New CSA guidance highlights the importance of climate change-related disclosure to securities regulators and investors and aims to assist issuers in identifying, and improving disclosure of, material risks posed by climate change.

The Canadian Securities Administrators (CSA) recently published CSA Staff Notice 51-358 Reporting of Climate Change-related Risks (the Notice). The Notice was motivated by increased investor interest in climate change-related risks, particularly among institutional investors, the CSA's view that issuers' existing disclosure with respect to climate change can be improved, and the large number of reports on climate change disclosure and other environmental governance topics over the last several years.

The Notice does not create any new legal requirements but expands upon the guidance regarding continuous disclosure requirements relating to climate change previously provided in CSA Staff Notice 51-333 Environmental Reporting Guidance.

Considerations for Directors and Management

The Notice highlights the respective roles of management and the board (and audit committee) in strategic planning, risk oversight and the review and approval of an issuer's annual and interim regulatory filings. While intended solely as an educational tool, the Notice generally suggests the following practices for an issuer's board of directors and management:

- Ensure that the board of directors and management has, or has access to, appropriate sector-specific climate change-related expertise to understand and manage climate change-related risk.

- Establish disclosure controls and procedures designed to collect and communicate climate change-related information to management to allow for the assessment of materiality and, as applicable, timely disclosure.

- Consider whether climate change-related risks and opportunities are integrated into the issuer's strategic plan.

- Assess whether the issuer's risk management systems and methodology, including business unit responsibility, appropriately identify, disclose and manage climate change-related risks.

- Avoid vague and boilerplate climate change-related disclosure.

- Review the CSA's select questions for boards and management designed to inform the assessment of climate change-related risk.

Materiality in the Climate Change Context

Canadian securities regulation mandates the disclosure of material information and provides guiding principles for determining materiality. The Notice is clear that the assessment of materiality in the context of climate change-related risk is no different.

The Notice emphasizes that climate change-related risks and their potential financial impacts are mainstream business issues. While climate change-related risks may differ from other business risks due to our evolving understanding of these risks, the potential difficulty in quantifying these risks and the potentially longer time horizon, boards and management should take appropriate steps to understand and assess the materiality of climate change-related risks to their business.

The Notice highlights certain specific considerations for determining materiality in the context of climate change-related risks:

- Timing – Issuers should not limit their materiality assessment to short-term risks. The uncertainty and time horizon of a risk occurring may impact the assessment of whether the risk is material but not whether it needs to be considered and analyzed as to materiality.

- Measurement – Boards and management should consider the current and future financial impacts of material climate change-related risks on the issuer's assets, liabilities, revenues, expenses and cash flows over the short, medium and long-term. Where practicable, issuers should quantify and disclose the potential financial and other impact(s) of climate change-related risks, including their magnitude and timing.

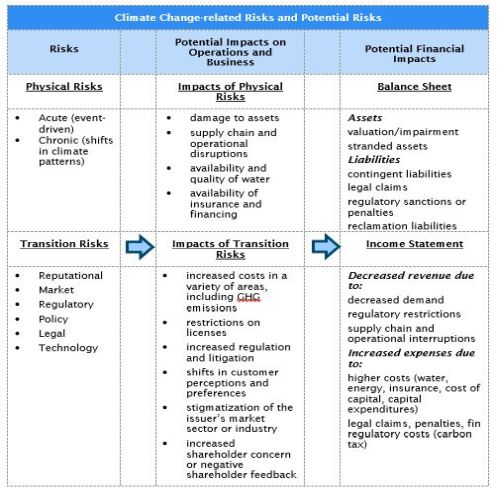

- Categorization of Risk and Potential Impact – The Notice provides helpful guidelines for thinking about climate change-related risk and its potential financial, operational and business impacts, as illustrated in the below chart:

Conclusion

While it does not create any new disclosure requirements, the Notice, in conjunction with increased interest from institutional investors and other stakeholders in climate change-related risk, may signal other forthcoming policy initiatives focused on climate change and the capital markets. The CSA will continue to monitor disclosure of climate change-related matters as part of its ongoing continuous disclosure review program.

In the meantime, boards and management should consider their existing practices with respect to collecting and communicating climate information and the assessment and disclosure of climate change-related risk. Furthermore, issuers should consider how this new CSA guidance may impact the risk factor sections of their quarterly and annual MD&A and annual information form going forward.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.