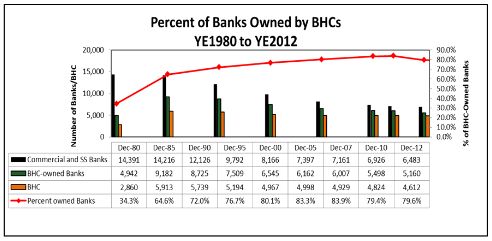

The last thirty years have witnessed a dramatic rise in bank adoption of the bank holding company ("BHC") structure. Inherent in this trend is an apparent accepted orthodoxy about the need of such structures from both a business and regulatory perspective. The percentage of U.S. banks owned by BHCs has more than doubled since 1980, from 34.3% to approximately 84% today.1

Federal banking agencies ("FBAs"), however, do not require banks to form a BHC.2 Thus, the uptick in BHC-owned banks has largely been driven by perceived legal, regulatory, and business advantages. Since 1980, the majority of banks presumably (1) identified significant advantages to forming a BHC that outweighed the increased costs of corporate governance and regulatory compliance and/or (2) saw their peers forming BHCs and generally accepted this industry trend as the orthodoxy of modern banking organization structure.

Despite the emergence of BHCs as the "must have" organizational structure for the banking industry, approximately 16% of U.S. banks have opted to remain outside of the BHC structure. This statistic suggests at the very least that, for certain banks, the perceived advantages of forming a BHC are not compelling. This rate of hold-outs suggests that the BHC structure's advantages do not always outweigh the structure's ever-increasing bank regulatory compliance and corporate governance costs, particularly as a result of the Dodd-Frank Wall Street Reform and Consumer Protection Act ("Dodd-Frank"). Notably, the hold-out banks are not limited to one particular size or business model. Instead, they range from small community banks with less than $10 billion in total assets,3 to mid-sized banks with $30 billion in total assets and a number of non-bank subsidiaries engaged in broker-dealer and investment advisory activities,4 and to large regional banks with total assets exceeding $50 billion.5This diversity calls into question the need for a BHC.

In our recent article, we trace how the perceived advantages of BHCs once held over banks have been steadily eroding, while the regulatory burdens imposed on BHCs have been significantly increasing, especially following the 2010 enactment of Dodd-Frank.6 Given the growing regulatory burden on BHCs in conjunction with the expanding range of activities that banks may engage in without them, the BHC structure may no longer be the most advantageous corporate structure for many banks, especially those engaged primarily in banking and certain financial services activities.

Need for Each Bank to Reevaluate Merits of BHC Structure

As a general matter, one of a corporation's primary objectives is to conduct its business activities to maximize corporate profit and shareholder gain.7 Thus, director leadership responsibilities include informed decision-making regarding corporate policies and strategic goals. From a fiduciary prospective, bank management bears a specific responsibility to periodically review its corporate and governance structure. In addition, the federal banking agencies have emphasized that "financial institutions are encouraged to 'periodically review their policies and procedures related to corporate governance ... matters.'"8 In this context, fiduciary duty requires management to periodically "evaluate which corporate governance policies and procedures are more appropriate [for an institution's] size, operations and resources."9

In this context, a corporate governance review should include an assessment of regulatory compliance and corporate governance costs and a consideration of what corporate structure is optimal for the entity to best maximize profitability, streamline regulatory burdens—consistent with the institution's business plans—and operate safely and soundly.10 Given the decreasing advantages and significantly increased disadvantages—primarily mounting compliance costs associated with BHCs—banks should evaluate the relative merits of a BHC structure.

Expansion of Bank Powers Decrease the Need for BHCs

Although BHCs may still engage in a wide range of activities, the gap between permissible BHC and permissible bank activities has, as a practical matter, substantially narrowed for most of the banking industry. Today, national banks and their operating subsidiaries are permitted to engage in a broad array of financial activities previously reserved for BHCs.11 The powers of state-chartered banks have likewise expanded as most states enacted "wildcard" statutes permitting their state chartered banks to engage in the same activities permissible for national banks.12 Banks can conduct, among other things, certain financial, investment and economic advisory services; provide transactional advice; and engage in various insurance and annuities activities as well as securities activities.13 Given the evolution and expansion of bank powers, many of the advantages of operating within the BHC structure have eroded.

Reduced Benefits of the BHC Structure

The waning benefits of the BHC structure are not limited to the reduced gap between authorized BHC and bank activities. Other traditional BHC benefits have also diminished or evaporated.

- Bank Subsidiaries—Historically, the BHC structure was the primary means of acquiring and holding multiple bank subsidiaries due to interstate banking prohibitions, but these interstate banking prohibitions have been eliminated.14

- Preferential Treatment of Debt—The previously preferential treatment of debt at the BHC level has largely evaporated. Prior to Dodd-Frank, the BHC structure facilitated double leverage where a BHC could engage in trust preferred securities ("TruPS") financing, which could be counted as capital at the BHC level and where the proceeds could be counted as Tier 1 capital at the bank level.15 This is no longer the case. The Collins Amendment to Dodd-Frank, along with the related Federal Reserve rules and policies, has largely eliminated TruPS and similar hybrid debt securities from being included in regulatory capital.16

- Director/Officer Liability—BHCs once had an advantage over banks with respect to director and officer liability. Banks once were restricted by the corporate governance provisions of the state of their headquarters, while BHCs had the flexibility to select their state of incorporation, allowing them to select states with more favorable indemnification and liability laws. But, in 1986, national banks were granted similar flexibility by the OCC,17 which allowed national banks to adopt corporate governance provisions in their bylaws from a number of jurisdictions, e.g., from the home state of the bank, BHC, Delaware, or Model Business Corporation Act.18

- Executive Compensation—Executive compensation and indemnification by all banks and BHC are now subject to compliance with the same statutory and FBA regulatory requirements.19 Additionally, Section 956 of the Dodd-Frank Act requires the federal banking/agencies to develop rules to "curb excessive compensation at financial services organizations,"20 which includes both BHCs and banks.21

Some Remaining Advantages

Notwithstanding the erosion of advantages and mounting regulatory burdens of the BHC structure, BHCs continue to offer certain key advantages.

