How can private debt offer investors an opportunity to positively contribute to a sustainable economy?

Executive summary

As we come closer to 2050, our collective shortcomings in financing the transition to a sustainable economy loom over us. Over $105 trillion USD in additional spending is required over the next 30 years to reach Net Zero, an increase of more than 60% of our current spending1. Immediate and tangible action is required to achieve this. As a result, investors' needs and obligations are evolving due to shifting preferences, regulatory demands, and a desire to capitalise on this market shift.

We believe private debt offers investors an excellent opportunity to meet these needs through financing investments positively contributing to a sustainable economy, encouraging markets to broadly focus on sustainable investments and offering an opportunity to directly finance opportunities with tangible impact while accessing returns superior to those found in public markets.

Introduction

At a time when the world is driving towards meeting Net Zero goals in line with the Paris Agreement, we believe it is increasingly possible to find solutions that intertwine strong financial outcomes with compelling sustainable investing and real-world impact. There has been a palpable rise in the quantity and size of funds with a sustainability focus, coupled with demand from all types of investors, who are becoming increasingly knowledgeable about the ways they can pursue sustainable investments and generate impact.

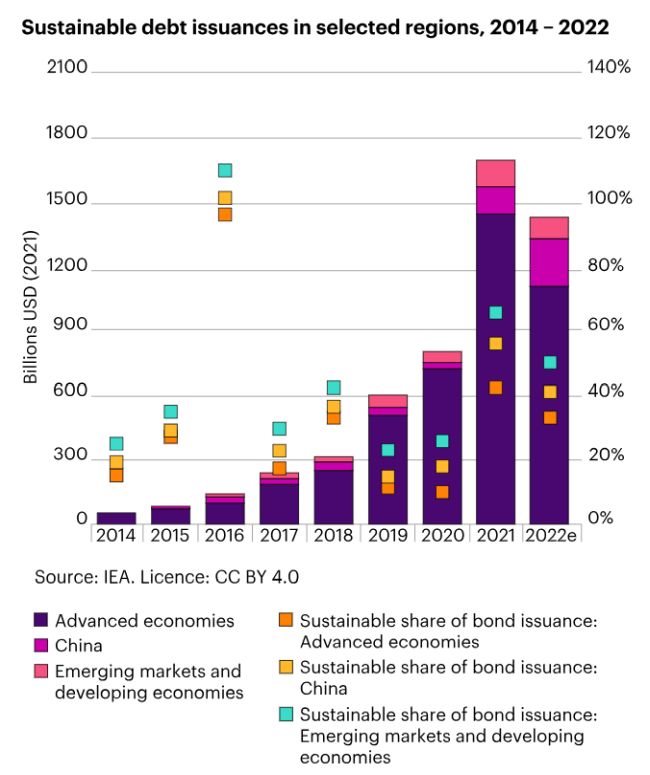

There has been a dramatic rise in sustainable debt issuance and there is significant demand for an increase in financing to drive the energy transition forward.

Sustainable debt issuances in selected regions, 2014 – 20222

We believe that private debt offers a compelling avenue to achieve this. This trend has been accelerated by the increasing popularity of private debt for borrowers as an alternative to public markets and investors embracing the higher returns due to illiquidity. Private debt solutions can be relevant for and are being used by DB, Insurance, Endowments, Foundations, Charities, and potentially Wealth and DC clients, making it a versatile solution. At WTW, we have engaged and will continue to engage with managers on implementing more sustainable investment processes and in finding strategies with tangible impact.

Lenders are better placed to drive positive change than many think

It may seem harder for private debt funds to generate impact as, unlike private equity, they do not have control over underlying assets. But companies refinance every 3–5 years, and so lenders may hold far more sway than many asset managers have traditionally thought (noting that competitive dynamics can and do have an effect). Thankfully, recognition of the need to do better in terms of sustainability is increasingly recognised and managers recognise that an asset with better sustainability characteristics should be less at risk of becoming a stranded asset, have a greater chance of being refinanced, and be a more attractive asset to sell. Managers have the capability to set ESG-linked terms in directly originated private debt deals, unlike traded public bonds on the secondary market, and hence can invest with intentionality and demonstrate impact.

