On December 15, 2017, the members of the US Congress responsible for reconciling the tax reform packages passed by the US House of Representatives and the US Senate filed their conference report. The tax package set forth in the conference report represents the most significant and extensive changes to the US Internal Revenue Code (IRC) since the Tax Reform Act of 1986.

The tax package, which includes not just statutory language, but explanations of the statutory language as well, is scheduled for votes in the House of Representatives and the Senate during the first part of the week of December 18. The legislation cannot be amended, other than isolated provisions being struck due to failure to comply with budget rules. Once H.R. 1, the "Tax Cuts and Jobs Act" (the Act), passes both houses, it will go to President Trump for his signature and enactment into law.

The Act is a compromise, adopting the House version of some provisions and the Senate version of other provisions. In a few cases, such as the changes to the mortgage interest deduction, the provision in the conference report is effectively a blend of competing House and Senate provisions. In many cases, the conference report adopts the House or Senate version of a provision, with changes, either because those changes were needed to obtain votes for the Act or because the changes were needed to provide revenue for changes needed to obtain votes for the Act. In a few cases, either for revenue reasons or because of needed votes, the Act omits a provision even though similar or identical provisions were passed by the House and Senate. Some of these dropped provisions are noted at the end of this summary.

Very generally, the Act more closely follows the Senate version than the House version. That is not surprising, since the Senate has a smaller Republican majority and more procedural restrictions than does the House.

Highlights of the Act

Individuals

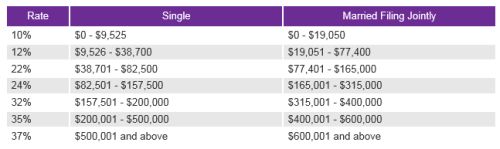

Rates. Like the Senate bill, the Act retains the current seven-tax-rate bracket structure, although several rates, including the top rate, would be lowered slightly.

The Act makes no change to capital gains or dividend tax rates although, for carried interests, the long-term capital gains tax rate will only apply to income attributable to a carried interest if the underlying investments are held for more than three years (rather than one year) . Existing alternative minimum tax (AMT) rates are retained, although the AMT exemption amounts and phase-outs are increased. The Act also retains the 3.8 percent tax on net investment income.

The new rates will have ripple effects throughout the IRC, changing the back-up withholding rate and other provisions tied to specific tax rates.

As in the House and Senate bills, the Act would index the rate brackets for inflation based on the "chained" Consumer Price Index (CPI), which will generally result in smaller inflation-adjusted increases in the rate brackets and other parts of the tax law that are indexed for inflation, such as the standard deduction.

Effective date: January 1, 2018, for calendar year

taxpayers.

Temporary or Permanent: The new rates and rate brackets

expire at the end of 2025. The change in inflation adjustments is

permanent.

Deductions, exclusions and exemptions. The Act increases the standard deduction to $24,000 for married filing jointly ($12,000 for single taxpayers) and the child tax credit to $2,000. It eliminates personal exemptions, although it includes a $500 credit for dependents other than qualifying children. It would eliminate most itemized deductions (and therefore the overall limitation on itemized deductions as well), except:

- The mortgage interest deduction would be limited for new homeowners by reducing the amount of qualified indebtedness to $750,000 and home equity loans would no longer be eligible for the mortgage interest deduction (the mortgage interest deduction for homeowners with existing mortgages will remain unchanged)

- The amount that could be deducted for state and local income taxes (or sales taxes in lieu of income taxes) and property taxes would be capped at $10,000 in total (property taxes on business assets or income property such as rental properties would remain deductible as a business expense)

- The deduction for charitable contributions would be retained and modified as proposed in the Senate bill (including an increase in the percentage limit for cash contributions to public charities)

- The deduction for investment interest expense would be retained

- The casualty loss deduction would be retained, but limited to those arising in declared disaster areas

- The moving expense deduction would be retained only for members of the Armed Forces

- The wagering loss deduction would be retained, but limited

- The deduction for medical expenses would be retained, with the floor decreased to 7.5% of adjusted gross income for 2017 and 2018.

"Excess Business Losses" would be limited for upper-income taxpayers. Such losses could be carried forward and treated as part of the taxpayer's net operating loss (NOL) carryforward in subsequent taxable years.

