I. Overview

On July 22, 2015, the Internal Revenue Service ("IRS") and the Treasury Department issued proposed regulations (REG-115452-14) under Section 707(a)(2)(A)1 of the Internal Revenue Code of 1986 (the "Code"), as amended to provide guidance with respect to the facts and circumstances under which an arrangement between a purported partner and its partnership would be treated as a disguised payment for services (the "Proposed Regulations"). The primary purpose of the Proposed Regulations is to distinguish between situations in which partnership interests granted in connection with a "management fee waiver" should be treated as taxable compensation for the performance of services, rather than as nontaxable "profits interests" in the partnership.2 In addition, in the preamble to the Proposed Regulations, the IRS and Treasury Department announced their intention to remove interests received in exchange for waived fees from an existing safe harbor, under which the receipt of certain interests are treated as "profits interests" that are not currently taxable.

The IRS added fee waiver guidance to its 2013-2014 priority guidance plan and, recently, government officials have been discussing their intention to issue regulations to address what they indicated are inappropriately aggressive fee waiver arrangements. Given the prevalence of management fee waivers in the asset management industry, private investment funds, their sponsors and investment managers and other industry participants have been anxiously awaiting the Proposed Regulations to understand the impact of the Proposed Regulations and the types of management fee waivers that would continue to be permissible.

The Proposed Regulations are proposed to be effective on the publication date of the final regulations. According to the preamble to the Proposed Regulations, in the case of an arrangement entered into before the effective date, the determination of whether the arrangement is a disguised payment for services will be made on the basis of Section 707 of the Code and the guidance provided in relevant legislative history. However, in the preamble to the Proposed Regulations, the IRS states that the Proposed Regulations generally reflect Congressional intent with respect to existing law, which suggests the IRS may use the Proposed Regulations as guidelines when auditing management fee waiver arrangements or potential disguised payments for services. In addition, the Proposed Regulations provide that a "modification" of a pre-existing arrangement after the effective date of finalized regulations, which includes the waiver of a fee after such date, would subject such arrangement to the Proposed Regulations as finalized.

II. Management Fee Waivers Generally

Management fee waivers generally entitle an investment manager to waive all or a portion of the management fee to which the investment manager would otherwise be entitled in exchange for an interest in the future net profits of the fund (which is treated as a partnership for U.S. tax purposes). Investment managers who also act as, or are affiliated with, the general partner of a fund may utilize management fee waivers to satisfy the general partner's required capital contributions to the fund through a "cashless" contribution. For example, rather than making a capital contribution to the fund equal to its share of a required capital call, the general partner will be deemed to contribute the amount of the waived management fee and receive an interest in the future net profits of the fund to match such deemed contribution.

There is significant variation in the structure of management fee waiver arrangements. In certain arrangements, the investment manager will waive the management fee before the management fee has been earned in exchange for an additional share of the fund's profits. Other arrangements involve the waiver of a management fee that has accrued, in whole or in part, in exchange for an additional interest in the fund's profits that are reasonably likely to occur during the life of the fund and/or an interest in future allocations of gross income or items of gain of the fund regardless of whether the fund is profitable.

Fund managers can benefit from these arrangements by being allocated long-term capital gain from the disposition of fund assets in which gain is taxable at a significantly lower rate than the waived fee and which otherwise would be treated as ordinary income subject to ordinary income rates, self-employment taxes and potentially additional taxes applicable to deferred compensation arrangements under Sections 409A or 457A of the Code. Management fee waivers also provides investment managers with the ability to defer income recognition until the investment manager receives an allocation of gain or income from the fund, which may occur years after the management fee would otherwise have been paid. However, under less aggressive structures, the favorable tax treatment for fund managers comes with the increased risk that the manager may not ultimately receive distributions in an amount equal to the fees that it would have otherwise been entitled to receive.

III. Summary of Proposed Regulations

The Proposed Regulations set forth rules for characterizing an arrangement between a purported partner and its partnership as a disguised payment for services. Whether an arrangement constitutes a payment for services depends on the facts and circumstances. Section 1.707-2(c) of the Proposed Regulations provides a non-exclusive list of six factors that may indicate an arrangement constitutes a payment for services. Drawing on the legislative history to Section 707 of the Code, the most important factor is a lack of "significant entrepreneurial risk" for the purported partner. An arrangement that lacks significant entrepreneurial risk constitutes a payment for services, while an arrangement that has significant entrepreneurial risk generally will not constitute a payment for services unless other factors establish otherwise.

