2020 or hire similarly qualified employees for unfilled positions by December 31, 2020; or

- return to the same level of business activity as the business was operating at before February 15, 2020 due to compliance with federal requirements or guidance issued between March 1 and December 31, 2020 related to standards for sanitation, social distancing, or any other COVID19 related worker or customer safety requirement.

- Lower the amount of PPP loan proceeds that must be used for payroll costs to qualify for loan forgiveness from 75 percent to 60 percent (There was some concern that the language of the Flexibility Act changed the PPP proportional forgiveness provision for borrowers who fail to meet the payroll spending threshold to an all-or -nothing threshold; however, the Administration agreed to interpret and implement the Flexibility Act to avoid creating a loan forgiveness cliff);

- Replace the six-month deferral period with deferral until the date on which the forgiveness payment is remitted to the lender. A borrower who fails to apply for loan forgiveness within 10 months after the last day of the "covered period" would be required to begin making payments of principal, interest and fees on the PPP loan; and

- Allow borrowers who receive PPP loan forgiveness to defer payroll taxes incurred between March 27 and December 31, 2020.

It is anticipated that SBA documents, including FAQs, will be modified to address these amendments. All FDIC-insured depository institutions and NCUA insured credit unions, as well as all SBA-licensed 7(a) bank and nonbank lenders are eligible to participate as lenders in the PPP program, by filing a special form with the SBA. Other nonbank lenders may also seek SBA approval to participate as lenders. PPP loan applications are made on a new SBA form and submitted by SBA-approved participating lenders to the SBA through a web-based portal for review and approval pursuant to SBA protocols, which generates an approval notice to the lender.

The terms of PPP loans are dictated by Treasury Rules and SBA guidance on the PPP program, as well as the statute and the terms in the notice of loan approval from the SBA.

Lenders may not charge fees to borrowers. The interest rate on all loans will be one 1%. The SBA will pay lenders for processing PPP loans in the following amounts:

- 5% for loans of not more than $350,000

- 3% for loans of more than $350,000

- 1% for loans of at least $2,000,000

Treasury also rules contemplate lenders paying agents that provide certain services in connection with PPP loans, subject to certain limitations and disclosure requirements. Agent fees are to be paid out of lender fees and may not be collected from the applicant. Treasury guidance provides that agent fees for assistance in preparing PPP applications may not exceed:

- 1% for loans of not more than $350,000

- 0.5% for loans of more than $350,000

- 0.25% for loans of at least $2,000,000

PPP lenders must comply with applicable SBA and Bank Secrecy Act (BSA) requirements, but are otherwise held harmless for borrowers' failure to comply with Program criteria. The Financial Crimes Enforcement Network has issued guidance specifically addressing BSA compliance in the context of the CARES Act generally and the PPP specifically, which can be found here. Treasury guidance provides reassurance to lenders that they can rely on representations and certifications by borrowers of eligibility for PPP loans. Many lenders are nonetheless wary that they will be held responsible for applicants' errors or misstatements in PPP loan applications.

Recent guidance from SBA, Treasury, and federal banking regulators have added to many lenders' degrees of skepticism. The recent guidance signals that each of those government agencies will review the lending practices and implementation of the PPP by lenders. For example, on April 27, 2020, the Office of the Comptroller of the Currency stated in OCC Bulletin 2020-45, "[w]hile not requiring banks to obtain or maintain information beyond what exists in the ordinary course of business, the OCC is encouraging banks providing loans under the SBA PPP to prudently document their implementation and lending decisions." Moreover, as described below, SBA and Treasury have stated that actions of lenders and borrowers may be subject to scrutiny over the coming months. In addition, on May 22, 2020, the SBA published an interim final rule regarding the SBA's loan review procedures and the responsibilities of borrowers and lenders in connection with such procedures.

