On 9 April 2024, the Australian Government released the exposure draft to reduce the managed investment trust (MIT) withholding tax rate from 30% to 15%. These measures were previously announced in the 2023-24 Federal Budget. The proposed reform promises to encourage more foreign investment in Australia's growing Build-to-Rent (BTR) market. But, do the changes go far enough?

This article examines the Government's proposed changes, its potential limitations and what further detail is needed. We highlight the State and Territory BTR incentives on offer and discuss the final piece in the puzzle: GST.

Reduced MIT withholding rate and increased capital works deductions

The Government has proposed to reduce the MIT withholding tax rate from 30% to 15% for eligible BTR projects from 1 July 2024 throughout a 15 year concession period (after which the MIT withholding tax rate will be increased to 30%). The measures also propose to increase the capital works depreciation rate for eligible BTR projects to 4% (from 2.5%), which can extend beyond the 15 year concession period.

To be an eligible BTR project (referred to as an "active BTR development"):

- Construction must commence after 7:30pm (AEST) on 9 May 2023 (i.e., after the proposed changes were announced in the 2023-24 Federal Budget).

- The project must have at least 50 dwellings or apartments made available to rent to the general public. The Government has conceded that concessions should be available to repurposed buildings for BTR (which we expect is likely to be attractive to developers, asset managers and investors). The BTR development can be part of a building, or include multiple buildings.

- The dwellings (and common areas that form part of the BTR development) must be retained by a single entity, at any one time, for at least 15 years before being sold (whereas the 2023-24 Federal Budget indicated a shorter 10 year single ownership period). The Government has conceded that a BTR development can be sold to another single entity during that period and still access the concessions, provided the new owner retains ownership throughout the balance of the 15 year concession period.

- Each dwelling must be offered for a term of at least 3 years (although the tenant can request a shorter term) throughout the 15 year concession period.

- At least 10% of the dwellings are available as affordable tenancies throughout the 15 year concession period. To be affordable tenancies, the owner must offer at least one of each apartment/dwelling type at discounted rent to eligible tenants. Discounted rent must be 74.9% or less of market rent. Tenants must meet income limits that will be set out in regulations.

There will also be BTR reporting obligations throughout the 15 year concession period (including evidence of tenant eligibility).

The Government has also introduced a "BTR misuse tax" which operates to clawback the tax benefits claimed by taxpayers where the BTR development ceases to qualify during the 15 year concession period. Broadly, the BTR misuse tax is expected to equal:

- 16.2% of the MIT fund payments that are attributable to the BTR development (i.e., 15% tax rate multiplied by 1.08, intended to represent interest and costs associate with the tax shortfall); and

- 1.62% of the accelerated capital works deductions (i.e, 1.5% accelerated deduction multiplied by 1.08, again intended to represent interest and costs associate with the tax shortfall) which is taxed at a 45% rate for trustee companies. That is, the BTR capital works deduction benefit is taxed at the highest rate and not the MIT withholding tax rate.

Prima facie, the Commissioner would issue the assessment to the MIT trustee, and will likely be a key area of focus in managing compliance annually and in diligence where BTR projects are transacted. This tax was not included in the 2023-24 Federal Budget announcement.

Consultation is open until 22 April 2024.

The change brings the withholding tax rate for BTR in-line with other real estate asset classes (like office, industrial and retail) for a limited period. The incentive is available for foreign investors located in 'information exchange countries' who invest in eligible MITs in Australia. Although the reduced withholding tax rate only applies to foreign investors, the change widens the pool of capital for Australian REITs and local fund managers.

Whilst a welcome development, there are a number of areas which require further thought by the Government, including:

- Existing BTR assets and projects for which construction commenced prior to 9 May 2023 are likely to be left 'stranded' under the 30% tax rate regime, and be ineligible for the proposed concessions (including where transacted in the future). This creates differential outcomes for BTR developments which might be similar in all aspects other than the date of construction. This creates a tension with the Government's aim of increasing rental housing supply, as BTR projects not eligible for concessional treatment may be more likely to leave the rental market in one form or another.

- The 15% tax rate will only be available throughout the 15 year concession period. This would appear to remove the incentive for asset managers and investors to continue to make the BTR development available for long term and/or affordable tenancies after this period lapses. How this will impact the value of "old" BTR developments, and the migration of capital from old to new BTR developments, is yet to be seen.