- Minority Investments—Unlike a bank, a BHC may own up to 5% of the voting shares of any other company without prior regulatory approval.22

- FHCs' Expansive Powers—Furthermore, BHCs that qualify as financial holding companies ("FHCs") enjoy additional advantages, for FHCs may engage in activities that are "financial in nature" beyond what is allowable for banks,23 including securities underwriting and dealing, insurance underwriting, and merchant banking—activities largely undertaken only by the nation's largest banking organizations.24

Footnotes

[1] Bank Holding Companies and Financial Holding Companies, Partnership for Progress, (last visited Feb. 22, 2016).

[2] See id. (encouraging organizations to individually consider the advisability of forming a BHC and noting that the Federal Reserve is neutral on their creation).

[3] See, e.g., Bank Information of Comenity Bank, FDIC, (last visited Feb. 17, 2016) (follow "Financials" hyperlink) (indicating that Comenity Bank has less than $10 billion in total assets).

[4] See, e.g., Bank Information of Signature Bank, FDIC, (last visited Feb. 17, 2016) (follow "Financials" hyperlink) (indicating that Signature Bank has a little over $30 billion in total assets).

[5] See, e.g., Bank Information of First Republic Bank, FDIC, (last visited Feb. 17, 2016) (follow "Financials" hyperlink) (indicating that First National Bank has over $50 billion in total assets).

[6] Dafna Avraham et al., A Structural View of U.S. Bank Holding Companies, 18 Fed. Res. Bank N.Y. Econ. Pol'y Rev. 65, 67 (July 2012), ; see also 12 C.F.R § 225.84 (2015).

[7] Am. Bar Ass'n, Corporate Director's Guidebook, 56 The Bus. Lawyer 1517, 1578 (3d ed., Aug. 2001); The ClearingHouse, Guiding Principles for Enhancing Bank Organization's Corporate Governance: Exposure Draft for Public Comment 9 (Sept. 10, 2014); see also Am. Bankers Assn., Corporate Governance for Mutuals (2007); Am. Bankers Ass'n., The Board's Role in Strategic Planning (2004) ("ABA CORP. GOV.").

[8] ABA CORP. GOV. at 3.

[9] Id.

[10] See id. at 2, 8.

[11] See generally OCC, Compendium of Activities Permissible for a National Bank, (April 2012) ("OCC Compendium") listing a broad array of activities permissible for national banks and their subsidiaries).

[12] Christine E. Blair & Rose M. Kushmeider, Challenges to the Dual Banking System: The Funding of Bank Supervision, 18 FDIC Banking Rev. 1, 14 (2006) (discussing how state statutes have allowed state chartered banks to engage in all activities permissible for national banks.

[13] See generally OCC Compendium, supra note 11 (listing permissible activities for national banks).

[14] See Mehrsa Baradaran, Reconsidering the Separation of Banking and Commerce, 80 Geo. Wash L. Rev 385, 400 (2012) (indicating that, before the Riegle-Neal Interstate Banking Act, interstate bank prohibitions provided BHCs with a competitive advantage as the primary way to engage in banking in multiple states); Carl A. Sax & Marcus H. Sloan III, Legislative Note, The Bank Holding Company Act Amendments of 1970, 39 Geo. Wash. L. Rev. 1200, 1208 (1971).

[15] Alan Faircloth, ViewPoint: Spotlight: A Guide to Trust Preferred Securities, 27 Fin. Update 1 (2014),

[16] Id. (noting that TruPs no longer constitute Tier 1 capital for BHCs with greater than $15 billion in assets).

[17] 61 Fed. Reg. 4849, 4866 (Feb. 9, 1996).

[18] See 12 C.F.R. § 7.2000 (2015).

[19] See 12 U.S.C. § 1828(k) (2006 & Supp. 2011) (granting FDIC authority to prohibit or limit, by regulation or order, any golden parachute or indemnification payment); See 12 C.F.R. §§ 359.2, 359.3 (2012); see also 12 C.F.R. § 359.2 (2012).

[20] Francine McKenna, Dodd-Frank Rule to Curb Bank incentive Pay Likely Last to Finish Line, MarketWatch (July 16, 2015, 9:18 AM), Dodd-Frank, Pub. L. 111–203, § 956(e)(2), 124 Stat. 1906 (2010) (codified as 12 U.S.C. § 5641).

[21] Joint Press Release, Bd. of Governors of the Fed. Reserve Sys., Agencies Seek Comment on Proposed Rule on Incentive Compensation (Mar. 30, 2011), ("requir[ing] compensation practices at regulated financial institutions to be consistent with three principles—that compensation arrangements should appropriately risk and financial rewards, be compatible with effective controls and risk management, and be supported by strong corporate governance").

[22] Bank Holding Company Act, 12 U.S.C § 1843(c)(6) (2012).

[23] Id. § 1843.

[24] Id. § 1843(k)(4).

Originally published by Harvard Law School Forum on Corporate Governance and Financial Regulation and American University Business Law Review.

The content of this article does not constitute legal advice and should not be relied on in that way. Specific advice should be sought about your specific circumstances.