Even before the second appropriation of PPP funds, accounts of perceived flaws in the PPP process received widespread attention. These included reports that larger companies, including publicly traded corporations, were able to obtain PPP loans, diverting funds from the smaller businesses that were intended to be the beneficiaries of the program. At the same time there were stories about bank lenders, particularly large banks, favoring existing larger customers at the expense of smaller customers or potential borrowers with no previous connection to the banks. These stories have resulted in new litigation, including purported class action suits, against lenders, borrowers, and the SBA itself. In one recent example, the U.S. Court of Appeals for the Sixth Circuit upheld a lower-court preliminary injunction granted to the owners of certain "sexually oriented" (but lawful) businesses who challenged an SBA rule making them ineligible for PPP loans.3 Additional information about litigation-related activities can be found here. The stories also contributed to the decision to set aside in the second round of funding $30 billion allocated specifically to community banks, credit unions and other lenders, and $30 billion allocated to medium-sized banks and credit unions.

The U.S Government Accountability Office, members of Congress, the SBA and Treasury have all raised concerns and indicated that, going forward, actions of lenders and borrowers will face enhanced scrutiny. For example, Senator Rubio, chairman of the Senate Committee on Small Business, sent a letter to the nation's largest lenders urging them to "ensure a neutral distribution of assistance" amid "reports of priority being given to certain applicants over others." Treasury Secretary Steven Mnuchin has made public comments discouraging larger companies, especially those with access to capital markets and other sources of liquidity for ongoing operations, from applying for loans under PPP. The borrower applications for PPP loans include certifications as to the planned use of the proceeds and the necessity to the borrower of obtaining the funds. Additionally, under Treasury's guidance for the PPP issued on April 23 (FAQ No. 31), 2020, borrowers were reminded of the requirement that they make a good faith certification of the need for a PPP loan, taking into account other available sources of liquidity. Public companies and larger companies with adequate sources of liquidity were advised to not apply for PPP loans and, as a "safe harbor," were given the opportunity to repay PPP loan proceeds before May 7, 2020, if they determined that they were not in compliance with the good-faith certification. Additionally, on April 28, 2020, during a news conference, Treasury Secretary Steven Mnuchin stated that small business loans above $2 million will be subject to a full audit to make sure that they are valid.4 The U.S. Department of Justice has been conducting an ongoing review of PPP lending, and on May 14, 2020, the U.S. Department of Justice announced that it had charged an individual in Georgia with misuse of funds from a PPP loan and an individual in Texas with making fraudulent PPP loan applications. There also have been reports of the SEC inquiring into publicly traded companies that received PPP funding to determine whether representations by the companies as part of their PPP applications were consistent with their SEC filing disclosures.

FAQ No. 31 raised a number of questions among borrowers who had received PPP loan funds and were unsure how to interpret Treasury's guidance regarding the need certification. This uncertainty caused a sense of paralysis among borrowers who were unable to determine, in light of FAQ No. 31, whether to begin to spend the PPP loan funds for their intended purposes, including rehiring employees, or return the loan to the SBA. On May 5, 2020, Treasury published FAQ No. 43, which extended the safe harbor deadline for repaying PPP loans to May 14, 2020. On May 13, 2020, Treasury published FAQ No. 46 which provides that any borrower that (together with any affiliates that must be included pursuant to the affiliation rules applicable to PPP loans) received PPP loans of less than $2,000,000 would be deemed to have made the need certification in good faith. In addition, borrowers that do not return PPP loans and are subsequently determined by the SBA to have lacked an adequate basis for making the need certification will be asked to return the loan with no possibility for loan forgiveness. If such borrowers return the loans as requested, the SBA will not take any administrative enforcement action against them or refer the matter to other agencies for enforcement in respect of the need certification. Treasury has also further extended the safe harbor deadline for repayment of PPP loans to May 18, 2020.

After being fully disbursed, PPP loans may be sold in the secondary market (if one develops), and the SBA will not collect any fees for any loan or guarantee sold. Lenders began processing PPP loan applications on April 3, 2020, and the SBA is authorized to guarantee PPP loans originated through December 31 2020 or until funds run out, on a first-come, first-served basis. As of the date of this advisory, however, even the second round of available PPP funds has almost been exhausted.

In order to promote PPP lending, the Federal Reserve has established a PPP Loan Financing Facility, which is discussed below. More recently, the Federal Reserve has temporarily modified its rules restricting the types and quantities of loans that bank directors, shareholders and officers, and businesses owned by these persons can receive from their related banks to permit these banks to make PPP loans to businesses owned by their directors and certain shareholders, subject to certain limits and without favoritism.