The Proposed Regulations presume an arrangement lacks significant entrepreneurial risk if any of the following facts and circumstances apply (the "Risk Factors"): (i) capped allocations of partnership income where the cap is reasonably expected to apply; (ii) an allocation in which the service provider's share of income is reasonably certain; (iii) an allocation of gross income; (iv) an allocation that is predominantly fixed in amount, is reasonably determinable or is designed so that sufficient net profits are highly likely to be available to make the allocation to the service provider; or (v) an arrangement in which a service provider waives its right to receive payment for the future performance of services in a manner that is non-binding or fails to timely notify the partnership and its partners of the waiver and its terms.

The other five factors that may indicate that an arrangement constitutes a payment for services include: (i) the service provider holds a transitory partnership interest or holds a partnership interest for a short duration; (ii) the service provider receives an allocation and distribution in the same timeframe that a non-partner service provider would receive payment; (iii) the service provider becomes a partner primarily to obtain tax benefits; (iv) the value of the service provider's interest in continuing partnership profits is small compared to the allocation and distribution; and (v) the arrangement provides for different allocations or distributions for different services received, the services are provided by one person or by related persons and the terms of the allocations or distributions are subject to levels of entrepreneurial risk that vary significantly.

Whether an arrangement constitutes a payment for services is determined at the time the arrangement is entered into or modified. An arrangement treated as a payment for services is treated as a payment for services in all areas of the Code, and any income or deduction resulting from such treatment is taken into account in the taxable year required by the Code. However, many aspects of the recharacterization of a partnership interest as a fee for services are not addressed (e.g., the timing of the income inclusion). For example, the Proposed Regulations do not clarify whether a partnership interest received in connection with a fee waiver that is subsequently recharacterized as a payment for the performance of services would receive the benefit of deferring the income taxation of such payment. Even fee waiver arrangements that involve "cashless" capital contributions would seem vulnerable to current taxation based on the value of the interest received unless other circumstances apply (e.g., a substantial risk of forfeiture).

IV. Summary of the Examples in the Proposed Regulations

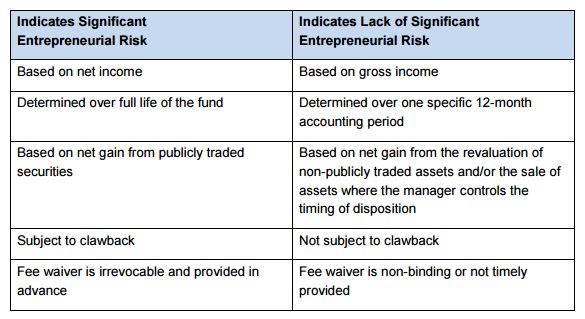

The Proposed Regulations include six examples to illustrate the factors discussed above. While the examples clearly highlight the government's focus on the potential lack of "significant entrepreneurial risk" in fee waiver arrangements, the examples do not provide comprehensive guidance regarding the meaning of the enumerated factors that lead to a presumption of a lack of "significant entrepreneurial risk." Based on the examples, unsurprisingly, the IRS is particularly concerned about fee waiver arrangements where the allocation is reasonably determinable or highly likely to be available, such as where the investment manager controls the timing of asset disposition and the valuation of non-publicly traded assets. The following chart summarizes some additional facts that the IRS considered in the examples:

Given certain of the examples' tendencies to assume the allocations are "highly likely" or "reasonably determinable," which amounts to concluding they lack significant entrepreneurial risk, it is difficult to draw too much definitive guidance from them because there are not enough facts to determine the meaning of "highly likely" and "reasonably determinable."

V. Safe Harbor

In the aftermath of Campbell v. Commissioner,3 Revenue Procedure 93-27 was issued to provide guidance on the treatment of the receipt of a "profits interest" for services provided to or for the benefit of a partnership.4 It provides that, if a person receives a "profits interest" (i.e., an interest in future profits and appreciation and not in existing capital) for the provision of services to or for the benefit of a partnership in a partner capacity or in anticipation of being a partner, the IRS will not treat the receipt of such interest as a taxable event for the partner or the partnership. This safe harbor does not apply if: (i) the profits interest relates to a substantially certain and predictable stream of income from partnership assets, such as income from high-quality debt securities or a high-quality net lease; (ii) within two years of receipt, the partner disposes of the profits interest; or (iii) the profits interest is a limited partnership interest in a "publicly traded partnership" within the meaning of Section 7704(b).

