The Bermuda Government has passed legislation, with effect from 31 December 2018, requiring relevant entities based in Bermuda to comply with certain obligations in regard to economic substance in the jurisdiction. We set out below a summary of the entities affected by this new legislation and the information that such entities will need to provide in order to evidence their compliance.

The Economic Substance Act 2018 and the Economic Substance Regulations 2018 were enacted in response to a scoping paper issued by the European Union's Code of Conduct Group (Business Taxation) in June 2018. The paper set out requirements that certain jurisdictions1 outside the EU must adopt with regard to the economic substance of entities based in those jurisdictions, in order to avoid being black-listed by the EU. Broadly equivalent legislation has been passed in all of the major offshore jurisdictions in addition to Bermuda, including the Cayman Islands, BVI and the Channel Islands. It is anticipated that the EU's economic substance requirements will soon become a global OECD standard.

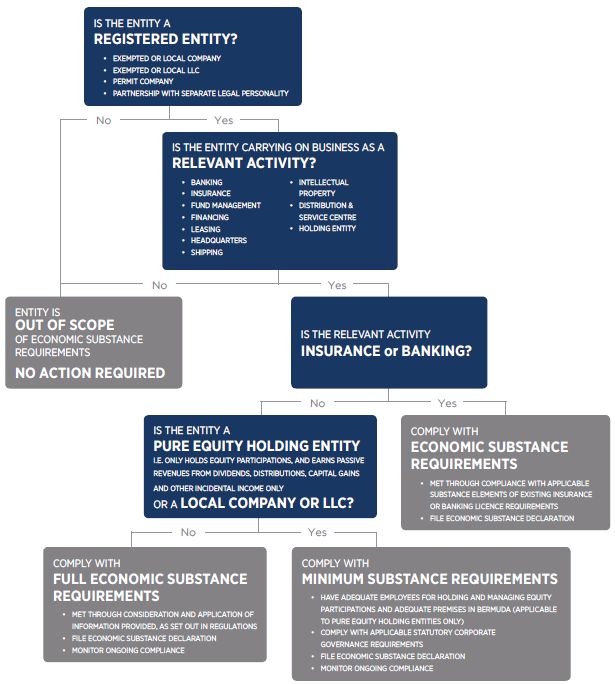

Entities within scope

Registered Entities

Entities within the scope of the legislation ('registered entities') include exempted and local companies, permit companies, exempted and local LLCs and partnerships that elect to have separate legal personality, where those entities are carrying on a 'relevant activity'.

Relevant Activities

Those registered entities which carry on as a business any one or more of the following relevant activities will be in scope and must comply with economic substance requirements:

- Banking

- Insurance

- Fund management

- Finance and leasing

- Headquarters

- Intellectual property

- Distribution and service centres

- Holding entity

These terms are defined in the legislation and a summary of them is included in Appendix 2 to this bulletin. It is anticipated that guidance notes will be issued by the Bermuda Government in due course to provide further practical detail.

Entities out of scope

Registered entities which do not carry on as a business a relevant activity will not be required to comply with economic substance requirements.

Registered entities with minimum economic substance requirements

Local companies and local LLCs carrying on relevant activities, and pure equity holding entities (as defined in Appendix 2), are only required to comply with minimum economic substance requirements. These requirements include (i) compliance with the applicable corporate governance requirements of the Companies Act 1981 (for companies) or the Limited Liability Companies Act 2016 (for LLCs), or the Partnerships Acts (for partnerships that elect to have separate personality) including keeping records of account, books and papers and financial statements; and (ii) filing an economic substance declaration (see below). Pure equity holding entities will also be required to have adequate employees for holding and managing equity participations, and adequate premises in Bermuda.

