Preface to the Series

The advent of blockchain technology in the year 2009 has completely revolutionised the digital space. The idea of creating a universal, entirely decentralised network for carrying out transactions of a myriad nature has forced us to re-think the capabilities and limitations of the internet. While blockchain technology holds the future and the key to ensuring ease of carrying out transactions over the digital space, the same has also led us to contemplate some very pertinent questions as to the legality of such transactions devoid of any laws or regulations overlooking the same. A blockchain network that is transnational in nature also leads us to examine how our existing territorially limited laws can ensure supervision over transactions happening over such a vast network.

The present series seeks to examine some of these raging questions that need to be discussed, deliberated and answered. The series has been divided and presented into multiple, separate, comprehensive parts, with each part dealing with a specific subject. The first paper in the series is presented in three parts, wherein the first part will capture the intricacies of the blockchain network, its essential characteristics and types, while the second part will discuss blockchain from a legal perspective and will set out the measures adopted by various sectoral regulators in India, the third and final part shall discuss the initiatives of various States in India in advancing the implementation of the technology. The forthcoming parts in the series aim to analyse the interaction of the technology with distinct legal practices such as Data Privacy, Arbitration, Dispute Resolution, Corporate Transactions, Intellectual Property Rights etc.

PART A | BLOCKCHAIN TECHNOLOGY – THE SCIENCE BEHIND THE REVOLUTION

A) Introduction

As the world advances towards a digital revolution, it has led to the birth of a decentralised world that seeks to self-govern and not rely upon a central authority of power to sustain and survive. It is a world that is increasingly controlled by codes, hash, programming to name a few. This system of decentralised power over the internet arises from a general mistrust of central structures, established rules of conduct (overregulation) and governance that seeks to promote an era of digital anarchy.

The name 'blockchain' stems from its technical structure — a chain of blocks. Each block is chronologically linked to the previous block via a cryptographic hash. A block is a data structure that allows each system to store a list of transactions/information. Transactions are created and exchanged by peers of the blockchain network which modify the state of the blockchain. As such, transactions can exchange monetary amounts, but are not restricted to financial transactions only and even allow the execution of arbitrary code within so called smart contracts.1

Blockchain was created to support a uniform, secure, decentralised system for sustaining the transfer of value-based crypto assets. The technology that first made its appearance in 2008 in a paper written by Satoshi Nakamoto2 (a pseudonym), was directed towards creating a decentralised online economy which did not require a central authority to sustain or govern the system, one that was beyond borders, and their concomitant rules and regulations. In essence, blockchain technology was as big of a revolution as the creation of the internet, combining a rebellion against all sources of power with the genius of cryptography so much so that it seems almost ironical that during the current times governments across the globe have started channelling the usage of the technology having realised the potential it possesses. While Nakamoto's paper only sought to utilise blockchain technology for enabling the transfer of cryptocurrencies, more specifically bitcoins, this is merely a singular application of the revolutionary technology. The genius behind the technology lies in the distributed ledger system that it works on.

Interestingly, cryptocurrencies unlike tangible currencies are easier to copy and may be re-utilised since these constitute completely digital transactions leaving no trace in the tangible world especially in absence of a central authority. This issue was witnessed by DigiCash which was created by cryptographer David Chaum in 1994.3 Digicash relied upon Chaum's company to validate all transactions and unfortunately, when his company went bankrupt in 1998, DigiCash went down with it.4

Blockchain showcased an elegant solution to this problem of double spending and continued reliance on a central regulatory figure. Blockchain permitted mutually mistrusting entities to perform financial payments without relying on a central trusted third party while offering a transparent and integrity protected data storage.5 Due to these properties, blockchain as a technology has gained much attention beyond the purpose of financial transactions – with the technology being utilised across various fields and services, such as financial market, IOT, supply chain, medical treatment, voting, storage and decentralized autonomous organizations to name a few.6

B) Blockchain Technology- How does it work

What is a Blockchain?

