What are "Corona Bonds"?

"Corona Bonds" are proposed joint debt securities issued by an EU institution in lieu of individual EU Member States issuing debt securities. The funds would be mutualised debt, taken collectively by all Member States of the European Union with the proceeds of the debt shared among all Member States in pre-agreed proportions.

Why is this on the agenda now?

The coronavirus or Covid-19 pandemic is an unprecedented worldwide emergency, and the EU has become one of the epicentres of the outbreak. European economies have been particularly hard-hit with millions losing their jobs and unprecedented levels of public spending being announced; to say nothing of the suffering of those who contract the virus and the ever rising death toll across the EU.

Faced with this historic challenge, nine EU countries wrote a letter calling for Corona Bonds to be issued EU-wide: Spain, Italy, France, Belgium, Luxembourg, Ireland, Portugal, Greece and Slovenia. The proposal is opposed by certain comparatively richer northern European Member States, including Germany, The Netherlands, Austria and Finland.

Ireland's position in supporting Corona Bonds is interesting as it could be said to shift away from Ireland's alignment with the "New Hanseatic League"; a group of eight northern European countries (including Ireland, the Netherlands and Finland) who professed to have "shared views and values in the discussion on the architecture of the [European Monetary Union]" in a position paper in 2018.

What are the arguments for Corona Bonds?

In their letter, the nine heads of government say "the case for such a common [debt] instrument is strong, since we are all facing a symmetric external shock, for which no country bears responsibility, but whose negative consequences are endured by all". They state that the bonds should have "sufficient size and long maturity to be fully efficient".

The argument is essentially that, faced with a common threat which is not the fault of any one Member State, it would be better to mutualise borrowing costs among all Member States rather than certain economies singled out by the markets.

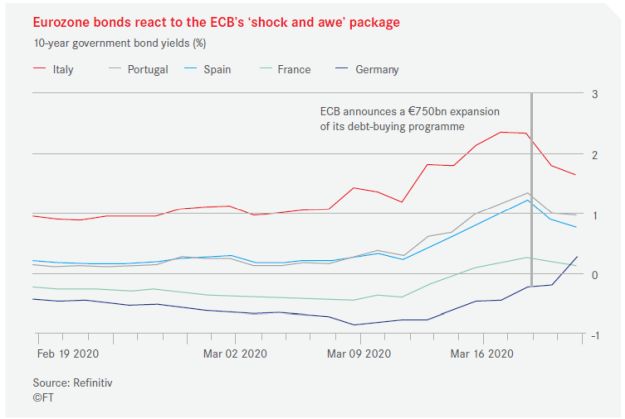

For example, the graph below shows how 10 year government bond yields have fluctuated over the past three months, with German yields remaining below 0% until recently, while Italian yields peaked at over 2%, with the difference - or "spread" - between Italian and German government bonds widening as the crisis in Italy deepened. The lack of existing supports for some EU economies was put into stark relief by Christine Lagarde, the head of the European Central Bank (speaking before the ECB announced the expansion of its debt-buying programme) who said "We are not here to close [bond] spreads, there are other tools and other actors to deal with these issues."

What are the arguments against Corona Bonds?

Fiscally prudent countries do not like the idea of less prudent countries "borrowing" their reputations in order to raise cheap money on the bond markets. The argument goes that without the constraint of higher borrowing costs less prudent countries will never change their ways, and such countries should not benefit from the hard work, prudence and self-control of their neighbours.

This sounds familiar.

That's right. During the 2010-2012 sovereign debt crisis there was a lot of discussion of issuing joint "Eurobonds". At the time some countries supported the idea, but it was strongly resisted by others, who again argued that each Member State should be individually responsible for keeping its budgetary affairs in order and managing its own borrowing costs.

What happens next?

At a video conference on 26 March, European leaders clashed over the concept of Corona Bonds. Italian Prime Minister Giuseppe Conte argued forcefully that the bonds were needed to support Member States such as Italy at their time of need. However, the refusal of other EU Member States to support the proposal led to difficulties in agreeing a joint response to be issued post-meeting. The final joint statement essentially delayed the decision, mandating Eurozone finance ministers to report back in two weeks with "proposals" for a comprehensive response, but without expressing any preferred options.

Another option: the Eurozone bailout fund

An alternative approach which has gained increasing prominence in recent weeks would be to use the European Stability Mechanism (ESM) (commonly known as the Eurozone bailout fund) to provide financial assistance to affected Eurozone countries. The ESM has a current lending capacity of ?410 billion and the proposal would be for relevant Member states to avail of loans on low-interest terms under the ESM's Enhanced Conditions Credit Line (ECCL) (representing approximately ?248 billion of the ESM's overall lending capacity).

The problem with this proposal is that ESM funds typically have conditions attached; many of which are aimed at restoring the stability of the public finances of the recipient. For some countries the borrowing is seen as a necessary response to a health crisis common to all Member States which is not of their own making. The idea of having conditions to such funding (including pledges on structural economic reforms) is unacceptable to many.

Originally published April 2, 2020

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.