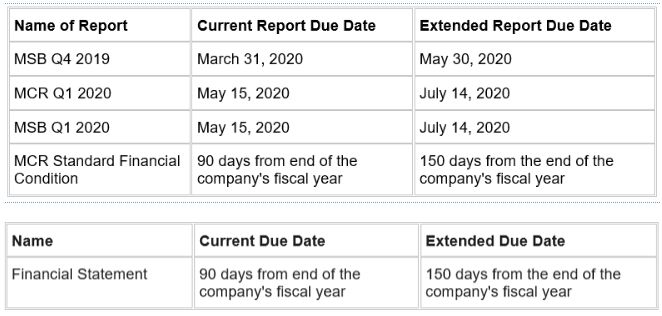

The next test for mortgage finance companies licensed through the NMLS is the requirement of a number of states to provide financial statements through the NMLS within 90 days of the licensee's fiscal year end. We brought this issue to the attention of the Conference of State Bank Supervisors ("CSBS") two weeks ago, and this was considered by the NMLS Policy Committee last week. No decision was made at that time, but the Policy Committee agreed to consider the matter further this week. As we understand, after the meeting of the Policy Committee on Tuesday, it was decided that while financial statements are still due, there will be a 60 day grace period to provide the financial statements, and certain other required filings of state licensed entities. Specifically, the NMLS Policy Committee issued the following yesterday:

"In response to the COVID-19 pandemic and its impact on state regulated entities, the NMLS Policy Committee has implemented a 60-Day deadline extension for the following types of reporting submitted in NMLS:

- Money Services Business Call Report

- Mortgage Call Report

- Financial Statement

Note that relief from a filing is provided, not just for financial statements and mortgage call reports of mortgage finance company licensees, but also call reports for money service business. Check the NMLS Coronavirus/COVID-19 page for the actual guidance provided by the CSBS. Regulators, in some states (Oregon for example) also have issued state-specific guidance on this issue.

Prior to the recent guidance of the NMLS Policy Committee, and after our initial request to CSBS, we contacted regulators in each state to inquire as to whether they would waive the filing of financial statement by the due date, or whether the licensee could be relieved of a sanction or financial penalty for not making a timely filing. Regulators in nearly all of the states responded to our request, but some states were uniquely positioned in their responses.

Some states such as Virginia, have statutory language that states that "every licensee shall file quarterly mortgage call reports through the Nationwide Multistate Licensing System and Registry ("NMLS" or the "Registry") as well as such other information pertaining to the licensee's financial condition as may be required by the Registry. Reports shall be in such form, contain such information, and be submitted with such frequency and by such dates as the Registry may require." Other state mortgage finance laws do not require the submission of audited financial statement by the end of the first quarter, but may still require the filing of a financial statement. Regulators in some states may not have the authority to waive the filing of a financial statement or other report by the due date, because the state law may expressly require the filing of a financial statement or other report by a certain date. Likewise, some other regulator(s) may not have sufficient discretionary authority under the jurisdiction's licensing statute to extend the due date for the filing.

We urge you to review the CSBS guidance, and any specific state guidance that also may have been issued. If after doing so you remain concerned about the position of any particular state's filing obligation(s) for licensed entities, please contact us and we will attempt to obtain additional guidance from that state.

Visit us at mayerbrown.com

Mayer Brown is a global legal services provider comprising legal practices that are separate entities (the "Mayer Brown Practices"). The Mayer Brown Practices are: Mayer Brown LLP and Mayer Brown Europe – Brussels LLP, both limited liability partnerships established in Illinois USA; Mayer Brown International LLP, a limited liability partnership incorporated in England and Wales (authorized and regulated by the Solicitors Regulation Authority and registered in England and Wales number OC 303359); Mayer Brown, a SELAS established in France; Mayer Brown JSM, a Hong Kong partnership and its associated entities in Asia; and Tauil & Chequer Advogados, a Brazilian law partnership with which Mayer Brown is associated. "Mayer Brown" and the Mayer Brown logo are the trademarks of the Mayer Brown Practices in their respective jurisdictions.

© Copyright 2020. The Mayer Brown Practices. All rights reserved.

This Mayer Brown article provides information and comments on legal issues and developments of interest. The foregoing is not a comprehensive treatment of the subject matter covered and is not intended to provide legal advice. Readers should seek specific legal advice before taking any action with respect to the matters discussed herein.