Blockchain, has been defined as a digital, decentralised (distributed) ledger that keeps a record of all transactions that take place across a peer-to-peer network.7 A peer-to-peer network allows all participants within the network to share files, resources and data that does not separately require a main server computer.8 Blockchain may also be conceived as a transparent distributed database that records details of all transactions performed by the system's participants.9

Put simply, a blockchain stores a record of information (as a ledger) that does not require a central authority to govern the network (decentralised). The technology is powered by an interconnected network of participants (nodes or miners), that lend to the network the unique characteristics of being decentralised and distributed.

Nodes

A blockchain network is a multi-layered dimension in itself with several systems or nodes connected to the network, with no third-party interference or control. A node could be a laptop, a computer, or even a small server. Each node over a blockchain network stores the entire record of transactions over the network. These nodes are linked together by a software protocol which governs the blockchain network.

If we are to draw a parallel between a banking system and a blockchain, the similarity lies in the fact that both systems need to store information with respect to transactions. While banks store the information on a private and centralised system, the storage system in a blockchain is completely different and unique with the entire blockchain functioning as a giant, decentralised ledger that stores information.10 Each node over a blockchain network stores a copy of the information/transactions over the network, such that there is no central single system serving as a ledger for the information. The records so saved gets automatically updated whenever a new transaction is added to a block.

Interestingly, while a technical glitch in the central server of a bank that stores the records of all transactions might cause a massive uproar, the same would just never happen on a blockchain network because even if one 'node' (i.e. a system) fails to function or experiences a glitch of some sort, the remaining network of nodes would still hold a copy of the records in the ledger. Another major difference between a bank ledger and the decentralised ledger is that while all nodes have access to the records stored over a blockchain network the same is not the case in a bank ledger which is subject to restricted access and any steps to access the records without authorisation might land one in prison. This system also allows all nodes over the network to validate and authenticate each and every transaction before it can be stored on a block.

11

11

The above figure is a classic representation of a decentralised ledger. Alice who wants to send cryptocurrency over the network to Bob will have to do the same through a network of nodes spread across the globe. Once the transaction has been validated through a consensus mechanism, the records maintained by every node over the system will get automatically updated.

Miners

Certain set of nodes who perform a more specialised function are referred to as 'miners'. A 'miner' is a node in the network who works towards authenticating a transaction. Simply put miners are nodes who have invested in higher levels of programming, specialised mining software and computer power that enables them to carry out extremely complex computational tasks in order to validate a transaction. While all miners are nodes, all nodes may or may not be miners.

Any person who wishes to join a blockchain network as a miner only needs to create an account over a platform that gives access to the network, and additionally invest in specialised computer software and programming powers. Upon doing the same, the person (or in essence his system) may become a miner and thereafter may participate in validating transactions. In reality, it is not the individual miner who authenticates the transaction, rather it is the system that performs extremely complex tasks using hashing functions (SHA-256) towards authenticating the transaction. The process of performing SHA-256 hash twice to arrive at a winning lottery number which is less than a target threshold, which in turn can then be used to authenticate and add new blocks of information to the blockchain, is known as mining. In exchange for the task of authenticating, miners are incentivised with a block reward by the network.

Public and Private Keys

Blockchains possess the capacity to function on a transparent, public network, where the identities of nodes and miners are hidden away with private keys and encryptions. Every node over the network has a public key and a private key that are paired together. While a public key is visible to all and could be considered akin to an email address, the private key is more like a password and is possessed by the node only. The private key attaches authenticity to any information sent out by the node or any transaction made by attaching a digital signature to the transaction and the private key is only known to the miner/node it belongs to.12

Validating a Record and Proof of Work

For a transaction to be validated over a blockchain network, each miner over the network performs the SHA- 256 hash twice in the hope that the said hash will provide a number lesser than a target threshold. Essentially, it is like performing a long mathematical division and hoping that the number arrived at is a single digit. The miners/computers are expending huge amounts of energy hoping that it would randomly pick a winning lottery number (and not a mathematical puzzle as is commonly misunderstood) which will allow the miner to claim that they have the next block and thus entitled to the next block reward.13

Hashing is an integral part of the process because it assists other nodes in authenticating or tracing the transaction. While mining and hashing techniques are complicated and a detailed explainer on these is outside the purview of this paper, it is safe to say that mining involves a game of trial and error by each miner until one hits the jackpot by creating a valid hash and authenticating the transaction. A miner's system has to keep generating hash numbers till one wins the gamble. The Bitcoin network typically uses the Secure Hashing Algorithm 256 (SHA-256) that performs the task of reducing every input transaction to a fixed output length of 256 bytes. This means no matter the input length of the data, the output length is always fixed.

