On 29 November, it was confirmed, that the changes to the Non-Habitual Tax Resident (NHR) regime will become effective – amending the current regime and introducing a new regime.

When will the Current NHR regime end?

The current NHR regime will end on two different dates for two separate groups of people – namely:

- Those who become tax resident before 31 December 2023; and

- Those who qualify to become tax resident before 31 December 2024 (under specific conditions referred below).

Those Who Become Tax Resident Before 31 December 2023 – Under the Current Regime

Anyone who becomes a tax resident in Portugal (as an EU national or through a qualified visa), before 31 December 2023, and are performing a high value-added activity or an activity of a scientific, artistic, or technical nature, and who have not been tax resident in Portugal in the last five years, will be able to apply for the NHR. They will have until 31 March 2024 to register for their NHR status.

Those Who Become Tax Resident Before 31 December 2024 – Under the Current Regime

The grandfathering rule will also apply to taxpayers who become tax residents of Portugal during the next year, by 31 December 2024, if one of the following conditions is met:

a. A promissory employment agreement or promissory secondment agreement (or employment or secondment agreement) is signed by 31 December 2023, to perform activities in Portugal; OR

b. A lease agreement or other agreement granting the use or possession of property located in Portugal before 10 October 2023 (the day when the NHR withdrawal was officially announced); OR

c. Reservation or promissory contract, for the acquisition of property located in Portugal before 10 October 2023 (the day when the NHR withdrawal was officially announced); OR

d. Enrolment or registration of dependents at a Portuguese educational establishment before 10 October 2023 (the day when the NHR withdrawal was officially announced); OR

e. Possession of a residence visa or residence permit that is valid by 31 December 2023; OR

f. A procedure, is initiated by 31 December 2023, to obtain a residence visa or residence permit from the competent authorities, in accordance with the current immigration legislation. This can be done by requesting an appointment or attending an appointment to submit the application for a residence visa or residence permit, or by submitting the application for a residence visa or residence permit directly; OR

g. The taxpayer is a member of the household of a taxpayer, who meets one of the above conditions.

I am currently an NHR – does this affect me?

As the current NHR regime will be grandfathered (for all applications made under the existing regime), there is no impact for individuals already enjoying NHR status (or who will become NHR under the conditions mentioned above). The regime will continue to exist until the 10-year NHR period is reached, from when each specific individual registered for NHR.

When will the New NHR regime take effect?

A new NHR regime is applicable to those who do not meet the conditions mentioned above.

The new regime is effective from 1 January 2024, and offers a narrower scope of eligible professions, than the current NHR regime.

Individuals who become tax residents of Portugal from 1 January 2024 (under the new NHR regime), and have not been tax resident in Portugal in the previous five years may qualify for the new NHR. Please see below, specific criteria to meet to be eligible under the new NHR.

Who will be eligible for the new NHR regime?

The following individuals may be eligible for the new NHR regime:

- Teaching in higher education and scientific research, including scientific employment in entities, structures, and networks within the Portuguese science and technology system, as well as positions on the governing bodies of entities recognised as technology and innovation centres;

- Qualified jobs within the scope of 'contractual benefits towards productive investment', as defined in Chapter II of the Portuguese Investment Tax Code;

- Qualified jobs recognised by AICEP Portugal Global – Trade & Investment Agency or by IAPMEI – Agency for Competitiveness and Innovation as being relevant to the national economy, particularly in the context of attracting productive investment;

- Research and development personnel whose costs are eligible for the purposes of the tax incentive system for research and business development, as defined in the Investment Tax Code;

- Employment in entities certified as start-ups under the Portuguese Start-Up Law;

- Activities carried out by tax residents in the autonomous regions of the Azores and Madeira, as specified by regional decree.

What are the tax consequences of the new NHR regime?

Taxpayers who meet the requirements and fall into one of the categories, detailed above, may be taxed at a preferential fixed rate of 20%, on employment or self-employment, Portuguese sourced income, earned from such activities, for a period of 10 consecutive years (with the option of utilising the marginal rates, if lower).

To maintain eligibility for this regime, taxpayers must continue to earn active income, with a maximum interim period of 6 months between activities.

Eligible taxpayers may be exempt from taxation on foreign income from various sources, including; employment income earned abroad, self-employment income earned abroad, foreign rental income, and capital gains from foreign assets, with the exception of pension income (taxed at the progressive tax rates – previously 10% under the old NHR regime). Income derived from blacklisted tax havens will be subject to a 35% tax rate.

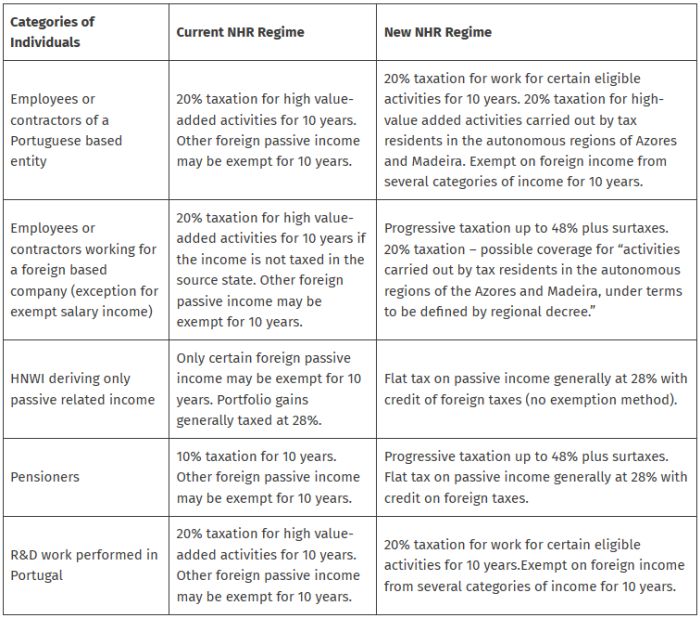

Summary of Tax Consequences Differentiating between the Current and New NHR Regime

What other tax benefits exist for Portuguese tax residents from 1 January 2024?

Individuals becoming tax resident in Portugal, as long as they have been Portuguese non-tax resident during the past five years and were previously tax resident in Portugal, will enjoy a 50% exemption from personal tax under the 'Regressar' programme. This relates to income, under the marginal tax rate, for the first €250,000 of taxable income from employment and independent business income. Income above this threshold will be taxed at the standard rate.

This exemption is valid for five years and is available for new tax residents from 1 January 2024 to 31 December 2026. Any individual, regardless of their expertise is eligible to benefit, high value-added criteria is not required.

To Conclude and for further advice and assistance

It is important to distinguish between the old regime ending on 31 December 2023, although with some exceptions valid until 31 December 2024, and the new regime (effective 1 January 2024).

There is an overlap in timings between the current and new NHR regimes, and it is important to engage with a technically qualified expert, such as Dixcart to advise further on the impact specific to you.

NHR does not need to be a complex topic when you consult with a relevant expert – reach out to Dixcart for more information: advice.portugal@dixcart.com.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.