This is the first entry in a two-part discussion on the documentation requirements to claim Input Tax Credits (ITCs) for Goods and Services Tax / Harmonized Sales Tax (GST / HST) purposes.

To begin, I'm focusing in on exactly what is required to substantiate an ITC claim. Note that this blog has been written under the assumption that the business has already taken the steps to ensure it is eligible to claim ITCs in respect of its commercial activities.

A business that is registered for GST / HST purposes is entitled to ITCs for the tax paid on business inputs used in commercial activities. The business must retain proper documentation to substantiate the claim. However, the documentation requirements are onerous and businesses often find themselves caught off guard during a GST / HST audit, with ITCs being denied due to unexpected issues with the invoices.

Prescribed Information

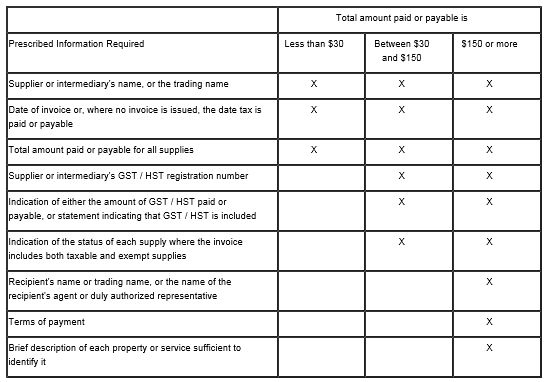

The Excise Tax Act (ETA) prescribes a list of information that must be present on an invoice in order for the recipient of that supply to claim ITCs. The information required is different depending on the dollar value of the invoice. For smaller amounts the requirement is less stringent and vice versa.

As a business that claims ITCs, it is crucial to ensure all required information is present on the invoice.

The required information is summarized as follows:

Exceptions

There are a number of exceptions to the rules outlined above. For a complete list of the exceptions, please refer to New Memorandum 8.4. Some of the notable exceptions are expense reports filed by employees, computerized records, contractual agreements, allowances, and taxi fares.

Best Practice

It is nearly impossible to ensure all your expenditures meet the documentation requirements. At a minimum it is recommended you perform a periodic check of large capital purchases and expenses. Perhaps on a monthly basis review the invoices for all expenditures over a certain dollar amount or the largest 10 to 20 invoices. Building this practice into the month-end process will help make the period checks a priority. The objective is to ensure the documentation requirements are met on the larger expenditures and deal with any issues before an auditor calls. For example, if a particular invoice doesn't have the supplier's registration number present, you can ask the supplier to re-issue the invoice.

While the documentation requirements may seem straightforward, the application of them has some interesting implications. I'll discuss more of the issues and pitfalls in my next installment.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.