In addition, on April 7, 2020 the federal banking agencies adopted an interim final rule to neutralize the regulatory capital effects of banking organizations participating in the Facility. More information about the capital relief is provided here.

For a more detailed description of the PPP, see our prior Advisories: Small Business Loan Relief From CARES Act and Analysis of CARES Act for Non-Profit Organizations.

FEDERAL RESERVE ACTIONS TO FACILITATE LENDING AND LIQUIDITY

The Federal Reserve has taken several actions to stabilize the economy, including using its emergency lending authority to establish broadly based facilities to lend to financial institutions and eligible US businesses and shore up liquidity in the markets. Among its actions to date in its role as the US Central Bank, the Federal Reserve has (1) reduced the federal funds rate to 0% to 25%; (2) agreed to purchase an unlimited amount of Treasury securities and agency mortgage-backed securities (MBSs), including agency commercial MBSs, to support smooth market functioning and effective transmission of monetary policy; (3) established three lending facilities under a Main Street Lending Program to complement efforts by the SBA and support lending to eligible small and medium-sized businesses; (4) established a lending facility to facilitate lending to small businesses under the SBA's PPP by providing term financing backed by PPP loans to financial institutions that are PPP lenders; and (5) established other liquidity facilities similar to those established under the 2008 Financial Crisis, including facilities that allow eligible borrowers to restructure their loans generally using investment grade collateral.

The new facilities are summarized below. In the interest of transparency and accountability around financial reporting and policymaking, the Federal Reserve has stated that it will provide monthly public reports on its liquidity and lending facilities that use CARES Act funding, and the reports will contain substantial amounts of information, including (i) names and details of participants in each facility; (ii) amounts borrowed and interest rates charged; (iii) overall costs, revenues and fees for each facility. The Federal Reserve has also made it clear that it is prepared to use the full range of tools at its disposal to support the flow of credit to businesses and consumers in furtherance of its goals of maximum employment and price stability.

Primary Market Corporate Credit Facility (PMCCF): Under this facility, the Federal Reserve will (i) purchase eligible corporate bonds as the sole investor in a bond issuance: and (ii) purchase portions of syndicated loans or bonds at issuance. The Department of the Treasury will make a $75 billion equity investment, using funding from Title IV of the CARES Act, to support both the PMCCF and the Secondary Market Corporate Credit Facility (SMCCF) described below. The initial equity allocation will be $50 billion to the PMCCF and $25 billion to the SMCCF. The combined size of the two Facilities will be up to $750 billion. Corporate bonds eligible for purchase by the PMCCF as sole purchaser must be issued by and eligible issuer and have a maturity of four years or less. PMCCF purchases of portions of syndicated loans and bonds are subject to the same requirements. In addition, the PMCCF cannot purchase more than 25% of any issuance of syndicated loans and bonds. An eligible issuer is a business that is created or organized in the US or under the laws of the US with significant operations in and a majority of its employees based in the US. Businesses using this facility must have investment-grade credit (rated BBB-/Baa3 or higher) as of March 22, 2020. Issuers rated at least BBB-/Baa3 as of March 22, 2020 but are subsequently downgraded must be rated at least BB-/Ba3 at the time the PMCCF makes a purchase. In every case, issuer ratings are subject to Federal Reserve review.

Under the PMCCF, the issuer may not be an insured depository institution or depository institution holding company, as those terms are defined in the Dodd-Frank Act, and cannot have received any specific support pursuant to the CARES Act or any subsequent federal legislation. In addition, the issuer must satisfy the conflicts-of-interest requirements of Section 4019 of the CARES Act (none of the President, Vice President, executive department head, member of Congress, or their immediate families may own over 20% or more of the equity of an entity). The maximum amount of outstanding bonds or loans of an eligible issuer that borrows from the PMCCF may not exceed 130% of the issuer's maximum outstanding bonds and loans on any day between March 22, 2019 and March 20, 2020. The maximum amount of instruments that the PMCCF and the SMCCF combined may purchase with respect to any eligible issuer is capped at 1.5% of the combined potential size of the two facilities. The PMCCF will cease purchasing eligible assets no later than September 30, 2020, unless the Facility is extended by the Federal Reserve and the Treasury Department. See term sheet here and the Frequently Asked Questions (FAQs) here.