- The requirement to maintain single ownership during the 15 year concession period does not appear to restrict changes in ownership of the MIT that owns the BTR development. This may allow transacting in BTR projects at the entity level to introduce new investors to fund development of expansions and new BTR projects under the same fund.

Developers and asset managers will also need to consider whether the minimum number of dwellings/apartments, minimum holding period and minimum lease term are commercially viable in funding the development of new BTR projects. Additional processes will also need to be put in place to address the new BTR reporting requirements and to assess the satisfaction of the affordable tenancies requirements.

States and Territories have different eligibility requirements for their BTR concessions, meaning it is possible for certain projects to be eligible for the Federal withholding tax concessions but not a State-based concession and vice-versa. Broadly, it is expected that the Federal BTR requirements will be the least restrictive although there may be some nuances (e.g., Western Australia only requires 40 dwellings).

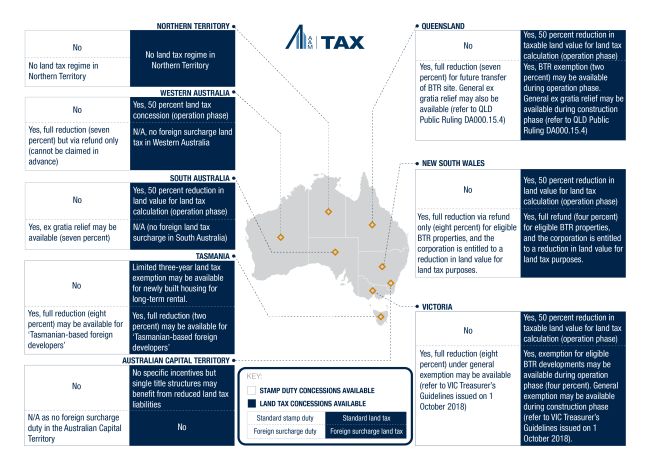

Duty and land tax concessions

The majority of the Australian States and Territories impose stamp duty and land tax surcharges in respect of residential land / property acquired or held by foreign persons. Specifically, surcharge duty of up to 8% (in addition to ordinary stamp duty) can apply to purchases of residential property by foreign persons, while surcharge land tax at a rate of up to 4% can apply each land tax year to foreign owned land.

In this regard, concessions from the foreign duty and land tax surcharges are available for eligible BTR projects in certain jurisdictions. The table below summarises the key concessions available in each of the jurisdictions (either announced or enacted):

The requirements to access the concessions outlined above vary between each State/Territory. Many of the requirements are aligned to the announced Federal BTR requirements, although additional requirements may apply. For example, New South Wales (NSW) requires at least 10% of the construction labour hours to involve work from certain classes of workers i.e., apprentices/trainees, long-term unemployed workers and Indigenous Australian job seekers.

Care should be taken with multi-stage developments and consideration should be given as to whether each stage has the required number of dwellings to qualify for the relevant concessions. Further, where land is jointly owned by an Australian and foreign entity, care should be taken to ensure no inadvertent consequences arise with respect to foreign acquirer surcharge duty and foreign owner land tax.

GST

While different GST treatments can apply depending on the type, and potential mix, of properties being built, BTR properties are generally treated as being input taxed, meaning no GST arises on the rent and on sale (provided the premises has been leased for 5 years). However, no input tax credits are available for any GST incurred on costs relating to such input taxed rent and sale, which effectively adds 10% to the acquisition, development and operational costs of a BTR project.

This GST leakage is likely to be a significant barrier to some BTR projects and further investment, particularly when compared with projects for new residential sale or commercial lease for which input tax credits are available.

Final word

The proposed Federal BTR incentives are a welcome change in tax policy which, alongside State and Territory incentives, should break down some of the barriers to BTR investment in Australia. However, further changes to the GST rules could still be made to align BTR with other asset classes.

Given the varying and detailed Federal and State/Territory eligibility requirements, the A&M Real Estate Tax team is available to assist clients at the planning stage to assess the tax and duty concessions that may be on offer to incentivise investment in new BTR projects.

Originally published by 10 April, 2024

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.