In the preamble to the Proposed Regulations, the IRS and Treasury Department announced their intention to narrow the scope of the safe harbor in Revenue Procedure 93-27. The safe harbor will not apply to management fee waiver arrangements in which an investment manager that provides services to a fund in exchange for a fee waives that fee in exchange for the issuance to an affiliate of the investment manager of an interest in future partnership profits calculated by reference to the amount of the waived management fees. The preamble notes that the safe harbor is inapplicable in such instance because (i) such transactions do not satisfy the requirement that receipt of a profits interest be for the provision of services to or for the benefit of the partnership in a partner capacity or in anticipation of being a partner, and (ii) the service provider would effectively have disposed of the partnership interest (through a constructive transfer to the related party) within two years of receipt. Accordingly, based on the guidance in the preamble, the IRS may contend that, even if a fee waiver arrangement by the investment manager has significant entrepreneurial risk, the receipt of an additional carried interest by a general partner (or other entity) that was not the actual service provider is a taxable event.

Furthermore, the IRS and the Treasury Department plan to issue a revenue procedure providing an additional exception to the safe harbor in Revenue Procedure 93-27. The new exception is expected to apply to a profits interest issued in conjunction with a partner foregoing payment of an amount that is substantially fixed for the performance of services.

The preamble also indicates that the IRS intends to: (i) amend provisions of existing regulations that are inconsistent with the Proposed Regulations, including as to the general treatment of certain amounts as guaranteed payments, and (ii) consider other related issues, including certain issues related to "targeted" capital accounts.

VI. Conclusion

Much can and will be said about the Proposed Regulations over the coming months as taxpayers and their advisors react to their proposals. Below, we set forth some preliminary observations:

- The issuance of the Proposed Regulations takes an important step in providing insight regarding the factors that the IRS and Treasury Department consider when analyzing management fee waivers and other arrangements between a purported partner and its partnership that, possibly, should be treated as disguised payments for services.

- While the IRS and the Treasury Department clearly are focused on arrangements that lack significant entrepreneurial risk, the Proposed Regulations do not provide sufficient clarity on what that means in the context of typical fund management fee waiver arrangements. For example:

-

- Risk Factors (i), (ii) and (iv) allude to profit allocations that are "reasonably" determinable or that have a "high likelihood." In assuming such characteristics, these Risk Factors do not provide clarity regarding the meaning of "a lack of significant entrepreneurial risk." Moreover the meaning of the various clauses of Risk Factor (iv), written in the disjunctive, is unclear.

- Similarly, the examples focus on extreme and unrealistic fact patterns, and they also do not provide facts to illustrate what is "reasonably determinable" or has a "high likelihood."

- The Proposed Regulations do not provide a "safe harbor" under which the IRS will not challenge a management fee waiver arrangement. Accordingly, taxpayers are left with a vague facts and circumstances test to determine whether arrangements with service providers should be characterized as compensatory.

- However, Risk Factors (iii) and (v) provide clear guidance that (1) fee waiver arrangements involving gross income allocations should be avoided and (2) fee waivers should be in writing, legally binding, irrevocable and clearly disclosed to the investors in the fund's offering documents.

In addition, the Proposed Regulations clearly provide that Revenue Procedure 93-27 does not apply in situations where the investment manager waives its management fee and an affiliate of the investment manager (i.e., the general partner) receives an interest in the future profits of the fund, the value of which approximates the amount of the waived fee. As a result, it is possible that the receipt of an additional carried interest by a general partner, in connection with an affiliated investment manager's fee waiver, could be taxable. We expect that the portion of the general partner's carried interest that is not issued in connection with the management fee waiver should continue to be treated as a "profits interest" that is not taxable on receipt under Revenue Procedure 93-27.

Footnotes

1 Section 707(a)(2)(A) provides that if a partner performs services for a partnership and receives a direct or indirect allocation and distribution, and if the performance of services together with the allocation and distribution are properly treated as a transaction occurring between the partnership and a partner acting other than in its capacity as a partner, then the transaction will be treated as occurring between the partnership and one who is not a partner.

2 While the focus of the Proposed Regulations is to address management fee waivers, the Proposed Regulations apply to any grant of a partnership interest potentially related to the performance of services.

3 943 F2d 815 (8th Cir. 1991). In Campbell, the Eighth Circuit Court held that a partner providing services to a partnership was not taxable on the receipt of a profits interest at the time of formation of the partnership because the partnership interest had no value at the time he received it due to its restricted transferability, subordinate rights to cash distributions and return of capital, and lack of management participation.

4 The IRS issued additional guidance in Revenue Procedure 2001-43 and in proposed Treasury Regulations and Notice 2005-43. Prop. Reg. § 1.721-1(b)(1) (2005); Prop. Reg. § 1.83-3(e) (2005).

Because of the generality of this update, the information provided herein may not be applicable in all situations and should not be acted upon without specific legal advice based on particular situations.

© Morrison & Foerster LLP. All rights reserved