Basis of taxation

All Cyprus tax resident individuals are taxed on all chargeable income (including certain employment benefits) accrued or derived from all sources in Cyprus and abroad. Individuals who are not tax residents of Cyprus are taxed on certain income accrued or derived from sources in Cyprus.

An individual is tax resident in Cyprus if (s)he spends in Cyprus more than 183 days in any one calendar year.

With effect as from 1 January 2017, an individual may also be considered tax resident in Cyprus if (s)he satisfies the "60 day rule". The "60 day rule" applies to individuals who in the relevant tax year:

- do not reside in any other single state for a period exceeding 183 days in aggregate, and

- are not considered tax resident by any other state, and

- reside in Cyprus for at least 60 days, and

- have other defined Cyprus ties. To satisfy this condition the individual must carry out any business in Cyprus and/or be employed in Cyprus and/or hold an office (director) of a company tax resident in Cyprus at any time in the tax year, provided that such is not terminated during the tax year. Further the individual must maintain in the tax year a permanent residential property in Cyprus which is either owned or rented by him/her.

For the purposes of both the "183 days rule" and the "60 days rule" days in and out of Cyprus are calculated as follows:

- the day of departure from Cyprus counts as a day of residence outside Cyprus

- the day of arrival in Cyprus counts as a day of residence in Cyprus

- arrival and departure from Cyprus in the same day counts as one day of residence in Cyprus

- departure and arrival in Cyprus in the same day counts as one day of residence outside Cyprus

Personal tax rates

The following income tax rates apply to individuals:

| Chargeable income for the tax

year € |

Tax rate % |

Accumulated tax € |

| First 19.500 | Nil | Nil |

| From 19.501 - to 28.000 | 20 | 1.700 |

| From 28.001 - to 36.300 | 25 | 3.775 |

| From 36.301 - to 60.000 | 30 | 10.885 |

| Οver 60.000 | 35 |

Foreign pension income is taxed at the flat rate of 5% on amounts over €3.420. The taxpayer can however on an annual basis elect to be taxed at the normal tax rates and bands set out above.

Cyprus source widow(er)'s pension is taxed at the flat rate of 20% on amounts over €19.500. The taxpayer can however on an annual basis elect to be taxed at the normal tax rates and bands set out above.

Exemptions

The following are exempt from income tax:

Exemptions

| Type of income | Exemption |

| Interest, except for interest arising from the ordinary business activities or closely related to the ordinary business activities of an individual | The whole amount (1) |

| Dividends | The whole amount (1) |

| Remuneration for first employments exercised in Cyprus commencing as from 1 January 2022 with remuneration exceeding EUR55.000 by individuals who were not residents of Cyprus for a period of 10 consecutive tax years immediately prior to the year of commencement of the employment in Cyprus. For each individual the exemption will apply once in their lifetime for a period of 17 years. Subject to certain conditions, individuals whose employment commenced prior to 1 January 2022, may also be eligible to claim the exemption. (2). | 50% of the remuneration |

| Remuneration for first employments exercised in Cyprus commencing after 26 July 2022, by individuals who immediately prior to the commencement of their employment in Cyprus were not a resident of Cyprus for a period of at least 3 consecutive tax years and were employed outside of Cyprus by a non-resident employer. For each individual the exemption will apply for a period of 7 years, starting from the tax year following the tax year of commencement of employment. Individuals granted the above 50% exemption will not be eligible for this exemption. (2) | 20% of the remuneration with a maximum amount of €8.550 annually |

| Remuneration from salaried services rendered outside Cyprus for more than 90 days in a tax year to a non-Cyprus resident employer or to a foreign permanent establishment of a Cyprus resident employer | The whole amount |

| Profits of a foreign permanent establishment under certain conditions (3) | The whole amount |

| Lump sum received by way of retiring gratuity, commutation of pension or compensation for death or injuries | The whole amount |

| Capital sums accruing to individuals from any payments to approved funds (e.g. provident funds) | The whole amount |

| Profits from the sale of securities (4) | The whole amount |

| Profits from the production of films, series and other related audiovisual programs | The lower of 35% of the eligible expenditure and 50% of the taxable income. Any restriction may be carried forward for 5 years. |

Notes:

1. Such dividend and interest income may be subject to Special Contribution for Defence - refer to the Special Contribution for Defence section.

2. Individuals that were eligible to claim the 20% or 50% exemptions that applied pre-1 January 2022 may continue to claim the said exemption for any remaining period if they are not eligible to claim the exemption for employments commencing as from 1 January 2022. The 20% and 50% exemptions that applied pre-1 January 2022 were available for a total period of 5 or 10 years respectively for each individual.