Typically, investors do not need to forgo returns to generate impact, with some private debt infrastructure impact opportunities offering more attractive pricing than similarly rated liquid infrastructure assets, even allowing for the illiquidity premia afforded to private debt. This may seem surprising given the much-reported greenium seen in public markets3 but impact capital is still relatively new in the private debt space and commands a premium.

Private debt is also a suitable solution to demonstrate sustainability characteristics or impact that align with definitions of sustainability included in recent EU and draft UK regulations for investment firms, such as MiFID II in Europe and the UK Sustainable Disclosure Regulation. The private debt industry is acting and responding positively to this new regulation, with greater integration of sustainability considerations and a greater push for ideas with genuine impact.

Private debt's ability to generate impact is still a new concept and we recognise the need for collaborative efforts by investors and fund managers across different forms of financing to ensure widespread impact and fulfilment of sustainability objectives.

Better integrating sustainability into investment

At WTW, we have established ESG minimum expectations that we require all rated managers to meet or face rating re-evaluations. This helps ensure our investable universe meets a certain standard and enforces our belief that sustainability should be integrated into all managers' considerations, even if they do not run a sustainable or impact fund. These minimum expectations aim to satisfy client needs, which includes meeting regulations and demonstrating stewardship.

Minimum expectations

We strongly encourage all managers to adopt these practices. WTW will engage on these areas. In future years, failure to meet these expectations could impact our ratings and client flows, or lead to a downgrade.

TCFD reporting

Mandate Level

- Disclosure of appropriate climate-related metrics, e.g. Scope 1 + 2 carbon emissions

Firm Level

- A TCFD entity report setting out how climate-related matters are taken into account in managingor administering investments on behalf of clients and consumers

- There are four areas covered in the TCFD entity report: Governance, Strategy, Risk Management, Metrics, and Targets

ESG engagement reporting

- Mandate level engagement to be reported on annually

- The ICSWG engagement template may provide a useful reference

Exclusions reporting

- We expect managers to have a clear exclusions policy and accompanying processes in place

- Thermal coal

- Any company/group/tenant with revenues > 25% from mining or sale to third parties, and any companies/group/tenant with > 50% from coal power generation

- Oil/tar sands

- Any tenant company/group with revenues > 25% from tar sands extraction

Modern slavery and human trafficking policy and reporting/statement

We expect all managers to confirm and commit that the firm and its funds/products are not exposed to any incidence of modern slavery or human trafficking and to make an appropriate statement annually to this effect

We work with managers that do not meet our minimum standards to outline steps they can take to move towards a more sustainable process or, ideally, an impact strategy. Working closely with managers in this way can generate tangible long-term industry and system change and promote integrated sustainable considerations and impact generation in all funds. We also work with managers that are meeting our minimum standards on further process improvements so they can have conviction and generate impact.

There is no standardised definition of climate impact, but we believe that the SFDR framework is well-positioned as a baseline proxy, because of the links to ESG in its reporting requirements. It continues to evolve and incorporate new metrics as the impact space develops.

Private debt funding as a means to drive targeted impact

Climate impact has been a large part of our focus so far, but the potential areas of impact are much broader. We have found a variety of opportunities with compelling risk adjusted returns, particularly in today's environment where demand for private debt financing has increased dramatically.

Corporate asset class

Means of impact

- ESG linked ratchets: setting targets for borrowers to improve critical ESG items relevant to that business and industry

- Impact related industries: directly financing companies involved in the energy transition and other areas of impact (e.g. economic inclusivity)

Means of measuring

- SFDR

- Impact KPIs

Infrastructure asset class

Means of impact

- Renewable assets: financing green, renewable energy; circular economy industries (e.g. better, greener recycling)

Means of measuring

- IIGCC

- EUT

- SFDR

- Impact KPIs

Real estate asset class

Means of impact

- Green construction: financing the build of newer, sustainable buildings

- Energy efficiency: financing projects seeking to lower the carbon footprint of new and existing buildings

- Social / affordable housing: improving inclusivity in the residential market

Means of measuring

- BREEAM

- LEED

- SFDR

- Impact KPI

When setting up an impact fund, it is critical to agree on a clear and measurable definition of the desired impact. We show how this can be achieved through collaborative engagement in the case study below.