Before the block with the validated information can be added to the blockchain, the same has to be verified by a majority of nodes over the system. These nodes run a simple calculation in order to ensure that the hash output so generated is valid and abides by the network protocol. This system of verification ensures that only authentic data has been stored on a block. Once the block has been verified, it is added to the network.

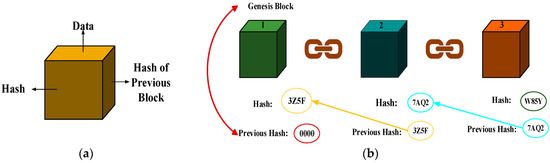

What does a Block comprise of?

Every validated transaction is stored on a block which is then added to the chain. Each block over a network comprises of four components: (a) Timestamp; (b) Nonce & Difficulty; (c) Hash of the present block; and (d) Hash of the previous block.

When a miner attains the winning lottery number, it generates a unique hash number that attaches validity to the transaction. A hash is a unique 64 digit hexadecimal number that operates as a unique fingerprint for each block. Instead of searching for a certain transaction in a network of thousands of blocks, every transaction can simply be traced through its unique hash.14 The hash so generated is authenticated by a majority of nodes over the network, once authenticated the transaction gets recorded in a block.

A block does not simply record the hash of its own data, it also stores the hash of the previous block. However, the first block in a blockchain (called the 'Genesis Block') cannot point towards the hash of a previous block. The Genesis Block depicts the previous hash value as 0.15 This feature lends to blockchain network a certain amount of authenticity, since modifying the hash of a particular block would necessarily require modification of the hashes contained in all other preceding blocks over the network. Accomplishing this would require a node or a miner to possess extremely fast computational power that changes the hash numbers of the blocks faster than they are created.

In addition to the hash, each block over the blockchain network also consists of a nonce number. This number is appended to the block header, and miners must guess this nonce number through trial and error in order to get through to the hash value.16

17

17

Consensus Algorithm and Forks

A blockchain network has no centralised authority to govern and regulate the system. All the decisions over the network have to be made by the network of nodes by reaching a consensus. The consensus mechanism may manifest itself in several ways over a blockchain network. For instance, consensus may be said to be achieved when a majority of the nodes validate the hash generated by the miner and create a consensus that the block should be added to the blockchain (the proof-of-work consensus).18 This consensus is of utmost significance on the network due to the lack of a central authority.

This consensus forms the grundnorm upon which the blockchain subsists. However, in some cases, the nodes may be unable to come to a consensus as to a certain transaction. This is where a 'fork' or a split is created. A fork results in creation of a new chain of blocks stemming from the previous chain. The fork created may be a soft fork, one that does not alter the validity of the old chain, however, it may also be a hard fork, one wherein the new chain cannot be validated with the old rules, and a consensus is needed as to which chain of blocks should prevail.19

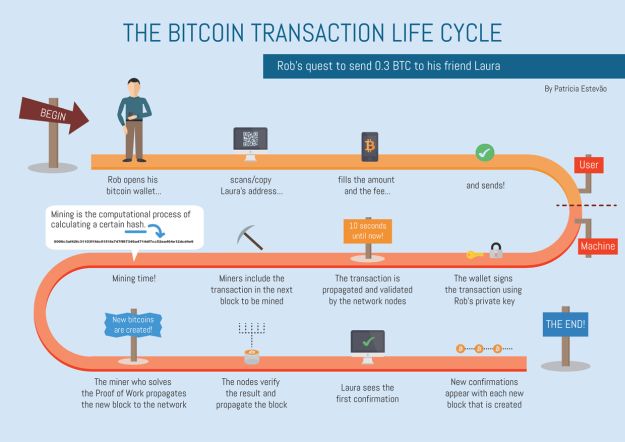

Bitcoin transaction cycle

The diagram below elaborates how a transaction is undertaken on a bitcoin network:

20

20

C) Characteristics of blockchain technology

Blockchain networks carry a unique set of characteristics, few being:

Decentralised Network

Like the internet, blockchain network transcends borders and functions seamlessly. Nodes over a blockchain network may be spread across the globe each possessing a copy of all transactions taking place over the network. This decentralised network of nodes spread across the globe constitute the real authority over a blockchain network responsible for keeping the network up and running. There is no central authority governing the activities over the network, no central server holding all records together. The nodes over the network operate together in-tandem with each other to verify transactions, adding a block to the chain, and serving as individual ledgers with updated record of all transactions taking place over the network.

Consensus-based mechanism

The blockchain network functions on a pre-defined consensus mechanism. The consensus that has to be reached among the nodes over the network accords to the network its unique characteristics, constituting the ability to remain decentralised, and rendering data stored over the network non-repudiable. For validating and recording a new transaction over the network, a consensus of nodes would have to be achieved. The consensus mechanism allows users to trust the network without the need of knowing the identity of other nodes.

Tamper proof network and non-repudiable data

The soul of a blockchain network lies in the fact that there is no central power figure in the system. If we imagine a blockchain network to be a nation in itself, it would be a nation run by the individual citizens all of whom have equal power to run the same, build aspects that they want, and most importantly simultaneous and uniform access to information. Relying upon the same analogy, on a blockchain network, citizens are replaced by the individual nodes in the system. All of these nodes have equivalent and universal powers. All of them have the capacity to authenticate or validate transactions broadcasted over the network, although they must compete to achieve the valid hash.

While the records of transactions stored on a block are accessible to all nodes over the network, the data stored on a block cannot be modified or deleted. If data over a block is indeed to be modified or deleted, it would require a consensus of more than half the number of miners or nodes over a system, that is, about 51% of the system would have to collude in order to attain the objective.21 This would mean convincing a majority of anonymous nodes over the system to tamper the data, which on the face of it may be challenging.

Also, since all records are stored with a unique hash and every block is timestamped, tampering with one block will trigger the requirement to modify all the previous blocks which will require massive computational power especially in order to attain 51% consensus.22 This unique characteristic essentially makes a blockchain network tamper-proof and resilient to change. This may be of great benefit in several sectors (especially financial sector) that must necessarily rely upon the tamper proof nature of records, for instance, banking and financial sectors.

D) Types of Blockchains

While all blockchains operate in a similar manner, blockchains may be of three types depending upon the extent of accessibility to the system:

- Public Blockchains- This is an open, free network where anyone can create an ID and join the network. Each user joining the network forms a node and is automatically granted the power to authenticate transactions, or access the data stored in blocks. In a public blockchain network, there is no central authority who owns or grants access to the network thus keeping it free for access by all. The bitcoin network is the best example of a public network in which anyone can participate and get full access to the entire network.

- Private Blockchains- Private blockchains are generally used by entities who do not wish their data to be accessible to the general public. A private blockchain is equivalent to an intranet system installed by entities to make local data sharing fast and efficient. In a private blockchain only identified users have the permission to access the network and the underlying transactions. The permissioned users are given access by the respective authority in-charge of the blockchain network.

- Consortium Blockchains- Consortium blockchains are a hybrid of public and private blockchains. While private blockchain networks might have a single organisation controlling access to the system, in a consortium network the system is controlled by several organisations pooling in together. The same may be beneficial for organisations with a common desired objective. For instance, about 94 companies signed up to be a part of the IBM/Maersk Blockchain based supply chain initiative.23 Similar consortium blockchains may be formed in specific sectors such as healthcare and banking.

E) Conclusion

Blockchain technology constitutes one of the most potent digital revolutions of our times and it is here to stay. With consistent research and efforts on in the field in order to make it more compatible with distinct sectors, the technology is bound to be closely tied up with digital advancements in the near future.