The Act expands the benefit of section 529 savings plans to include tax-free distributions (up to $10,000 per year per student) for elementary, high school, and certain homeschool expenses.

Effective date: Generally, January 1, 2018, for

calendar year taxpayers although certain provisions, such as the

denial of the deduction for alimony payments apply in general to

divorce or separation agreements executed in 2019. The conference

report specifically prevents taxpayers from prepaying 2018 state

and local taxes to avoid the new $10,000 limitation.

Temporary or Permanent: The changes to current law

generally expire at the end of 2025.

Individual Mandate. The "individual responsibility payment," enacted as part of the Affordable Care Act, would be reduced to zero, effective with respect to health coverage status for months beginning after December 31, 2018.

Businesses

Corporate Tax Rate. Despite both the House and Senate bills including a 20 percent corporate tax rate, the Act adopts a 21 percent rate for corporations. The corporate AMT is repealed, although AMT credits would continue to be available to offset regular tax liability and would be partly refundable in certain cases as well.

Effective date: Tax years beginning after December 31,

2017.

Temporary or Permanent: Permanent

Pass-Through Entity Deduction. The Act permits individuals, trusts, and estates to deduct 20 percent of their "qualified business income" from a partnership, S corporation or sole proprietorship (including a disregarded entity) as well as 20 percent of aggregate qualified real estate investment trust (REIT) dividends, qualified cooperative dividends, and qualified publicly traded partnership income. The provision includes many of the restrictions in the Senate bill regarding wages, income levels, etc., plus new ones. Generally, the 20 percent deduction cannot exceed the greater of (a) 50 percent of wages paid by the qualified business, or (b) 25 percent of wages paid and 2.5 percent of the cost of qualified property of the business. Further, the deduction is not available for taxpayers above the threshold described below for any "specified service business," which means any business:

- Involving the performance of services in the fields of health, law, accounting, actuarial science, performing arts, consulting, athletics, financial services, brokerage services or

- Where the principal asset of such trade or business is the reputation or skill of one or more of its employees or owners, or which involves the performance of services that consist of investing and investment management trading, or dealing in securities, partnership interests, or commodities.

In addition:

- The wages paid and specified service business limitations apply to taxpayers above a threshold amount of $315,000 for married filing jointly and $157,500 for individual filers. The limitations phase in above these amounts.

- Only domestic business income qualifies. Capital gain or loss items, dividends, interest and certain other investment-type items are excluded.

- Multiple qualified businesses are aggregated, and the deduction is allowed against the net qualified business income. Aggregate net losses are carried forward and reduce future deductions under this provision

The novelty and attraction of this provision mean that there will inevitably be complicated regulations and guidance, and substantial tax planning efforts, under this provision.

Effective date: Tax years beginning after December 31,

2017.

Temporary or Permanent: Permanent

Deductions, exclusions and exemptions. The Act provides full expensing of equipment and other qualified property (generally, the same property that is currently eligible for "bonus depreciation") acquired and placed into service between September 27, 2017, and January 1, 2023. The expensing provision, which applies to both new and used property, would be phased down so that qualified property placed into service between January 1, 2023, and December 31, 2026, would be subject to partial expensing. Special rules apply to aircraft and other "longer production period property" and to qualified film, television and live theatrical productions. In addition, the limits on IRC section 179 expensing for small businesses are increased as well. Other changes apply to the rules for luxury automobiles and personal use property, farm property, and real property.

The alternative depreciation period for residential rental property is shortened from 40 years to 30 years. All other current real property depreciation periods are retained.

For businesses with average gross receipts of more than $25 million, business interest expense is generally limited to the sum of business interest income and 30 percent of adjusted taxable income. Special rules apply to allow interest deductions for businesses use "floor plan" financing. For the 2018-2021 taxable years, "adjusted taxable income" does not take into account deductions for depreciation, amortization, or depletion. For businesses operating as partnerships, this limitation is applied at the partnership level. Real property development, construction, management, rental, and brokerage businesses (including investment vehicles such as low-income housing partnerships) may elect out of this limitation (at the cost of using the alternative depreciation system).

