On 10th December 2020, the Central Bank of Nigeria ("CBN") issued a Circular dated 9th December 2020 on a new licence categorisation for payments system in Nigeria ("Circular"). It is instructive to mention that the CBN issued an exposure draft on the licensing regime for payment service providers in 2018, however, the substantive circular was not issued.

The approval delay over the past couple of years created fear and apprehension for existing market players, not leaving out potential investors in the Nigerian payments industry. Certainly, this Circular will bring a huge relief to all concerned, as it now provides the much-needed clarity on licence categories for participants and applicable minimum capital requirements. It's also a very welcome development to see that the high minimum capital thresholds previously set out in the exposure draft have been significantly reduced for some of the categories.

We have taken the liberty to highlight the provisions of the Circular for your information.

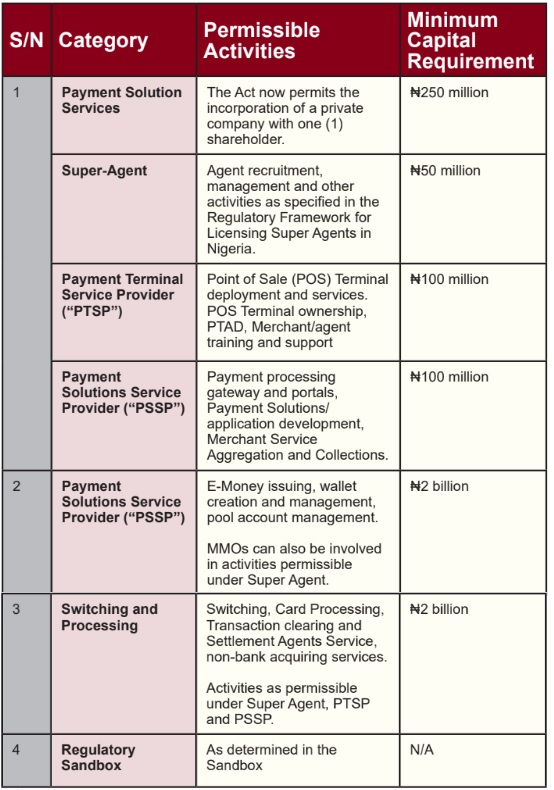

Under the new Circular, payments system licencing has been streamlined into four categories, and these are:

- Payment Solution Services ("PSS")

- Mobile Money Operators ("MMOs")

- Switching and Processing; and

- Regulatory Sandbox

We have outlined the permissible activities below, and the minimum capital requirements for each licence category:

In addition to the above, all payment service providers and other stakeholders in the payment service industry must note the following:

- Only MMOs are allowed to hold customers funds. All other players with a licence within any of the other categories are not permitted to hold customer funds.

- Companies intending to operate as a Switch and MMO are only permitted to operate under a holding company structure with the operations of the subsidiary companies clearly separated to properly delineate their respective business operations.

- Payment companies under the PSS category may hold either the Super-Agent, PTSP or PSSP licences, or hold a combination of these three licences under the broad category "PSS" with a much higher minimum capital requirement at ₦250million.

- Any licensed payment service provider covered by the Circular, who is looking to obtain any other licence from the CBN, must obtain a "no objection" letter from the Payments System Management Department of the CBN.

- The object clauses in a payment service provider's Memorandum and Articles of Association must be restricted to the permissible activities under their licensing authorizations.

- Any collaboration regarding product and service offerings between licenced Payment Service Providers, Banks and Other Financial Institutions are now subject to the CBN's prior approval.

Compliance with the Circular

Companies that intend to apply for any of the licences listed above must ensure immediate compliance with the requirements set out in the Circular. This immediate compliance also applies to companies that have been granted Approvals – in- Principle by the CBN in respect of any of the above licences.

Existing licenced payment companies however enjoy a circa six-month grace period and are expected to comply with the new licencing requirements not later than the end of June 2021.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.