While the technology may prove to be quite beneficial when applied across sectors, certain concerns may arise. While the inherent decentralised, tamper-free nature of the technology lends certain benefits and advantages to the network, the same characteristics also bring forth a plethora of challenges. These concerns arising from the interplay of the technology with the law and various sectoral regulators shall be discussed in the second part of this paper.

Footnotes

1. Karl Wüst & Arthur Gervais, Do you need a Blockchain?, (April 27, 2020, 10:33 am), https://eprint.iacr.org/2017/375.pdf.

2. Satoshi Nakamoto, Bitcoin: A Peer-to-Peer Electronic Cash System, (April 28, 2020, 11:01 am), BITCOIN.ORG, https://bitcoin.org/bitcoin.pdf.

3. Aaron Wright & Primavera De Filippi, BLOCKCHAIN AND THE LAW 19 (2018).

4. Id.

5. Supra note 2.

6. Iuon-Chang Lin & Tzu-Chun Liao, A Survey of Blockchain Security Issues and Challenges, INTERNATIONAL JOURNAL OF NETWORK SECURITY, Vol.19, No.5, 653-659 (2017).

7. Blockchain: the next innovation to make our cities smarter, (May 18, 2020, 11:10 am), FICCI-PWC, http://ficci.in/spdocument/22934/Blockchain.pdf.

8. James Cope, What's a Peer-to-Peer Network?, (April 27, 2020, 13:30 PM), https://www.computerworld.com/article/2588287/networking-peer-to-peer-network.html.

9. Balamurali K., 2020: an Era of b-Governance Blockchain, 21ST NATIONAL CONFERENCE ON E-GOVERNANCE - COMPENDIUM OF SELECTED PAPERS, 2020, DEP. OF ADMINISTRATIVE REFORMS & PUBLIC GRIEVANCES, GOVT. OF INDIA, 69, 73.

10. The Economist, Blockchain The Next Big Thing, Or Is It?, (April 27, 2020, 13:30 PM), https://www.economist.com/special-report/2015/05/07/the-next-big-thing.

11. CB Insights, What is Blockchain Technology?, [image], (April 27, 2020, 13:30 PM), https://www.cbinsights.com/research/what-is-blockchain-technology/.

12. Leon Di, Why do I Need a Public and Private Key over a Blockchain? (June 08, 2020, 19:13 PM), https://blog.wetrust.io/why-do-i-need-a-public-and-private-key-on-the-blockchain-c2ea74a69e76.

13. Keir Finlow Bates, https://www.linkedin.com/feed/update/urn:li:activity:6678487266249314304/ .

14. Online Hashcrack, Hashing in Blockchain Explained, (April 27, 2020, 15:00 PM), https://www.onlinehashcrack.com/how-to-hashing-in-blockchain-explained.php.

15. Medium, What is Genesis Block and Why Genesis Block is needed?, (May 16, 2020, 10:00 PM), https://medium.com/@tecracoin/what-is-genesis-block-and-why-genesis-block-is-needed-1b37d4b75e43.

16. Jake Frankenfield, Nonce (May 16, 2020, 10:00 AM) https://www.investopedia.com/terms/n/nonce.asp.

17. Hash of the previous block, [image], (May 9, 2020, 8:45 pm), https://www.mdpi.com/J/J-02-00021/article_deploy/html/images/J-02-00021-g002-550.jpg.

18. Investopedia, Consensus Mechanism (Cryptocurrency), (May 16, 2020, 14:30 PM), https://www.investopedia.com/terms/c/consensus-mechanism-cryptocurrency.asp.

19. Geeks for Geeks, Blockchain Forks, (May 15, 2020, 11:57 PM), https://www.geeksforgeeks.org/blockchain-forks/.

20. How Bitcoin Transactions Work?, [image], (June 10, 2020, 13:28 PM), https://janzac.com/how-bitcoin-transaction-works/.

21. The Economist, supra note 10.

22. Aaron Wright, supra note 3, at 36.

23 Darya Yafimava, What are Consortium Blockchains and What Purpose Do they Serve?, (April 29, 2020, 9:00 AM), https://openledger.info/insights/consortium-blockchains/.

Originally published 6 August 2020

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.