Certain deductions are repealed, including:

- IRC section 199 "manufacturing" deduction

- The deduction for entertainment expenses

- The deduction for employee fringe benefits

Other significant changes:

- The 70 percent dividends received deduction (DRD) and the 80 percent DRD are reduced to conform to the new 21 percent corporate tax rate

- NOLs arising in taxable years beginning after December 31, 2017, are limited to 80 percent of taxable income (determined without regard to the deduction), and most taxpayers would lose the ability to carry NOLs back

- Like-kind exchanges are generally limited to exchanges of real property that is not held primarily for sale

- Ability of small businesses to use cash accounting is expanded

- Fewer contributions to capital made after date of enactment qualify as tax-free

- No deduction would be permitted for expenses incurred after date of enactment for lobbying local or Indian tribal governments.

Deductions for Federal Deposit Insurance Corporation (FDIC) premiums are limited:

- Specified research or experimental expenditures paid or incurred in taxable years beginning after December 31, 2021, and attributable to research conducted within the US must be capitalized and amortized ratably over a five-year period, and specified research or experimental expenditures which are attributable to research that is conducted outside of the US must be capitalized and amortized ratably over a period of 15 years

- Accrual method taxpayers subject to the "all events test" for an item of gross income generally must recognize that income no later than the taxable year in which the income is taken into account as revenue in an applicable financial statement

- The category of payments treated as non-deductible fines or penalties is expanded for payments made after date of enactment

- No deduction is allowed for any settlement, payout, or attorney fees, paid or incurred after date of enactment, related to sexual harassment or sexual abuse if such payments are subject to a nondisclosure agreement

- The "orphan" drug credit is retained but limited

- The 20 percent rehabilitation credit for certified historic structures is also retained but taken ratably over five years (instead of immediately upon placement in service). The 10 percent credit for non-certified structures is repealed. The change is subject to a complicated phase-in rule

- The "technical termination" rule for partnerships is repealed.

Effective date: Generally (except as noted above), tax

years beginning and payments made or incurred, sales and exchanges,

dispositions, issuances, etc. after December 31, 2017.

Temporary or Permanent: Permanent

Impact on particular sectors

Significant changes are made to tax rules for:

- Insurance companies

- Retirement savings

- Partnerships

- The production and distribution of beer, wine, and distilled spirits

- Alaska Native Corporations.

Tax-Exempt Entities

Tax-exempt entities will be impacted by the Act both directly and indirectly. A 21 percent excise tax will be imposed on exempt organizations for "excess" executive compensation that exceeds $1 million annually for the five highest compensated employees, affecting both public and private organizations. A 1.4 percent excise tax will be imposed on the net investment income of the certain large endowments of private colleges and universities.

As for tax-exempt bonds, future advance refunding bonds would be taxable. Authority to issue future tax-credit bonds and direct-pay bonds is eliminated. Opportunity Zones with tax incentives would be created.

Other significant changes:

- Unrelated business taxable income rules are subject to new limitations

- Modification of certain charitable deductions

Effective date: Generally tax years beginning after

December 31, 2017.

Temporary or Permanent: Permanent

Estate and gift tax

The estate and gift tax exemption amount is doubled to $10 million and indexed for inflation.

Effective date: Effective for estates of decedents

dying and gifts made after December 31, 2017.

Temporary or Permanent: The changes to current law

generally expire at the end of 2025.

International tax reform

As in the House and Senate bills, the Act adopts a 100 percent exemption for dividends from foreign subsidiaries and a "deemed repatriation" provision.

- The 100 percent dividend exemption is limited to domestic "C" corporations (other than Regulated Investment Companies (RICs) or REITs) that hold a 10 percent or greater interest in a foreign corporation and have met a one year holding period requirement. The dividend exemption applies only to foreign-source dividends and does not apply to "hybrid" dividends that are deductible by the foreign corporation paying the dividend. The Act also includes special rules addressing tiers of foreign subsidiaries and dealing with the sale of stock of foreign subsidiaries to take into account the 100 percent dividend exemption. As in the Senate bill, the Act repeals the "active trade or business" exception in IRC section 367 for all transferors, whether corporations or not.

- Even though styled as a "transition" to the new

dividend exemption system, the deemed repatriation provision

applies to all US shareholders in a "specified foreign

corporation." Specified foreign corporations are generally

controlled foreign corporations (CFCs) and all other foreign

corporations (other than passive foreign investment companies) in

which a US person owns a 10 percent voting interest, although in

the case of a foreign corporation that is not a CFC, there must be

at least one US shareholder that is a domestic corporation for the

foreign corporation to be a specified foreign corporation.

