The Insolvency and Bankruptcy Code, 2016 (IBC) was passed by the Parliament on 11 May 2016, received Presidential assent on 28 May 2016 and was notified in the official gazette on the same day.

Erstwhile legislative framework

Chapter XIX & Chapter XX of Companies Act, 2013

Part VIA, Part VII & Section 391 of Companies Act, 1956

RDDBFI Act, 1993

SARFAESI Act, 2002

SICA Act, 1985

The Presidency Towns Insolvency Act, 1909

The Provincial Insolvency Act, 1920

Chapter XIII of the LLP Act, 2008

Non-statutory guidelines/out-of-court mechanism:

- Bilateral restructuring

- One-time settlement

- JLF/CDR/SDR

- Sale of loan to ARC

New framework

The Insolvency and Bankruptcy code (Provisions of this Code to override other existing laws on matters pertaining to Insolvency and Bankruptcy)

"An act to consolidate and amend the laws relating to reorganisation and insolvency resolution of corporate persons, partnership firms and individuals in a time bound manner for maximisation of value of assets of such persons, to promote entrepreneurship, availability of credit and balance the interests of all the stakeholders including alteration in the order of priority of payment of Government dues and to establish an Insolvency and Bankruptcy Board of India, and for matters connected therewith or incidental thereto."

- Objective section of the Act

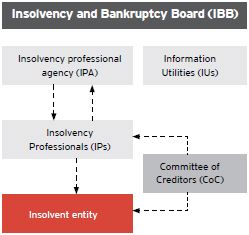

The Insolvency and Bankruptcy Code ecosystem

Insolvency and Bankruptcy Board (IBB)

NCLT – The adjudicating authority (AA)

IBB – apex body for promoting transparency & governance in the administration of the IBC; will be involved in setting up the infrastructure and accrediting IPs & IUs.

IUs - centralised repository of financial and credit information of borrowers; would accept, store, authenticate and provide access to financial data provided by creditors.

IPs- persons enrolled with IPA and regulated by Board and IPA will conduct resolution process; to act as Liquidator/ bankruptcy trustee; appointed by creditors and override the powers of board of directors.

Adjudicating authority (AA) - would be the NCLT for corporate insolvency; to entertain or dispose any insolvency application, approve/ reject resolution plans, decide in respect of claims or matters of law/ facts thereof.

IPA - registered by the board shall enroll IPs.

Corporate Insolvency Resolution and Liquidation

Resolution timeline and process

Key highlights

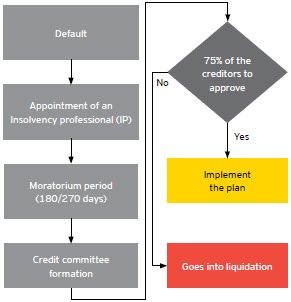

Corporate insolvency resolution process

Application on default – Any financial or operational creditor(s) can apply for insolvency on default of debt or interest payment

Appointment of IP – IP to be appointed by the regulator and approved by the creditor committee. IP will take over the running of the Company.

From date of appointment of IP, power of Board of directors to be suspended and vested in the IP. IP shall have immunity from criminal prosecution and any other liability for anything done in good faith

Moratorium period – Adjudication authority will declare moratorium period during which no action can be taken against the company or the assets of the company. Key focus will be on running the Company on going concern basis. A Resolution plan would have to be prepared and approved by the Committee of creditors

Credit committee - A credit committee of creditors will be constituted. Related party to be excluded from committee. Each creditor shall vote in accordance to voting share assigned if 75% of creditor approve the resolution plan same needs to be implemented.

Liquidation process

Initiation – Failure to approve resolution plan within specified days will cause initiation of Liquidation. Debtor can also opt for voluntary liquidation by a special resolution in a General Meeting.

Liquidator – The IP may act as the liquidator, and exercise all powers of the BoD. The liquidator shall form an estate of the assets, and consolidate, verify, admit and determine value of creditors' claims.

Order of priority for distribution of assets

- Insolvency related costs

- Secured creditors and workmen dues upto 24 months

- Other employee's salaries/dues up to 12 months

- Financial debts (unsecured creditors)

- Government dues (up to 2 years)

- Any remaining debts and dues

- Equity

Key aspects of the Insolvency and Bankruptcy Code

- IBC proposes a paradigm shift from the existing 'Debtor in possession' to a 'Creditor in control' regime.

- IBC aims at consolidating all existing insolvency related laws as well as amending multiple legislation including the Companies Act.

- The code would have an overriding effect on all other laws relating to Insolvency & Bankruptcy.

- The code aims to resolve insolvencies in a strict time-bound manner - the evaluation and viability determination must be completed within 180 days.

- Moratorium period of 180 days (extendable upto 270 days) for the Company. Insolvency profressional to take over the managemnent of the Company.

- Clearly defined 'order of priority' or the waterfall mechanism.

- The waterfall to render government dues junior to most others is significant.

- Antecedent tranactions can be investigated and in case of any illegal diversion of assets personal contribution can be ordered by court.

- Introduce a qualified insolvency professional (IP) as intermediaries to oversee the Process

- Establishment of Insolvency and Bankruptcy board as an independent body for the administration and governance of Insolvency & bankruptcy Law; and Information Utilities as a depository of financial information.

The Code, at best, is a plan currently awaiting execution. Appropriate information-flow, establishment of a tribunal process and the provision to bring in responsible professionals. The Ministry of Finance has indicated that they are aiming to make IBC operational by 31 March 2017.

The IBC envisages a "creditor in control" regime with financial creditors exercising control through IPs in the event of a single default in repayment of any loan or interest. This can be effected without any notice and the law is very stringent as compared to the SARFAESI Act, 2002. As a result, stressed/ distressed corporates need to implement an accurate cash flow forecasting mechanism to identify mismatches of inflows with commitments on a timely basis. If there is a possibility of a potential default that can trigger IBC, an effective turnaround plan should be devised and communicated to all stakeholders in advance – including financial and operating creditors, employees, etc. Such a plan should include aspects of financial restructuring, operational improvement and sale of assets which can be monetised.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.