Secondary Market Corporate Credit Facility (SMCCF): The SMCCF is intended to provide liquidity to existing bondholders. The SMCCF will purchase in the secondary market individual eligible corporate bonds and eligible corporate bond portfolios in the form of exchange-traded funds (ETFs). The Treasury Department will make an equity investment as described in the PMCCF analysis above. The SMCCF may purchase corporate bonds issued by an eligible issuer, have a remaining maturity of five years or less, and were sold to the SMCCF by an eligible seller. The requirements to qualify as an eligible issuer are substantially the same as those to qualify under the PMCCF, as described above. In order to qualify as an eligible seller, the institution must be a business that is created or organized in the US or under the laws of the US, with significant US operations and a majority of US-based employees. The institutions also must satisfy the conflicts-of-interest requirements of Section 4019 of the CARES Act described above. The SMCCF may also purchase certain US-listed ETFs whose investment objective is to provide broad exposure to the market for US corporate bonds. The preponderance of ETF holdings will be ETFs whose primary investment objective is exposure to US investment-grade corporate bonds, with the remainder in ETFs whose primary investment objective is exposure to US high-yield corporate bonds. The maximum amount of bonds of any single issuer that the SMCCF will purchase from the secondary market is capped at 10% of the issuer's maximum bonds outstanding on any day between March 22, 2019 and March 22, 2020, and the SMCCF will not purchase any shares of a particular ETF if the purchase would result in the Facility holding more than 20% of the ETF's outstanding shares. The SMCCF commenced its purchase of ETFs on May 12, 2020. The SMCCF will cease purchasing eligible corporate bonds and ETFs no later than September 30, 2020, unless the SMCCF is extended by the Federal Reserve and the Treasury Department. See term sheet here and updated FAQs here.

Term Asset-Backed Securities Loan Facility (TALF): Under this facility, the Federal Reserve Bank of New York (New York Fed) will initially make available, through a special-purpose vehicle, up to $100 billion of loans to eligible borrowers (generally at the 30-day secured overnight financing rate (SOFR) plus 1.50%), with the first subscription date occurring on June 17, 2020. This lending will be supported by an equity investment of $10 billion by the Treasury Department. The loans will have a 3-year term, will be nonrecourse to the borrower, and will be fully secured by eligible asset-backed securities (ABS), based upon specified advance rates. All US companies that own eligible collateral and maintain an account relationship with a primary dealer are eligible to participate (subject to certain limitations). US company is defined as a business created or organized in the US or under the laws of the US that has significant operations in and a majority of its employees based in the US (generally determined on a consolidated basis, but taking into account only downstream affiliates, not parent or sister entities) and includes investment funds with managers that are US companies. In order to be eligible, ABS must be (among other requirements) AAA-rated, USD-denominated and backed by USD-denominated automobile loans and leases (including fleet leases to rental car companies), student loans, credit card receivables, loans and leases relating to equipment (excluding aircraft, shipping containers, ships, cell phone towers, locomotives and railcars), floorplan loans, premium finance loans for property and casualty insurance, certain SBA-guaranteed small business loans, leveraged loans (thereby permitting static collateralized loan obligations (CLOs)) or commercial mortgages. With the exception of commercial mortgage-backed securities (CMBS), eligible ABS must be issued on or after March 23, 2020 (or, in the case of certain SBA certificates, January 1, 2019). Only CMBS issued before March 23, 2020 will be eligible for this facility. Also, for CMBS to be eligible, the underlying credit exposures must be to real property located in the US or one of its territories. Eligible collateral does not include ABS with interest payments that step up or step down to predetermined levels on specific dates, or whose underlying exposures include synthetic assets or other ABS. Eligible borrowers will be subject to the conflicts-of-interest requirements of Section 4019 of the CARES Act (described above), may not be the ABS issuer, an originator of the underlying credit exposures or an affiliate thereof and will be required to make certain certifications (including as to its inability to secure "adequate credit accommodations" from other banking institutions). On May 20, 2020, the New York Fed released a Master Loan and Security Agreement, under which the TALF loans would be made (including certifications to be made by the ABS issuer and sponsor, and by the borrower, linked here, here and here), and a revised set of FAQs relating to the program. Certain key terms of TALF II are also summarized in a term sheet. The New York Fed also announced on May 12, 2020 that it will disclose, on a monthly basis, the name of each TALF participant; the amounts borrowed, interest rate charged, and value of pledged collateral; and the overall costs, revenues, and fees for the Facility.

