The Transition Plan Taskforce Disclosure Framework (the "TPT Framework") published on 9 October 2023 has been publicly welcomed by the UK's Financial Conduct Authority (the "FCA"). For UK asset managers and portfolio managers, including private capital adviser-arrangers, this is a signal for likely change to FCA requirements on climate-related reporting.

What is the Transition Plan Taskforce Disclosure Framework?

The TPT Framework is intended to be the "gold standard for best practice transition plans" to support a range of organizations to identify, manage and report on their climate commitments with regards to the transition towards a low-carbon economy.

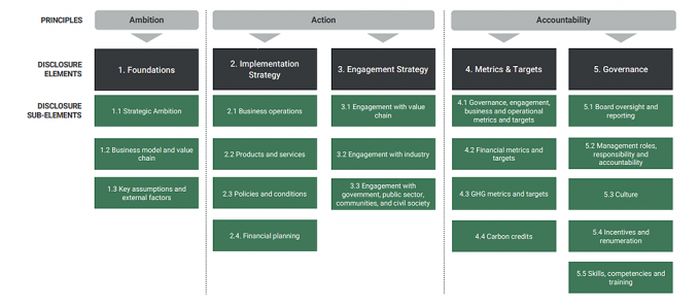

It provides a set of good practice recommendations to help entities across the economy make high‑quality, consistent and compatible transition plan disclosures. The TPT Framework's disclosure requirements are set under three principles for entities of "Ambition, Action, Accountability" as detailed in the diagram below:

Source: TPT-Summary-Recommendations.pdf (transitiontaskforce.net)

The TPT Framework builds on the International Sustainability

Standards Board's ("ISSB") global

non-financial reporting standards which were published earlier this

year for jurisdictions to consider adopting. The ISSB standards

require entities to disclose information about any climate-related

transition plans an organization has, including key assumptions

used in developing these plans and the dependencies on which the

plan relies. It is envisaged that the TPT Framework can be used to

support meeting these suggested ISSB disclosures. We discuss below

the expected relevance of both the TPT Framework and the ISSB

standards for asset managers (and other entities).

Why is this of interest?

The UK's Greening Finance Roadmap, published in 2021, set out commitments to introduce new, and strengthen existing, sustainability reporting requirements for a broad range of companies, including requiring the publication of climate transition plans. This has taken place so far through reporting requirements being placed on a range of entities, including those in financial services, based on the Taskforce for Climate-related Disclosures framework ("TCFD").

For UK‑regulated asset managers (including private capital adviser-arrangers) and asset owners with more than £5 billion of assets under management/ownership ("In‑Scope Firms") there is a requirement to make such TCFD reports in the FCA's ESG Sourcebook. With regards to transition plans, the ESG Sourcebook sets out a requirement for In-Scope Firms to "take reasonable steps" to follow the TCFD guidance, including publication of organizations' plans for transitioning to a low-carbon economy. The FCA provides further guidance in its ESG Sourcebook that where an In-Scope Firm is based in a jurisdiction which has made a net zero commitment, such as the UK, the In-Scope Firm is encouraged to assess the extent to which it has considered that commitment in developing and disclosing its transition plan. However, the reporting requirements stop short of mandating that In-Scope Firms have a transition plan in place and, if they do have one, what that plan should contain, which has been partly because the expectations of what a transition plan should cover have been fluid.

With the development of the TPT Framework, there are much clearer expectations of what a transition plan should contain and how commitments should be structured. The FCA has publicly welcomed its publication, and the TPT Framework itself signposts that "regulation is coming" with a direct reference to the FCA. This development runs alongside the UK currently undergoing an official assessment, before an expected endorsement and adoption, of the ISSB standards which, as set out above, are linked to the TPT Framework in that they require organizations to publish any climate-related transition plans they have.

It seems, as with the staggered rollout of TCFD reporting, that listed companies will be the first of any future compliance with the TPT Framework and ISSB standards, based on the documents released by the TPT. However, overall, the indicators are clear that the regulatory landscape on climate-related reporting for FCA-regulated firms, including asset managers, is on course for change in coming years. The momentum is in the direction of adoption of ISSB standards that require disclosure of climate transition plans with the TPT Framework guiding companies on how to formulate those plans.

What can UK asset managers do now?

The TPT Framework advises firms to ensure that transition plans are not viewed as merely a compliance exercise but that they form a critical component of a firm's business – helping to explain to clients, shareholders and investors their contribution to the transition to net zero.

For all asset managers, but particularly those in scope of the current ESG Sourcebook, we would recommend early review of the TPT Framework either to carry out a:

- gap analysis of existing transition plans against the TPT Framework; or

- a readiness assessment to meet the requirements where there is no current transition plan.

Such actions can be carried out with reference to what the TPT describes as "deep dive" guidance for asset managers which will be published next month in November 2023. Getting ahead will be important – obtaining the data and metrics to support any transition plans may pose some challenges, and robust disclosures will be even more critical with the imminent introduction of the FCA's anti-greenwashing rule for UK asset managers via their Sustainability Disclosure Requirements. For more information on some of the EU and UK legal and regulatory changes on the horizon in the area of sustainable finance, please see our recent note published here.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.