3. With effect as from 1 July 2016, taxpayers may elect to tax the profits earned by a foreign permanent establishment, with a tax credit for foreign taxes incurred on those foreign permanent establishment profits. Transitional rules apply in certain cases on the granting of foreign tax credits where a foreign permanent establishment was previously exempt and subsequently a taxpayer elects to be subject to tax on the profits of the foreign permanent establishment.

4. The term "Securities" is defined as shares, bonds, debentures, founders' shares and other securities of companies or other legal persons, incorporated in Cyprus or abroad and options thereon. Circulars have been issued by the Tax Authorities further clarifying what is included in the term Securities. According to the circulars the term includes, among others, options on Securities, short positions on Securities, futures/forwards on Securities, swaps on Securities, depositary receipts on Securities (ADRs, GDRs), rights of claim on bonds and debentures (rights on interest of these instruments are not included), index participations only if they result on Securities, repurchase agreements or Repos on Securities, units in open-end or close-end collective investment schemes. The circulars also clarify specific types of participation in foreign entities which are considered as Securities.

Tax deductions

The following are deducted from income:

| Contributions to trade unions or professional bodies | The whole amount |

| Loss of current year and previous years (for individuals required to prepare audited financial statements, current year losses and losses of the previous five years only may be deducted) | The whole amount |

| Rental income | 20% of gross rental income |

| Donations to approved charities (with receipts) | The whole amount |

| Expenditure incurred for the maintenance of a building in respect of which there is in force a Preservation Order | Up to €1.200, €1.100 or €700 per square meter (depending on the size of the building) |

| Social Insurance, General Health System medical fund, private medical fund insurance contributions (maximum 1,5% of remuneration), pension and provident fund contributions (maximum 10% of remuneration) and life insurance premiums (maximum 7% of the insured amount) | Up to 1/5 of the chargeable Income |

| Amount invested each tax year as from 1 January 2017 in approved innovative small and medium sized enterprises either directly or indirectly subject to conditions (applicable up to 31 December 2023). | Up to 50% of the taxable income as calculated prior to this deduction (subject to a maximum of €150.000 per year) (1) |

| Eligible infrastructure and technological equipment expenditure in the audiovisual industry | 20% |

| Expenditure of revenue nature for scientific research and for R&D, subject to conditions | The whole amount (and for expenditure incurred in years 2022, 2023 and 2024, an additional 20%) |

| Tax amortisation on any expenditure of capital nature for scientific research and for R&D, subject to conditions | The whole amount (and for expenditure incurred in years 2022, 2023 and 2024, an additional 20%) allocated over the lifetime of the asset (maximum period 20 years) |

Note

1. Unused deduction can be carried forward and claimed in the following 5 years, subject to the cap of 50% of taxable income (and overall maximum of €150.000 per year).

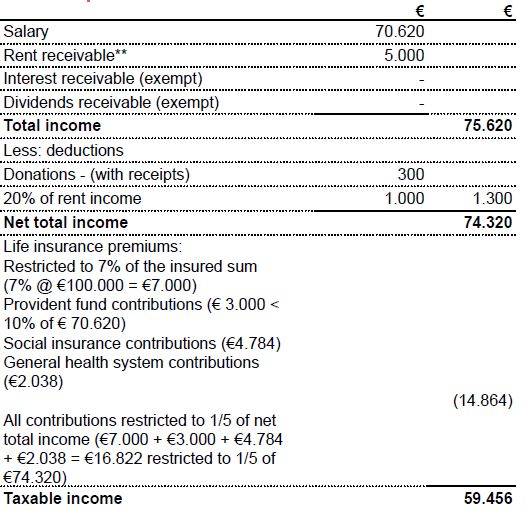

Example of personal Tax computation for 2022

| Salary (€5.885 monthly) | €70.620 |

| Rent receivable | €5.000 |

| Interest receivable | €700 |

| Dividend income | €600 |

| Social Insurance contributions | €4.784 |

| General health system contributions | €2.038 |

| Life insurance premiums | €8.500 |

| Insured sum | €100.000 |

| Provident fund contribution | €3.000 |

| Donations to approved charities – with Receipts | €300 |

Tax computation

*Please refer to Special Contribution for Defence section. The individual in this example is both Cyprus tax resident and Cyprus domiciled for the purposes of the Special Contribution for Defence.

** In regards to the immovable property on which rental income is earned, the deductions could additionally include any interest expense accruing on borrowings that were obtained by the individual to finance the acquisition of the building as well as wear and tear allowances (if not already exhausted).

To read this Report in full, please click here.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.