FINMA published its new FINMA Guidance 08/2023 "Staking" clarifying the regulatory requirements for providing custody staking services in Switzerland in connection with validation services in proof-of-stake (PoS) protocols. This creates full legal certainty for such services, which brings Switzerland at the forefront in crypto regulations.

FINMA regards staking as the process of blocking native crypto assets at the staking address of a validator node in order to participate in a blockchain validation process based on a proof-of-stake (PoS) consensus mechanism. Participants earn rewards for staking crypto assets. Some blockchains delay the unlocking of staked crypto assets after the user or custodian triggered the unstaking process (Unstaking Period). Further, some blockchains "burn" part or all of the staked assets if the validator behaves improperly (Slashing)

FINMA communicated in Summer 2023 at its own Fintech Roundtable as well as on a seminar that it assumes crypto-based assets staked in PoS protocols for providing validation services not being kept available at all times in view of the Slashing risk and the Unstaking Period.

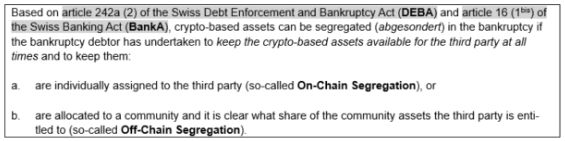

Based on article 242a (2) of the Swiss Debt Enforcement and Bankruptcy Act (DEBA) and article 16 (1bis) of the Swiss Banking Act (BankA), crypto-based assets can be segregated (abgesondert) in the bankruptcy if the bankruptcy debtor has undertaken to keep the crypto-based assets available for the third party at all times and to keep them:

- are individually assigned to the third party (so-called On-Chain Segregation), or

- are allocated to a community and it is clear what share of the community assets the third party is entitled to (so-called Off-Chain Segregation).

After various interactions and discussions with the industry and supervised entities, FINMA published now a distinguished approach in its new FINMA Guidance 08/2023 "Staking", which is internationally unique and brings the Swiss crypto space internationally at the forefront. Therein, FINMA acknowledges that articles 242a (2) DEBA and 16 (1bis) BankA have been drafted historically for pure custody-services and therefore are not automatically also applicable mutatis mutandis to staking services in PoS-protocols. At least, there is no legal certainty about "kept available at all time" and it can be interpreted differently until there will be clarification by new legislation, a court decision or international developments.

After various interactions and discussions with the industry and supervised entities, FINMA published now a distinguished approach in its new FINMA Guidance 08/2023 "Staking", which is internationally unique and brings the Swiss crypto space internationally at the forefront. Therein, FINMA acknowledges that articles 242a (2) DEBA and 16 (1bis) BankA have been drafted historically for pure custody-services and therefore are not automatically also applicable mutatis mutandis to staking services in PoS-protocols. At least, there is no legal certainty about "kept available at all time" and it can be interpreted differently until there will be clarification by new legislation, a court decision or international developments.

FINMA's own interpretation for "kept available at all time" in connection with staking services in PoS-protocols for providing validation services – which is not applicable to pure custody services – is as follows:

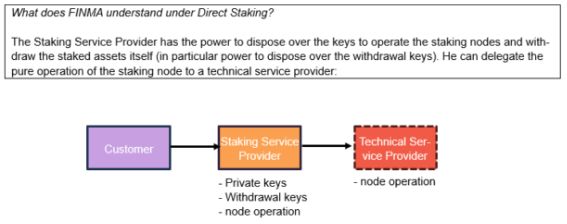

1. Direct Staking Structures

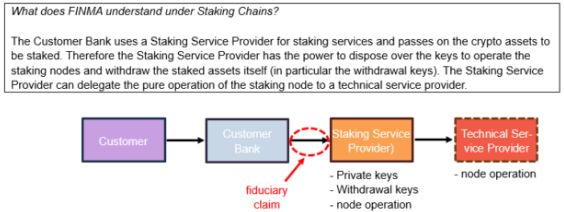

2. Staking Chains with Customer Bank and 2nd Bank

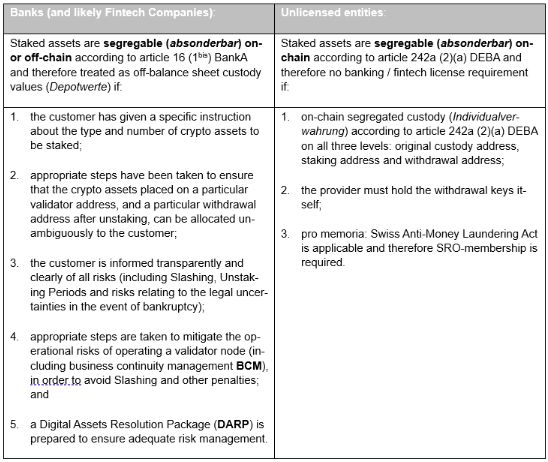

According to FINMA, Staking Chains can only be applied between licensed institutions (and presumably companies with a fintech-license) and Staking Service Providers subject to prudential supervision with a good credit standing. The Staking Service Provider must hold the withdrawal keys itself, which limits the staking chain length. Further, on-/off-chain segregation and off-balance sheet treatment according to article 16 (1bis) BankA is not possible for the Customer Bank.

However, the Customer Bank can structure the transfer of customer assets for staking to the Staking Service Provider as a fiduciary claim in its own name but on the accounts of the customer (Treuhandforderung) in accordance with the directive of Swiss Banking on fiduciary investments (Richtlinie betreffend Treuhandanlagen) so that it will be segregable (aussonderbar) and treated as off-balance sheet custody value (Depotwert) according to art. 16 (2) BankA.

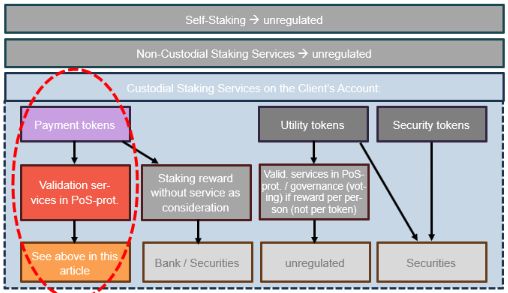

3. Where Does this new FINMA-Regulation Fit In?

In the past, FINMA has developed various unpublished practice not only about staking services on PoS-protocols with validation services, but also on other staking types. In a much simplified and only indicative way, this looks as follows:

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.