WTW Case Study

We worked with a private debt manager4 to create a strategy focused on impact generation through financing the low-carbon transition. We initially sought a strategy with 100% EU Taxonomy (EUT) alignment. However, we recognised that this could constrain the investment characteristics of the portfolio (due to concentration, deployment speed, and areas of impact not well covered by the EU Taxonomy), diluting the overarching requirement to maximise the impact the strategy could achieve and perhaps the other investment characteristics of the mandate.

EU Taxonomy

The EU Taxonomy offers a means of classifying investments as environmentally sustainable based on four criteria:

- the investment targets one of six listed climate and environmental objectives,

- the investment does no significant harm to the other five objectives,

- minimum safeguards are met, and

- the technical screening criteria are met.

The six objectives are:

- climate change mitigation,

- climate change adaptation,

- sustainable use and protection of water and marine resources,

- transition to a circular economy,

- pollution prevention and control, and

- protection and restoration of biodiversity and ecosystems.

This is not a comprehensive list of investments that may generate climate impact, but we believe it is sufficiently comprehensive to be useful.

Furthermore, the EU Commission regularly reviews the included (and disincluded) sectors and have put forward thoughtful arguments for the reason to include or not include certain sectors that may be deemed harmful to sustainable efforts. As investments that are EUT aligned are likely to fuel sustainable activity that otherwise might not have occurred, particularly as the stricter do no significant harm criteria must be applied, we are classifying EUT aligned assets as impact generating.

Instead, the manager agreed to three KPIs to ensure that the portfolio maintained its sustainable focus even without a 100% EUT alignment target. The first KPI was a reasonable yet ambitious EUT alignment based target, the second a fund-level temperature in line with the 2 degrees Paris Agreement, and the third a cap on fund-level carbon intensity. Fees were aligned to the goals of the mandate. Please note that the outcomes for this fund are not yet known as of October 2023 as it is in the early stages of its investment period.

This structure will be a template for our impact investing activities in future.

Risks of private debt investing

Private debt can be a great vessel for impact investing, however understanding the risks involved is important before pursuing investments. One key risk is that private debt is a highly illiquid investment, with assets not traded on a secondary market. Many lenders intend to hold assets to maturity, but if forced to sell before, there is the risk of selling and incurring losses. In addition, the private debt market is not regulated which means funds are not required to hold assets against potential losses and underwriting standards are not enforced in the same way as for traditional lenders. With less regulation, private debt is also less transparent both to regulators and markets, with no standardisation or market data to rely on. This may mean investors do not have full visibility into underlying holdings.

In order to help mitigate these risks, it is important to ensure that fund managers you work with have relevant experience, offer transparency which can be through regular and detailed reporting, and robust processes.

Conclusion

We believe private debt offers all investors a notable opportunity to meet their needs and obligations through delivering strong risk-adjusted returns while financing investments that contribute to a sustainable economy and demonstrate impact through additionality.

We (WTW) continue to spend substantial time and effort in furthering sustainability in the industry and searching for attractive impact ideas seeking compelling risk adjusted returns.

The direction of travel is very encouraging, with many managers increasingly integrating sustainable considerations into their investment processes and looking for impact opportunities, but best practice in the industry is fast evolving and our process will too.

We will continue to research which private debt managers are contributing to a sustainable economy and creating impact through their investments across all industries so that we can recommend these managers to impact-oriented investors.

Footnotes

1. The net-zero transition: What it would cost, what it could bring. Return to article undo

2. Sustainable debt issuances in selected regions, 2014-2022. Return to article undo

3. 32% of Green Bonds Achieved a Greenium in the First Half of 2023. Return to article undo

4. WTW began working with this private debt manager on April 2022. As such, there are no outcomes to report for this manager to date. Return to article undo

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.