Keywords: UBTI, unrelated business taxable income, subscription credit facilities

A subscription credit facility (a Facility), also frequently referred to as a capital call facility, is a loan by a bank or other credit institution (the Creditor) to a real estate or private equity fund (the Fund). A Facility is defined by its collateral package: the obligations are secured by the unfunded capital commitments (the Unfunded Commitments) of the limited partners of the Fund (the Investors) and the Creditor's primary and intended source of repayment is the funding of capital contributions (Capital Contributions) by such Investors.

When a Fund incurs debt under a Facility, certain of its tax-exempt Investors, such as pension plans, private foundations, universities and charitable endowments (Tax-Exempt Investors) can be subject to unrelated business income tax (UBIT) on their unrelated business taxable income (UBTI) under the US Internal Revenue Code (the Code). Preferring to avoid paying UBIT, such Investors often require a Fund to covenant in its partnership agreement that the Fund will not incur, or will limit or minimize, UBTI.

This Legal Update provides a basic understanding of UBTI and sets forth structural and practical solutions to enable a Fund to enter and benefit from a Facility.

Understanding UBTI

A Tax-Exempt Investor is generally exempt from US federal income tax. However, to prevent Tax- Exempt Investors from unfairly competing with their taxable counterparts, they are subject to taxation on their UBTI under Section 511 of the Code. UBTI is defined, generally, under the Code as any income earned or derived by a Tax- Exempt Investor from a trade or business that is unrelated to the Tax-Exempt Investor's exempt purpose.1 While the Code provides that most forms of passive income, such as interest, dividends and capital gains, will not be treated as UBTI,2 UBTI does include income that is derived from assets that are subject to "acquisition indebtedness."3

Acquisition indebtedness is generally the unpaid amount of any indebtedness incurred directly or indirectly to acquire or improve an asset, including (i) indebtedness incurred in acquiring or improving the asset, (ii) indebtedness incurred before the acquisition or improvement of the asset if such indebtedness would not have been incurred but for the acquisition or improvement of the asset and (iii) indebtedness incurred after the acquisition or improvement of the asset if such indebtedness would not have been incurred but for such acquisition or improvement and such indebtedness was reasonably foreseeable at the time of the acquisition or improvement.4

UBTI generated by a Fund that is classified as a partnership for US federal income tax purposes "flows through" to its Tax-Exempt Investors and retains its character as UBTI in the hands of the Tax-Exempt Investors.5 Consequently, if such a Fund incurs debt in connection with its acquisition of an investment (an Investment), a pro rata share of the Fund's income from the Investment allocable to certain Tax-Exempt Investors may result in UBTI for such Investors.

Practical and Structural Solutions

There are a variety of solutions that a Fund may deploy to enable the use of a Facility without generating UBTI. The best solution to manage this issue, however, will ultimately depend on a number of specific factors, including but not limited to: (i) the Fund's organizational structure; (ii) the Fund's investment strategy; (iii) the overall composition of the Fund's Investors; and (iv) the actual sensitivity to UBTI of the Fund's Tax-Exempt Investors. Below are potential alternatives that enable a fund to borrow under a Facility without attributing the debt specifically to the Tax-Exempt Investors for purposes of the UBTI rules. It should be noted, however, that these alternatives may each raise other tax issues for Investors and only after consideration of all factors, including those described above, can an optimal approach be identified.

TIMING OF THE BORROWING

In practice, UBTI can be avoided based on the tenor of the individual loans under a Facility. For example, if acquisition indebtedness is paid off more than 12 months prior to the date that the debt-financed Investment is sold, UBTI on the gain should be avoided.6 Thus, for Funds making Investments with lengthy time horizons, indebtedness under a Facility giving risk to UBTI may be only a theoretical concern, not a practical one. This is especially true for funds that only use a Facility during their investment period. However, as the timing of harvest events is inherently unpredictable, Funds may have discomfort relying on this exemption in isolation.

BLOCKER CORPORATIONS

If a Fund acquires an Investment in or through an entity classified as a corporation for US federal income tax purposes (as opposed to an entity classified as a partnership for US federal income tax purposes) and such entity or a subsidiary is the borrower under the Facility, the Investment generally does not generate UBTI because, under the Code, the debt of a corporation is not deemed to be the debt of the shareholders. Thus, a Fund can block UBTI by employing a structure that permits its Investments to be made through a blocker corporation. Several structural variations as to how that can be accomplished are set forth below along with the corresponding adjustments to the Facility structure.

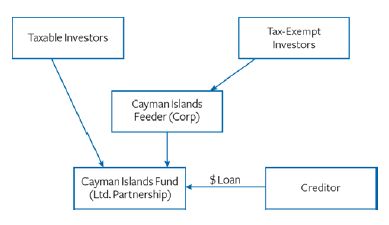

Tax-Exempt Blocker. A Fund can be structured so that the Tax-Exempt Investors hold their interests in the Fund through a blocker corporation. For example, if the Fund is a Cayman Islands limited partnership, the Tax- Exempt Investors invest in the Fund through a Cayman Islands feeder that elects to be classified as a corporation for US federal income tax purposes. This allows the Fund to borrow under a Facility without generating UBTI for the Tax- Exempt Investors.