- The deemed repatriation of "post-1986 earnings" is considered to occur at the end of the 2017 taxable year.

- The deemed repatriation rates for corporate shareholders are generally eight percent for illiquid assets and 15.5 percent for liquid assets. Individuals may use these rates by electing to be taxed as a corporation under IRC section 962.

- The "post-1986 earnings" subject to the deemed repatriation are limited to the period in which the foreign corporation qualified as a specified foreign corporation.

- Taxpayers subject to the deemed repatriation provision may elect to pay the tax in installments over eight years. The installment payments are back-loaded (eight percent of the tax in the first five years, 15 percent in year six, 20 percent in year seven and 25 percent in year eight). S corporations are permitted to defer payment of the tax even further until a triggering event occurs (such as a liquidation or sale of substantially all of its assets or a transfer of its stock).

Following the Senate bill, the Act introduces a new concept and tax, "global intangible low-taxed income" (GILTI), for US shareholders in CFCs. The calculations to determine a US shareholder's amount of GILTI are extremely complex.

- GILTI is generally the excess (if any) of the shareholder's net CFC "tested" income over the shareholder's net deemed tangible income return.

- The shareholder's net deemed tangible income return is the excess (if any) of 10 percent of the aggregate of its pro rata share of the qualified business asset investment (QBAI) of each CFC with respect to which it is a US shareholder reduced by certain interest expense.

- For any amount of GILTI included in the gross income of a domestic corporation, the domestic corporation is deemed to have paid foreign income taxes equal to 80 percent of the product of the corporation's inclusion percentage multiplied by the aggregate tested foreign income taxes paid or accrued, with respect to tested income, by each CFC with respect to which the domestic corporation is a US shareholder.

- The bite of the GILTI provision is further reduced for domestic C corporations: The Act provides domestic C corporations with a deduction for foreign-derived intangible income (FDII) and GILTI. As a result of the deduction, the effective tax rate on domestic C corporations on FDII is 13.125 percent and the effective US tax rate on GILTI is 10.5 percent for the 2018-2025 taxable years. Individuals and pass-through entities with owners that are individuals (such as S corporations) would not be eligible for the deduction and would pay income tax at ordinary income tax rates on their GILTI and FDII.

The Act includes another new concept and tax, a version of the Senate bill's "Base Erosion and Anti-Abuse Tax." This base erosion minimum tax effectively requires a domestic corporation that makes deductible payments to a foreign affiliate to pay the higher of (a) a tax equal to 10 percent (five percent in 2018 and 12.5 percent in tax years after 2025) of its income without any deduction for such otherwise deductible payments to its foreign affiliate ("base erosion payments") and (b) its regular corporate tax liability (reduced by the R&D tax credit in full and the low income housing tax credit and certain energy credits in part). The base erosion minimum tax applies to domestic corporations that have annual gross receipts in excess of $500 million and that have a "base erosion percentage" of three percent (two percent for certain financial entities, which are also subject to a base erosion minimum tax rate one percent higher than the regular rate) or higher for the taxable year. The "base erosion percentage" is the domestic corporation's total base erosion payments divided by its total deductible payments.

The Act includes several expansions of Subpart F, including a change to the constructive ownership rules for determining whether a foreign corporation is a CFC (retroactive to current taxable years), an expansion of the definition of "United States shareholder" to include any US person who owns 10 percent or more of the voting power or value of a foreign corporation, and elimination of the requirement that a corporation must be controlled for 30 days before subpart F inclusions apply.

The Act also:

- Expands the taxation of cross-border transfers of intellectual property

- Disallows deductions for payments involving hybrid transactions and hybrid entities

- Subjects expatriated entities to further adverse rules

- Restricts the insurance business exception in the passive foreign investment company rules

- Tightens the foreign tax credit rules by adding a new separate foreign tax credit limitation for foreign branch income and repealing the fair-market-value interest expense apportionment method, although the maximum overall domestic loss recapture is increased to 100 percent for pre-2018 losses

- Requires the source of income from sales of inventory to be determined solely on basis of production activities

- Subjects sales of interests in partnerships engaged in a trade or business in the US to US income tax, whether the seller is domestic or foreign. This provision is effective for sales, exchanges, and dispositions on or after November 27, 2017, although the new withholding requirement on sales or exchanges of partnership interests is effective for sales, exchanges, and dispositions after December 31, 2017.