Money Market Mutual Fund Liquidity Facility (MMLF): Under this facility, the Federal Reserve will lend to US depository institutions, US bank holding companies (and their US broker-dealer subsidiaries), and US branches and agencies of foreign banks. Eligible collateral will be limited to certain types of assets purchased by the borrower from a money market fund. The types of assets that may serve as eligible collateral include US Treasuries and Fully Guaranteed Government Securities, securities issued by the Government Sponsored Enterprises, highly-rated municipal short-term debt, and secured and unsecured commercial paper. No new credit extensions will be made after September 30, 2020, unless the facility is extended by the Federal Reserve. On March 23, 2020, the bank regulatory agencies adopted an interim final rule to neutralize the regulatory capital effects of banking organizations participating in the program. See term sheet here. On May 12, 2020, the FDIC issued a Notice of Proposed Rulemaking to mitigate the deposit insurance assessment effects of participating in the MMLF, the PPP, and the PPPL, with a proposed effective date by June 30, 2020 and an application date of April 1, 2020, in order to cover the second quarter of the year.

Municipal Liquidity Facility (MLF): The MLF will provide funding and liquidity directly to state and local governments. The MLF will purchase Eligible Notes from Eligible Issuers at the time of issuance. Originally, Eligible Notes were certain short-term notes with maturities not to exceed 24 months issued by Eligible Issuers, and Eligible Issuers included US states and the District of Columbia, US cities with a population exceeding 1 million residents, and US counties with a population exceeding 2 million residents. On April 27, the Federal Reserve revised the terms of the MLF to increase the maximum maturity to 36 months and decrease the population thresholds for cities and counties to 250,000 and 500,000, respectively. The Treasury Department will make an initial equity investment of $35 billion and the MLF have the ability to purchase up to $500 billion of Eligible Notes. Under the revised terms, the MLF will cease purchasing Eligible Notes on December 31, 2020, unless the Federal Reserve and the Treasury Department extend the Facility.

On June 3, 2020, the Federal Reserve announced an expansion of the number and type of entities eligible to directly use the MLF. As described in the revised term sheet, all U.S. States will be able to have at least two cities or counties eligible to directly issues notes to the MLF, regardless of population; otherwise, the 250,000 and 500,000 population thresholds still apply. Governors of each state also will be able to designate two issuers in their jurisdictions whose revenues generally are derived from operating government activities (such as public transit, airports, toll facilities, and utilities) to be eligible to directly use MLF. The Federal Reserve addressed this expansion in FAQs also issued on June 3.

Commercial Paper Funding Facility (CPFF): This facility is structured as a credit facility to a special purpose vehicle (SPV), and the SPV will serve as a funding backstop to facilitate the issuance of term commercial paper by eligible issuers. The SPV will purchase investment-grade 3-month dollar-denominated commercial paper from eligible US issuers (including US issuers with a foreign parent company). The SPV will cease purchasing commercial paper on March 17, 2021, unless the Federal Reserve extends the facility. The New York Fed will continue to fund the SPV until its underlying assets mature. See term sheet here and FAQs here.

FIMA Repo Facility: This is a temporary repurchase agreement facility for foreign and international monetary authorities to help the smooth functioning of financial markets, including the US Treasury market. Under the FIMA Repo Facility, FIMA account holders (i.e., central banks and other international monetary authorities with accounts at the New York Fed) will be able to enter into repurchase agreements with the Federal Reserve, whereby the FIMA account holder temporary exchanges their US Treasury securities for US dollars. See FAQs here.

