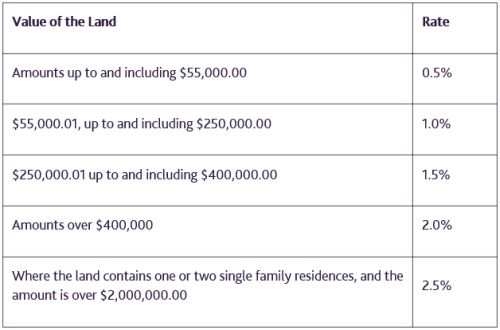

As of January 1, 2017, there are new land transfer tax ("LTT") tax rates applicable to the purchase of land (residential and commercial) in Ontario. The new tax rates are as follows:

The new tax rates apply to all purchases of land where: (1) the agreement of purchase and sale was entered into after November 14, 2016; and (2) the transaction closes on or after January 1, 2017.

A Comparison of the old and new LTT rates (applicable to properties not in Toronto)

Sample LTT calculation using old LTT rates

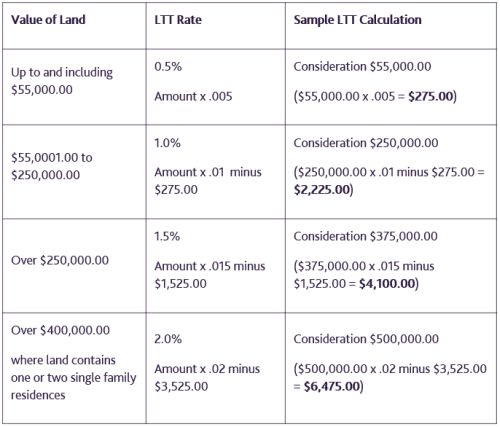

Sample LTT calculation using new LTT rates

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.