Some buy gold as a luxury good, in the form of jewellery, and some use it for investment, or both. It is a highly liquid asset that is also very scarce and unlike many other commodities it is not used. It is no one's liability. Being an element there is as much gold today as there was thousands, or even millions of years ago. The World Gold Council outlines four fundamental roles that holding gold plays in a portfolio which are discussed in depth here under:

As a source of long-term returns

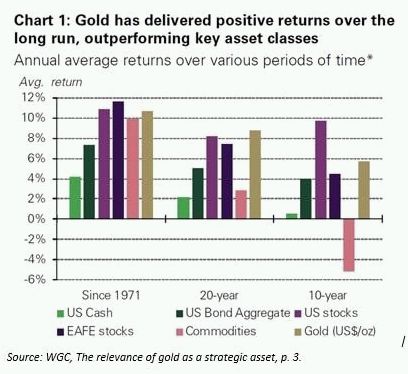

Gold is valuable. It has been used in history as a form of money and today is used as a store of wealth. The price of gold has increased by an average of 10% year on year since 1971 when it began to be freely traded. Gold's long-term results are comparable to stocks and actually higher than bonds or commodities. Gold's value increases and price surges in times of market stress as opposed to other key asset classes, as witnessed during the 2008 financial crisis. We saw a 150% gain in the value of gold while on the other hand stocks crashed. As such, even a small allocation in gold would have offset the unfavourable returns elsewhere. It would also have provided security and a peace of mind when the banks crashed, provided gold was not stored in that specific bank and instead at a designated private physical storage company on segregated and allocated basis (such as Liemeta ME Ltd). For in depth information on the forms of gold storage please read our article: Physical Gold Storage.

Wealth preservation often only matters at certain times and that is usually during times of turmoil, war, currency debasement and financial troubles. Since these are too difficult to accurately predict it is always a good idea to have a small allocation of your portfolio in gold (as a rule of thumb: 7-15% approximately). Thus enhancing overall asset performance.

"Gold has not just preserved capital but has helped capital grow." It has consistently outpaced inflation:

During the past 8 years Central Banks have been net-buyers of gold. During the first quarter of 2019, central banks bought a total of 145,5 tonnes of gold which is 68% percent more than a year earlier and a 7% increase in global gold demand for that period.

As a portfolio diversification tool to mitigate losses during times of market stress

It is not the standalone performance of gold that works, it is its stature as an example of "diversification that works", as the WGC says. During times of rising correlations between other asset classes, gold remains reserved for most of the time. Extreme times then send people away and towards gold. During the 2008-09 crisis, for example, "hedge funds, broad commodities and real estate, long deemed portfolio diversifiers, sold off alongside stocks and other risk assets." That was not, though, true of gold.

Gold investors benefit from both the fact that the gold market is deep and liquid. By the WGC's estimates, "physical gold holdings by investors and central banks are worth approximately US$2.9 trillion, with an additional US$400 billion" as open interest via the gold derivatives markets. There is definitely some depth there.

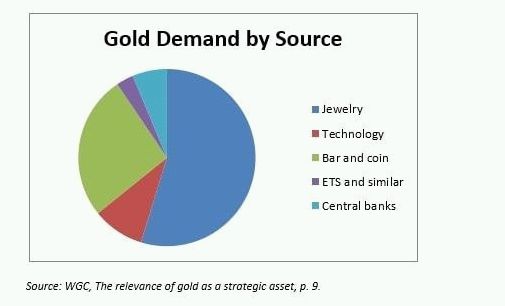

The source of gold demand for its value as diversification looks like this:

As to the liquidity of the gold market we get transactions between US$ 150 billion to US$ 220 billion per day. This is the combined figure of both spot and derivatives OTC markets.

The average trading volume in gold exceeds the trading volume of all stocks in the S&P 500, for example.

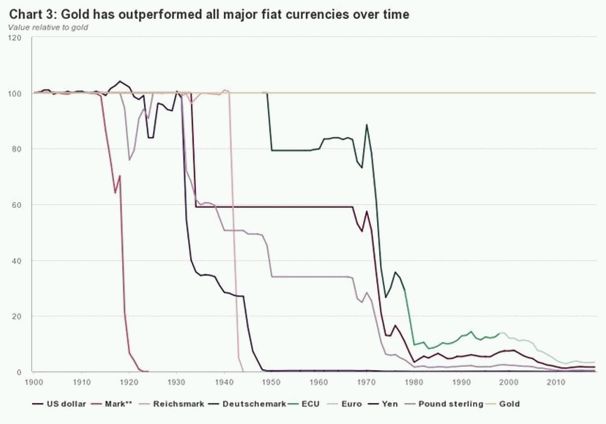

It is a liquid asset with no credit risk that has outperformed fiat currencies

Gold is rare and gold is finite. Fiat money on the contrary can be printed in unlimited quantities to support monetary policies.

Gold goes beyond commodities

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.