Note that the Federal Reserve, along with the Bank of Canada, the Bank of England, the Bank of Japan, the European Central Bank, and the Swiss National Bank have agreed to coordinate actions to further enhance the provision of US dollar liquidity. These central banks have agreed to increase the frequency of 7-day maturity operations from weekly to daily. The operations began on March 23, 2020, and are expected to continue at least through the end of April. The swap lines among these central banks serve as an important liquidity backstop to ease strains on global funding markets, and thereby help mitigate the effects of such strains on the supply of credit to households and businesses domestically and abroad.

Primary Dealer Credit Facility (PDCF): This facility will allow primary dealers to support smooth market functioning and facilitate the availability of credit to businesses and households by offering overnight and term funding with maturities up to 90 days. Eligible collateral for primary dealers includes a broad range of investment grade debt securities, including commercial paper, municipal bonds and equity securities. This facility will be available until September 2020, unless economic conditions warrant a longer availability. See term sheet here.

PPP Loan Financing Facility. On April 6, 2020 Federal Reserve announced a new facility, the Paycheck Protection Program Liquidity Facility (PPPLF), that will facilitate lending to small businesses via the PPP by providing term financing backed by PPP loans. Many nonbank SBA lenders do not have sufficiently large balance sheets to carry the volume of PPP loans they expect to originate, and there is not currently a functioning secondary market in PPP loans (although one may develop). This facility is intended to bridge that funding shortfall by permitting lenders to obtain financing from the Federal Reserve of their PPP loans, taking the loans as collateral at face value. On April 9, 2020, the Federal Reserve released a term sheet describing the terms of the PPPLF. See PPPLF term sheet here. Also, as described above in the summary of the PPP program, the federal banking agencies have provided specific capital relief in connection with PPP lending. On May 12, 2020, the Federal Reserve announced that it will disclose, on a monthly basis, the name of each PPPLF participant; the amounts borrowed, interest rate charged, and value of pledged collateral; and the overall costs, revenues, and fees for the Facility. Also On May 12, 2020, the FDIC issued a Notice of Proposed Rulemaking to mitigate the deposit insurance assessment effects of participating in the MMLF, the PPP, and the PPPL, as described above under Money Market Mutual Fund Liquidity Facility (MMLF).

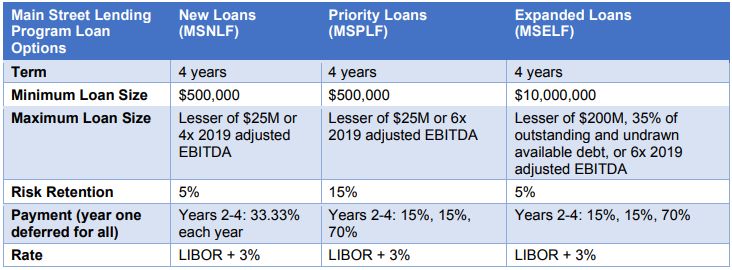

Main Street Lending Program (MSNLF, MSELF, and MSPLF): On April 9, 2020, the Federal Reserve announced the terms of a Main Street New Loan Facility (MSNLF) and a Main Street Expanded Loan Facility (MSELF) to implement its Main Street Lending Program. On April 30, 2020, the Federal Reserve expanded the scope and eligibility of businesses that may participate in these facilities and announced the creation of a third facility, the Main Street Priority Loan Facility (MSPLF).

