As India's financial sector addresses its climate risks, it must consider the vulnerabilities of its small borrowers, offering valuable lessons for emerging economies on building just transitions.

The notion that economic growth necessarily leads to prosperity is increasingly being questioned.1 Amid rising environmental degradation, ecological breakdown, and widening inequality there is growing consensus that economies – and the businesses that drive them – need a critical reexamination of their objectives and outcomes.

The concept of double materiality has taken root in this institutional environment; it asks that firms factor and disclose not just development and environmental risks to their businesses, but how their actions (including ones that are sustainability-led) impact the wider society, environment, and the economy.2

As climate-linked impacts become more frequent and pervasive, such considerations are gradually being adopted by "just transition"3 frameworks across economies and sectors. And yet, we argue, there is some way to go before the construct of "just" is widened, particularly by financial actors, to encompass physical climate risks and community resilience more concretely in the Global South. A case in point is the conceptualization and governance of climate-related financial risks (CRFR) in an emerging market like India.

CRFR was conceived by the financial community in 2015 to highlight how climate change – both physical risks as well as stranded carbon assets produced by transitioning to a low carbon economy – could disrupt the global economy and impact financial stability.4 CRFR has paved the way for multi-stakeholder, industry-led deliberations culminating in the creation of key formal bodies such as the Task Force for Climate-related Financial Disclosures or TCFD.5 Since their release in 2017, recommendations by the TCFD have been widely endorsed and adopted by corporates, governments, and financial institutions across the globe. These recommendations are centered around the idea that climate change is a market externality and the pricing and disclosure of climate risks by individual firms can restore market discipline.6

In India, the Reserve Bank of India (RBI), the country's central bank, has been at the forefront of conversations on CRFR. RBI joined the Network of Central Banks and Supervisors for Greening the Financial System (NGFS) some years ago and much of its narrative on CRFR builds on knowledge produced in such transnational settings. A review of RBI's policy literature on CRFR indicates that climate-related financial risks in India have been constructed as risks to the country's financial stability and must be managed as such.7

This micro-prudential approach to managing financial risks, however, requires a closer look at India's interventionist policy context which entails mandated lending to sectors and communities that may not have easy access to capital in a market-led economy. Two policies, for instance, have historically co-opted the banking sector to meet India's poverty alleviation and stabilization agendas: the country's financial inclusion program8 and the priority sector lending scheme (PSL).9 Under the PSL scheme, domestic commercial banks are mandated to allocate 40 percent of their net bank credit to priority sectors such as agriculture, micro enterprises, education, housing etc.10 PSL also includes a sub-category called weaker sections which constitutes lending to some of India's most marginalized caste, class, and communal groups.

For banks, a higher 'probability-of-default' is seen as a credit risk.

Recent (albeit scant) literature11 from industrialized economies indicates that borrowers are more likely to default on loans when faced with losses in assets and resources because of extreme weather events. For banks, a higher 'probability-of-default' is seen as a credit risk.12 Such credit and liquidity risks to financial institutions can travel up the financial chain, negatively affecting financial portfolios and collectively impacting the economy. There are no qualitative studies, to our knowledge, that closely examine the ways in which financial actors in the emerging economies construct and regulate such climate risks, and how these discursive and material outcomes travel through the financial value chain affecting lending mandates to socio-economically vulnerable communities.

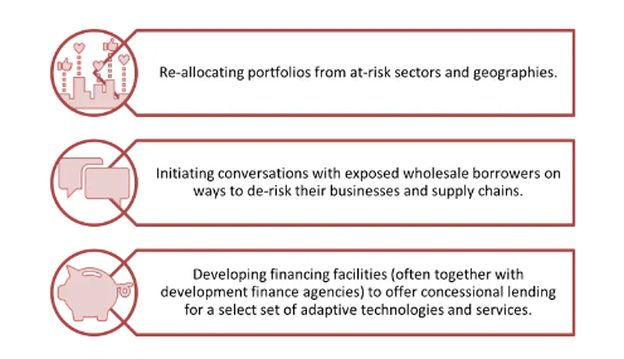

Practitioners working with financial institutions on their climate risks anecdotally note that banks and regulatory agencies have envisioned three broad routes to govern physical risks to their portfolios13:

Three broad routes banks & regulatory institutions envision on governing physical climate risks to their portfolios.

These approaches likely miss the mark in factoring lending processes in countries like India where a sizeable portion of banks' mainstream retail lending portfolios can include borrowers that are already financially precarious.14 The social and economic precarity of these borrowers make them particularly vulnerable to climate risks.

As acute and chronic climate events escalate in frequency and severity in South Asia, India faces a pressing issue: how its banks and regulators construct and tackle climate-related financial risks, especially when socio-economically vulnerable borrowers are involved. There is a need to ensure that our transition to a greener economy doesn't leave these vulnerable groups at further risk.

There is a need to ensure that our transition to a greener economy doesn't leave these vulnerable groups at further risk.

"Just transition frameworks" have focused on equitable greening of the economy. Recently, these frameworks have evolved to consider not just low carbon transitions but also ensuring climate resilience. This broader conceptualization is more normative in scope, and is meant to ensure, among other things, that private sector adaptation practices and risk management decisions do not reinforce vulnerability and maladaptation among at-risk communities.15

The social and economic precarity of these borrowers make them particularly vulnerable to climate risks.

The WTW Research Network (WRN) acknowledges this challenge. Collaborating with researchers from the London School of Economics and Political Science (LSE), the WRN seeks deeper insights into this issue. This qualitative research is poised to reveal the perspectives of both financial institutions and marginalized borrowers, providing conceptual and policy-relevant empirical insights. The goal is not only to delve into the existing landscape but also refine how "just transition frameworks" operate. Ultimately, the aim of the research is to guide the better disclosure and management of climate risks while shedding light on the financial practices and precarities of vulnerable communities in emerging economies.

Footnotes

1. RSA Shorts. 2014. Kate Raworth on Growth

2. Täger, M., 2021.'Double materiality': what is it and why does it matter?

3. UNDP, 2022. What is just transition? And why is it important?

4. Carney, M., 2015. Breaking the tragedy of the horizon - climate change and financial stability. London, Bank of England.

5. TCFD, 2017. Recommendations of the Task Force on Climate-related Financial Disclosures

6. Chenet, H., Ryan-Collins, J. & van Lerven, F., 2021. Finance, climate-change and radical uncertainty: Towards a precautionary approach to financial policy. Ecological Economics, Volume 183.

7. RBI, 2022. Discussion Paper on Climate Risk and Sustainable Finance.

8. Department of Financial Services, Government of India. 2023. Pradhan Mantri Jan Dhan Yojana

9. RBI, 2022. Master Directions – Priority Sector Lending (PSL) – Targets and Classification.

10. For private commercial banks the target is 32%

11. Noth, F. and Schüwer, U, 2018. Natural Disaster and Bank Stability: Evidence from the U.S. Financial System. SSRN

12. Bell, F. and van Vuuren, G, 2022. The impact of climate risk on corporate credit risk, Cogent Economics & Finance, 10:1.

13. Meisenzahl, R, 2023. How Climate Change Shapes Bank Lending: Evidence from Portfolio Reallocation. SSRN

14. Islam, E. & Singh, M., 2022. Information on Hot Stuff: Do Lenders Pay Attention To Climate Risk?. SSRN.

15. Kuhl, L., 2021. Engaging with climate adaptation in transition studies. Environmental Innovation and Societal Transitions, Volume 41, pp. 60-63.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.