Effective date: Generally (except as noted above) tax years beginning and sales and exchanges, distributions, transfers, etc. after December 31, 2017.

Temporary or Permanent: PermanentProvisions that were dropped

As is always the case in a conference report, some provisions in the House version of the bill or the Senate version of the bill were not included in the final bill. Noteworthy omissions include:

Individuals

- The House bill's phase-out of the 12 percent rate for upper-income taxpayers

- The House bill's repeal of the credit for the elderly and permanently disabled

- The House bill's repeal of the credit for plug-in electric drive motor vehicles

- The House bill's termination of the credit for interest on certain home mortgages

- The House bill's reform of the American opportunity tax credit and repeal of lifetime learning credit

- The House bill's repeal and limitation of existing education incentives, including repeal of the exclusion for qualified tuition reductions

- The House and Senate bills' increased taxation of gain on the sale of a principal residence

- The House bill's repeal of the exclusion for adoption assistance programs

- The House bill's repeal of the estate tax

- The House bill's repeal of the special rule for sale or exchange of patents

- The Senate bill's requirement that cost basis of specified securities be determined without regard to identification

- The House bill's repeal of the deduction for student loan interest

- The House bill's repeal of the exclusions and deductions related to Archer MSAs.

- Taxation of exempt organization income from the sale or licensing of the entity's name or logo

- Repeal of tax exemption for professional sports leagues

- Expansion and limitation of certain intermediate sanctions rules for exempt organizations

Businesses

- The House bill's provision limiting deductions in contingency fee cases

- The House bill's provision increasing carryover NOLs to account for the time value of money

- The House bill's repeal of many business tax credits, such as the new markets tax credit

- The House bill's repeal of many energy tax credits

- The House bill's repeal of private activity bonds

- The House bill's prohibition on issuance of tax-exempt bonds to finance professional sports stadiums.

- The House bill's permission for charitable organizations to make statements related to political campaigns

International

- The House and Senate bills' repeal of section 956 for corporations

- The Senate bill's incentives to move intangible property in CFCs to the United States

- The House and Senate bills' additional interest limitation for multinational groups

- The House and Senate bills' indexation of the Subpart F "de minimis" rule for inflation

- The House and Senate bills' permanent extension of the CFC look-through rule

- The House bill's 20 percent excise tax on payments to foreign affiliates.

US territories

- The House bill's extension of the deduction allowable with respect to income attributable to domestic production activities in Puerto Rico

- The House bill's extension of temporary increase in limit on cover over of rum excise taxes to Puerto Rico and the Virgin Islands

- The House bill's extension of American Samoa economic development credit

- The Senate bill's modification to source rules involving possessions.

Conclusion

The changes made by the Act are wide-ranging and, in many cases, almost immediately effective. Taxpayers will need to act quickly to understand these new rules and to comply with them. For many taxpayers, especially those who are owners of pass-through entities or that engage in cross-border activities, the Act will require them to revisit their structure, arrangements, and activities, often in fundamental ways.

Enactment is also merely the first step in the process. The speed with which the Act was drafted and its enactment so late in the year mean that the IRS will be spending much of 2018 developing rules, forms, and guidance to interpret and implement the new rules. So, at least when it comes to details, the Tax Cuts and Jobs Act still remains to be written.

For questions regarding trusts and estates, please contact Tom Opferman.

For questions regarding tax-exempt entities, please contact Tom Hyatt.

For questions regarding public policy matters, please contact John Russell.

For all other tax matters, please contact John Harrington, Tom Stephens, Marc Teitelbaum, Andrea Sharetta, Tim Santoli, JT Hutchens, or any other member of the Dentons US tax team.

Dentons is the world's first polycentric global law firm. A top 20 firm on the Acritas 2015 Global Elite Brand Index, the Firm is committed to challenging the status quo in delivering consistent and uncompromising quality and value in new and inventive ways. Driven to provide clients a competitive edge, and connected to the communities where its clients want to do business, Dentons knows that understanding local cultures is crucial to successfully completing a deal, resolving a dispute or solving a business challenge. Now the world's largest law firm, Dentons' global team builds agile, tailored solutions to meet the local, national and global needs of private and public clients of any size in more than 125 locations serving 50-plus countries. www.dentons.com.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.