Under the MSNLF, MSELF and MSPLF, "eligible lenders" are U.S.-insured depository institutions (including banks, savings associations and credit unions), U.S. branches and agencies of foreign banks, U.S. bank and savings and loan holding companies, U.S. intermediate holding companies of foreign banking organizations, and U.S. subsidiaries of any of the foregoing. "Eligible borrowers" are businesses created in the U.S. or under the laws of the U.S. (prior to March 13, 2020) with significant operations and a majority of its employees in the U.S. Additionally, borrowers must meet either an employee or an annual revenue threshold: (i) 15,000 or less employees, or (ii) no more than $5 billion in 2019 annual revenue. Prior to the April 30th expansion of the program, the limits for employees and annual revenue were 10,000 and $2.5 billion, respectively. As part of the April 30th changes, the Federal Reserve added to the borrower eligibility criteria that borrowers must not have received specific support under Subtitle A of Title IV of the CARES Act, but notes that this restriction does not prohibit businesses that have received PPP loans, provided that the business is otherwise an eligible borrower. Another eligibility requirement for borrowers is that the borrower is not of the type of entity that is ineligible for an SBA loan under 13 CFR 120.110(b)-(j) and (m)-(s) (citation excludes nonprofits and religious institutions) as modified by regulations for the PPP. However, the Federal Reserve notes that the application of this restriction may be further modified at the agency's discretion. The combined size of the MSNLF, MSELF, and MSPLF will be up to $600 billion. The Treasury Department will make a $75 billion equity investment using CARES Act funds. Borrowers may only participate in one of the three Main Street Lending Program facilities, and borrowers of the MSNLF, MSELF, or MSPLF may not participate in the PMCCF.

Under both the MSNLF and the MSELF, the Federal Reserve through a special purpose vehicle ("SPV") will purchase 95% participations in eligible loans from eligible lenders, with the eligible lenders retaining the remaining 5%. The 5% is viewed as a risk retention component of the loan. Under the MSPLF, which is for new loans to businesses with higher leverage amounts than those eligible for the MSNLF, the SPV will purchase 85% participations in eligible loans, and lenders will be expected to retain the remaining 15%. According to the FAQs released on April 30th, the eligible lender would be required to retain its participation interest until the applicable loan matures or the SPV sells off all of its participation, whichever comes first. Under all three facilities, "eligible loans" are secured or unsecured term loans made by an "eligible lender" that have: (i) a 4-year maturity; (ii) principal and interest payments deferred for one year (but with accrued and interest added to principal); and (iii) interest accrued at an adjustable rate of LIBOR plus 3% (prior to the April 30th changes, the rate was SOFR plus 250-400 basis points).

Under the lending facilities for loans originated after April 24, 2020 (i.e. MSNLF and MSPLF), the minimum loan size is now $500,000 (reduced from $1 million minimum that was set previously for the MSNLF), and the maximum loan size is the lesser of (i) $25 million, or (ii) an amount that, when added with the eligible borrower's existing outstanding and committed but undrawn debt does not exceed four times the eligible borrower's 2019 adjusted EBITDA for the MSNLF, or six times the eligible borrower's 2019 adjusted EBITDA for the MSPLF. Aside from the difference in leverage thresholds, the MSNLF and MSPLF have different criteria for the priority of eligible loans under each facility. Under the MSNLF, at the time of origination or at any time during the loan term, eligible loans must not be contractually subordinated in terms of priority to any other loans or debt instruments of the eligible borrower. Eligible loans under the MSPLF at the time of origination and at all times thereafter must be senior to or pari passu with, in terms of priority and security with any other loans or debt instruments of the eligible borrower, other than mortgage debt.

Loans from eligible lenders to eligible borrowers that were originated on or before April 24, 2020 may qualify for "upsizing" pursuant to the MSNLF, so long as the underlying loan has a maturity (taking into account any extensions at or prior to upsizing) of at least 18 months. Under the MSNLF, eligible lenders are able to increase an eligible borrower's existing term loan or revolving credit facility with the eligible lender, whether secured or unsecured, by adding a new tranche. The upsized tranche is a four-year term loan ranging in size from $10 million to $200 million (increased from $150 million under the April 30th expansion of the Main Street Lending Program). The maximum loan size for any eligible borrower may not, however, be greater than the lesser of (i) 35% (increased from 30% under the April 30 expansion) of the eligible borrower's existing outstanding and committed but undrawn debt that is pari passu in priority with the eligible loan and equivalent in secured status, or (ii) an amount that, when added to the eligible borrower's existing and outstanding and committed but undrawn debt does not exceed six times the eligible borrower's adjusted 2019 EBITDA. At the time of upsizing and at all times thereafter the upsized tranche must be senior to or pari passu with, in terms of priority and security, the eligible borrower's other loans or debt instruments, other than mortgage debt.

