Introduction

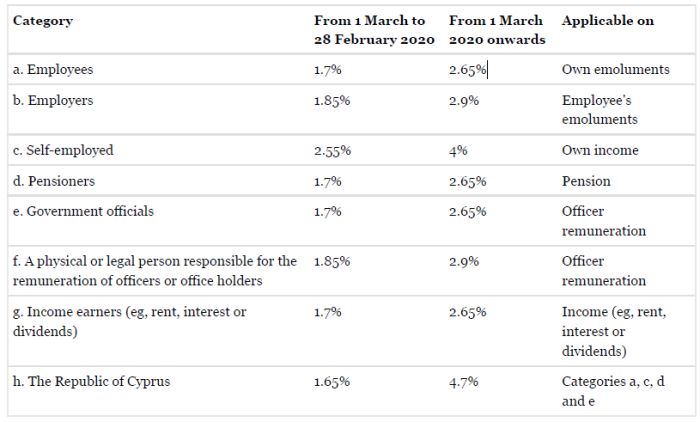

From 1 March 2019, employees, pensioners, state officials and income earners in Cyprus must contribute 1.7% of their income to the General Health System, while self-employed individuals will be required to contribute 2.55% of their income. The General Health System is a state-imposed universal healthcare system introduced in Cyprus by the National Health Insurance System Law 2010 (as amended in 2017).

Each private employer must also make General Health System contributions of 1.85% on emoluments made to employees, while the state must make an additional contribution of 1.65% of the income of employees, self-employed individuals, pensioners or government officials.

General Health System contributions must be made on all income earned up to a maximum of €180,000. The above contribution rates are set to increase on 1 March 2020, as set out below.

Payment methods

Employees' contributions

Employers are responsible for paying both their own and their employees' General Health System contributions through social insurance. The payment deadline and procedure are the same as those for social insurance payments and General Health System contributions are listed as a separate column in the updated version of the social insurance contribution form for each month. The maximum annual insurable earnings for employees applicable for Social Insurance Fund contributions do not apply in the case of the General Health System.

Selfemployed persons

Contributions relating to insurable earnings are paid through the Social Insurance Fund. Contributions based on the income of self-employed persons beyond these sums are paid to the tax commissioner.

Pensioners

Contributions are deducted by the payer and paid through the tax commissioner. Social Insurance Fund pensions are received net after General Health System deductions have been made, while contributions on pensions received from abroad must be paid by pensioners to the tax commissioner.

Government officials

The government deducts contributions from the pay of government officials which are paid through the tax commissioner.

Income earners

For dividends or interest received by an individual from a Cyprus source, a deduction is made by the payer and paid to the tax commissioner. For rents received by an individual from a Cyprus source:

- a deduction is made by the payer and paid to the tax commissioner if the payer is a company; or

- the recipient makes a payment to the tax commissioner if the payer is an individual.

For income from abroad, the recipient (income earner) makes a payment to the tax commissioner.

Where an individual is not a Cyprus tax resident, they will be required to pay contributions based on only the income, earnings and pensions that derive from Cyprus, excluding dividends and interest.

Contribution threshold

Contributions are paid on an individual's total annual earnings up to €180,000. Annual earnings are calculated according to the following hierarchy:

- employment salary;

- self-employed salary and officer;

- pensions; and

- income.

Where contributions in any calendar year are above the €180,000 threshold, the contributor should request the return of any excess amount paid from the Health Insurance Organisation.

Contribution rates

Originally published in International Law Office, 10 April 2019

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.