Economic substance requirements

For all other registered entities carrying on relevant activities, the legislation requires that they maintain a substantial economic presence in Bermuda, and in that regard comply with full economic substance requirements. These requirements will be met if:

- the entity is managed and directed in Bermuda

- core income generating activities are undertaken in Bermuda with respect to the relevant activity

- the entity maintains adequate physical presence in Bermuda

- there are adequate full time employees in Bermuda with suitable qualifications

- there is adequate operating expenditure incurred in Bermuda in relation to the relevant activity

The Registrar will determine whether or not the economic requirements are met, based upon the following information provided by the entity:

- the nature and extent of the relevant activity engaged in by the entity including, in particular, its core income generating activities undertaken with respect to such relevant activity

- the nature and extent of the entity's presence in Bermuda including physical offices or other premises occupied by the entity or its affiliate in Bermuda and an adequate level of annual expenditure of the entity in Bermuda

- whether the entity is managed and directed in Bermuda or from Bermuda, having regard to:

-

- the location of strategic or risk management and operational decision-making, or where management of the entity meets to make decisions regarding business activities

- the presence of an adequate number of senior executives, employees or other persons in Bermuda who are suitably qualified and responsible for oversight/execution of its core income generating activities

- the location and nature and frequency of board, manager or partnership meetings held in Bermuda in relation to the overall number of meetings

- the nature and extent of outsourcing arrangements (if any) to affiliates or service providers in Bermuda and whether and to what extent the persons carrying on the outsourced services are suitably qualified and have adequate capacity for the implementation and execution of those services, and whether the outsourced service provider complies with the economic substance requirements applicable to the outsourcing entity (noting that employees, premises and expenditure may not be counted multiple times by multiple entities with respect to such compliance)

This information should be viewed collectively, and not prescriptively. In other words, for all registered entities that are in-scope, a combination of some or all information will be considered. In practice, this means that what constitutes compliance with economic substance requirements will necessarily differ from entity to entity, depending on each entity's relevant activity and its individual circumstances in relation to its business.

Core income generating activities

The core income generating activities that should be undertaken by the entity in Bermuda will differ between the various relevant activities. The core income generating activities identified in the legislation in respect of each relevant activity are set out in Appendix 2, and it will be necessary for entities to be conducting at least some of those activities in Bermuda, whether directly or through outsourcing arrangements in Bermuda (noting the comments above regarding the nature of any such outsourcing).

Regulated entities: insurance and banking

It is recognized that certain regulated sectors, notably insurance and banking, are already subject to 'substance' requirements in Bermuda by virtue of their existing regulatory requirements. As such, to the extent that entities are carrying on insurance or banking as a relevant activity, they will be deemed to meet economic substance requirements in respect of that activity through compliance with their existing regulatory requirements. Such companies will be required to complete and file an economic substance declaration (see below), but by confirming compliance with their respective regulatory requirements, it is expected that the completion of that declaration should be much simplified.

Intellectual Property

Entities carrying on IP business as a relevant activity are subject to certain enhanced requirements and will be presumed not to comply with economic substance requirements unless those enhanced requirements are met. In particular, those entities carrying on high risk IP activity (namely, owning an IP asset that has been acquired from an affiliate or been obtained through the funding of overseas research and development and which is then licensed to a foreign affiliate or used to generate revenue through activities performed by a foreign affiliate) must provide additional information to the Registrar, including a detailed business plan, in order to rebut the presumption of non-compliance. Registered entities undertaking IP business as a relevant activity are advised to seek legal advice regarding these enhanced requirements.

Annual Economic Substance Declaration

All entities undertaking relevant activities, which includes all pure equity holding entities, will file an Economic Substance Declaration ("ESD") annually, with information provided in relation to the previous financial year (the 'relevant financial period'). The ESD will require the disclosure of certain key information applicable to an analysis of economic substance requirements. At a minimum this will include:

- whether or not the entity is carrying on a relevant activity and the type of relevant activity being undertaken

- whether the entity is engaging in high risk IP activity

- whether the entity will outsource the relevant activity and to whom

- the core income generating activities that are undertaken in Bermuda with respect to the relevant activity

- the gross income for the relevant financial year

- the premises in Bermuda

- the names and physical addresses of the directors/managers/partners resident in Bermuda

- the holding entity, ultimate parent entity, owner or beneficial owner of the entity

- the operating expenses and assets for the relevant financial year and number of full time employees

- such other information as the Registrar may require

The form of ESD has not yet been prescribed by the Bermuda Government, but it is expected that it will be prescribed within the first half of 2019 and that, for most entities, the first ESD filing will be made in 2020.