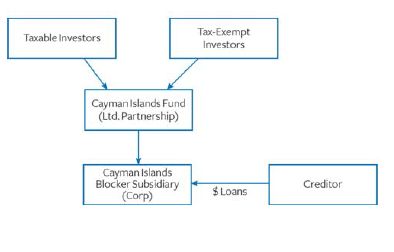

Fund Blocker. The Fund entity itself could form a blocker corporation subsidiary to borrow the funds under the Facility and thereby block all Investors from a pro rata share of the Facility debt. For example, a Cayman Islands limited partnership Fund (the Fund Parent) could form a wholly owned Cayman Islands entity that elects to be classified as a corporation for US federal income tax purposes (the Blocker Sub) through which it borrows monies under a Facility and makes its Investments. The Blocker Sub will effectively block UBTI for the Tax-Exempt Investors. Under this approach, however, all Investors and Fund Parent are effectively blocked and other tax considerations may be impacted.

When a Fund employs a Blocker Sub structure, the Facility security structure must be adjusted to accommodate the Fund structure. Often, the Fund Parent simply guarantees the Blocker Sub's obligations under the Facility, and secures such guaranty with the pledge of its Uncalled Commitments in favor of the Creditor. However, in certain circumstances such a guaranty may be deemed too analagous to debt of the Fund Parent, and further Facility structural changes will be required.

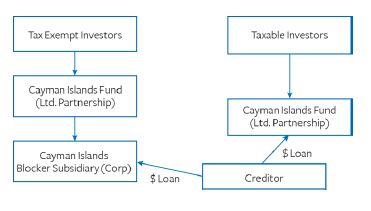

One such structural change is commonly referred to as "Cascading Pledge Structure" in the Facility market. To accomplish this, the Fund Parent secures its capital commitment to the Blocker Sub with a pledge of its Unfunded Commitments. In turn, the Blocker Sub onpledges such Unfunded Commitments to the Creditor to secure the obligations under the Facility.

Parallel Blockers. In a situation where a Fund is structured as a series of parallel funds, each parallel fund forms an appropriate borrowerentity that acts as a co-borrower. For example, the Tax-Exempt Investors would invest through a parallel fund that would form a blocker corporation as its borrower, while the Non-Tax- Exempt Investors would invest through a parallel fund that might form a tax pass-through entity as its borrowing vehicle. This way, the Tax-Exempt Investors' UBTI concerns are accommodated while the non-Tax-Exempt Investors can continue to invest through pass-thru entities. Various cross-collateral arrangements between the co-borrowers would then be put in place in the Facility for the benefit of the Creditor to ensure that the Unfunded Commitments of all Investors provide cross-collateralization.

POTENTIAL ADDITIONAL SOLUTIONS

There are additional potential structural solutions to avoid generating UBTI, particularly for Funds that invest in real estate. For example, the Code has an explicit exemption for debtfinanced real estate—specifically for certain Tax- Exempt Investors such as pension plans and educational institutions—recognizing the common practice of financing real estate Investments.7 Complying with this exemption requires care and is beyond the scope of this Legal Update (especially with regard to the "Fractions Rule" component), but it is another available option for real estate Funds.

Additionally, dividends and capital gains from REITs are generally not subject to UBIT even if the REIT borrows under a Facility to finance an Investment, so use of REITs in a real estate Fund's structure is another effective UBTI blocking technique.8

Market Trends and Conclusion

Interestingly, in recent years, we have seen a trend where Tax-Exempt Investors are increasingly open to bearing UBIT in certain circumstances, especially in Funds with very high expected returns. In fact, many Tax-Exempt Investors now seem satisfied if the Fund will simply covenant to give them the option to elect to fund any particular Investment through a blocker entity (as opposed to requiring the Fund to take commercially reasonable steps to avoid generating UBTI). Regardless, there are solutions available to a Fund to eliminate or reduce UBTI for Tax-Exempt Investors but still enjoy the benefits of a Facility. However, the appropriate solutions depend on the specific characteristics of the particular Fund and its Investors.

Footnotes

1 Code Section 512(a)(1).

2 Code Section 512(b).

3 Code Section 512 (b)(4); Code Section 514.

4 Code Section 514(c)(1).

5 Code Section 512(c); Code Section 513(b).

6 Code Section 514(c)(7). However, in the case of income other than disposition gain, UBTI will be determined based on the average acquisition indebtedness during the tax year in which such income is generated.

7 Code Section 514(c)(9).

8 However, REIT dividends may be treated as UBTI for certain pension plans if the REIT is, directly or indirectly, predominantly owned by pension plans. Code Section 856(h)(3)(C).

Originally published on November 12, 2012Visit us at mayerbrown.com

Mayer Brown is a global legal services provider comprising legal practices that are separate entities (the "Mayer Brown Practices"). The Mayer Brown Practices are: Mayer Brown LLP and Mayer Brown Europe – Brussels LLP, both limited liability partnerships established in Illinois USA; Mayer Brown International LLP, a limited liability partnership incorporated in England and Wales (authorized and regulated by the Solicitors Regulation Authority and registered in England and Wales number OC 303359); Mayer Brown, a SELAS established in France; Mayer Brown JSM, a Hong Kong partnership and its associated entities in Asia; and Tauil & Chequer Advogados, a Brazilian law partnership with which Mayer Brown is associated. "Mayer Brown" and the Mayer Brown logo are the trademarks of the Mayer Brown Practices in their respective jurisdictions.

© Copyright 2012. The Mayer Brown Practices. All rights reserved.

This Mayer Brown article provides information and comments on legal issues and developments of interest. The foregoing is not a comprehensive treatment of the subject matter covered and is not intended to provide legal advice. Readers should seek specific legal advice before taking any action with respect to the matters discussed herein.