Below is a chart summarizing the loan options under each of the Main Street Lending Program facilities.

Under all three of the facilities, eligible borrowers and eligible lenders are required to provide a number of certifications and commitments to the Federal Reserve, including (i) that loan proceeds will not be used to pay existing debt (except that, under the MSPLF, the proceeds may be used to refinance debt owed to a lender that is not the eligible lender providing the MSPLF loan), (ii) the eligible borrower will not prepay other debt until the new loan (or upsize tranche) is paid in full, and (iii) eligible borrowers will be able to meet financial obligations for at least 90 days and do not expect to file for bankruptcy during the time period of the loan. Significantly, the MSNLF, MSELF, and MSPLF all require an eligible borrower under each facility to attest that it will follow the compensation, stock repurchase and capital distribution restrictions applicable to direct loan programs under section 4003(c)(3)(A)(iii)of the CARES Act. Additionally, both eligible lenders and eligible borrowers must certify that their entity is able to participate in the respective facility, including that it is in compliance with conflicts-of-interest prohibitions in section 4019(b) of the CARES Act. Term sheets describing the MSNLF, MSELF and MSPLF can be found here. A more detailed update of the program terms can be found here. On May 27, 2020 the Federal Reserve Bank of Boston released additional information for potential lenders and borrowers in the MSLFP, including a form of loan participation agreement, lender and borrower certifications and covenants, updated FAQs and other legal documents.

REGULATORY SUPPORT

The federal banking agencies have taken a number of actions to support the CARES Act and Federal Reserve financing activities. For example, they have provided specific capital relief in connection with lending related to the PPP and the MMLF. Also, on May 5, 2020, the banking agencies released an interim final rule that modifies the agencies' Liquidity Coverage Ratio (LCR) rule to support banking organizations' participation in the MMLF and the PPPLF by neutralizing the LCR impact associated with the non-recourse funding provided by these Facilities. More information on regulatory measures to address the CARES Act, and COVID-19 more generally, are discussed in greater detail in our Advisory, "Financial Services Regulatory Actions to Address the Economic Impact of the Covid-19 Pandemic".

The CARES Act provisions and Federal Reserve actions described in this Advisory represent massive efforts to address the economic crisis facing the United States. They create both opportunities and risks for businesses, individuals, and state and local governments. How they will ultimately play out remains to be seen, particularly given that the rulemakings and other guidance necessary to implement them continue to evolve. The situation is constantly changing, leading to subsequent updates to regulatory actions and programs and policies described in this Advisory. Anyone interested in the outcome of this process would be well advised to pay close attention.

Footnotes

1. A review of federal and state financial services regulatory actions to aid financial institutions, other businesses, and individuals confronted by the pandemic can be found in our Advisory, "Financial Services Regulatory Actions to Address the Economic Impact of the Covid-19 Pandemic".

2. Pub. L. No. 116-139, Paycheck Protection Program and Health Care Enhancement Act (April 2020). The $484 billion consisted of $310 billion for the PPP (with $30 billion allocated specifically to community banks, credit unions and other lenders, and $30 billion allocated to medium-sized banks and credit unions) , $12 billion for PPP administrative costs, $60 billion for the SBA's Economic Injury Disaster Loan Program (which includes $10 billion in emergency grants for businesses), $75 billion in resources for hospitals, and $25 billion for COVID-19 testing.

3. DV Diamond Club of Flint, LLC, et al., v. Small Business Administration, et al., No. 20-1437 (6th Cir. May 15, 2020). (Plaintiffs were challenging the SBA-adopted "PPP Ineligibility Rule" as conflicting with statutory language referring to "any" business, slip op. at 2). The U.S. Court of Appeals for the Seventh Circuit also refused to stay a lower court preliminary injunction in a case involving plaintiffs that were strip clubs, in Camelot Banquet Rooms, Inc., et al., v. Unites States Small Business Administration, et al., No. 20-1729 (7th Cir. May 20, 2020).

4. See e.g., Lauren Hirsch, "Small business loans above $2 million will get full audit to make sure they're valid, Mnuchin says," CNBC, April 28, 2020

Originally published 29 May, 2020

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.