Monitoring and enforcement

The Bermuda Registrar of Companies will be responsible for implementing, monitoring and enforcing the economic substance regime. The legislation provides for civil penalties up to BD$250,000 to be applied in relation to non-compliance with the applicable economic substance requirements. If, after the civil penalties have been exhausted, an entity continues its failure to comply, the Registrar may apply to the Court for an order in such terms as it thinks fit. This may include an order for striking off the entity. There is also an offence created of knowingly making a false economic substance declaration, with penalties up to BD$10,000 or imprisonment for two years, or both.

Confidentiality

In the collection of information or documents pursuant to the legislation (whether through the ESD or otherwise), the Registrar is expressly obliged to preserve the confidentiality of such information or documents, other than as may be required in connection with its duties (see below).

Information sharing with competent authorities

As an extension of Bermuda's existing obligations to share information in connection with international Tax Information Exchange Agreements, the legislation provides for the automatic provision of information in relation to economic substance in certain circumstances. In particular, where an entity is found not to be in compliance with economic substance requirements for a relevant financial period, or is engaged in high risk IP activities (as described above), the Registrar is required automatically to provide economic substance information to the competent authority of the EU member state in which the entity's holding entity, ultimate parent, owner or beneficial owner is incorporated, formed, resident or registered.

Transition

The economic substance requirements are applicable from 1 January 2019 for all new entities formed or incorporated on or after that date. For existing entities, formed or incorporated on or before 31 December 2018, the requirements will be applicable from 1 July 2019.

Further development

The EU is in the process of reviewing Bermuda's legislation, along with the legislation passed by other jurisdictions. It is currently expected that they will issue their final decision by the end of Q1 2019 on whether, or to what extent, the legislation meets the requirements of their scoping paper. Following that decision, amendments to the legislation (and guidance notes) may be required. To the extent that such changes are made, they will be the subject of future client bulletins.

ECONOMIC SUBSTANCE DECISION-MAKING FLOW CHART – BERMUDA

APPENDIX 2

LIST OF CORE INCOME GENERATING ACTIVITIES, FOR EACH RELEVANT ACTIVITY

| Relevant Activity | Definition and Core Income Generating Activities |

| BANKING | Engaging in

deposit-taking business for which a licence is required in

accordance with the Banks and Deposit Companies Act 1999

|

| INSURANCE | Engaging in business for

which registration is required in accordance with the Insurance

Act 1978

|

| FUND MANAGEMENT | Managing investments for

funds and in respect of which a licence is required in accordance

with the Investment Business Act 2003 or for which a

licence would be required if such activity were taking place in

Bermuda

|

| FINANCING | Providing funds, other

than by way of subscription for shares or other equity

contributions, for the business activities of one or more other

entities (whether or not affiliated)

|

| LEASING | Providing leasing

arrangements in respect of which it is the lessor of one or more

assets leased to one or more affiliates or third parties

|

| HEADQUARTERS | Engaging in the general

management and administration of its affiliates within or outside

Bermuda

|

| SHIPPING | Engaging in ownership,

leasing, operation or management of a ship that is used to

transport goods

|

| DISTRIBUTION & SERVICE CENTRE | Engaging in resale of

goods purchased from a foreign affiliate (distribution centre); or

primarily providing consulting or administrative services to a

foreign affiliate (service centre)

|

| INTELLECTUAL PROPERTY | The exploitation of IP

assets held by the entity (including non-trade intangible assets)

|

| HOLDING ENTITY | A holding entity* may

include a pure equity holding entity. A pure equity holding

entity is an entity that only holds equity participations

in one or more entities, and earns passive revenues from dividends,

distributions, capital gains and other incidental income only.

|

Footnote

1. Anguilla, Bahamas, Bahrain, Bermuda, British Virgin Islands, Cayman Islands, Guernsey, Isle of Man, Jersey, Marshall Islands, Turks and Caicos Islands, United Arab Emirates, Vanuatu

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.