On 23 October 2023, the Australian Accounting Standards Board (AASB) released Exposure Draft ED SR1 Australian Sustainability Reporting Standards – Disclosure of Climate-related Financial Information that is proposed to apply to the climate-related financial disclosures of Australian reporting entities.

The Exposure Draft includes three standards that are closely aligned with the International Sustainability Standards Board's IFRS S1 and IFRS S2, and build on Treasury's second consultation paper released in June 2023 (see our earlier insights here).

Consultation is open until 1 March 2024.

Snapshot of proposals in the Exposure Draft

What are the proposed Standards?

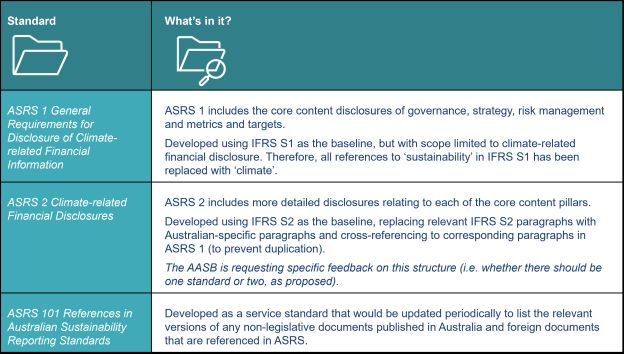

The Exposure Draft includes three draft Australian Sustainability Reporting Standards (ASRS):

So, what's changed?

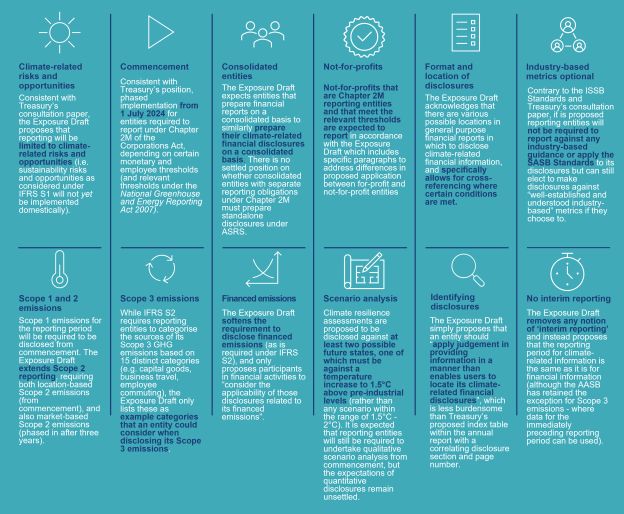

While the Exposure Draft is generally aligned with the ISSB Standards, we unpack some of the key changes proposed by the AASB below:

- Consolidated entities – Entities that prepare financial reports on a consolidated basis will be expected to similarly prepare their climate-related financial disclosures on a consolidated basis. However, the Exposure Draft does not address whether entities in a consolidated group with separate reporting obligations under Chapter 2M of the Corporations Act must prepare standalone disclosures under ASRS or can rely on the disclosures prepared by another group entity.

- Industry-based metrics not compulsory – The AASB has proposed that disclosures against relevant industry-based metrics and SASB Standards, as required under the ISSB Standards, should not be incorporated into Australia's domestic regime. The Exposure Draft notes that the SASB Standards are not representative of the Australian or global market (i.e. are "US-centric") and that the ISSB's consultation period was too short for stakeholders to appropriately consider the proposals or for the AASB to appropriately apply its own due process. However, reporting entities can still voluntarily choose to disclose against "well-established and understood industry-based" metrics if they choose to.

- Emissions (Scope 1, 2 and 3) –

- As expected, Scope 1 emissions for the reporting period will be required to be disclosed from commencement.

- Scope 2 reporting will be expanded to require both location-based Scope 2 emissions (from commencement), and also market-based Scope 2 emissions (phased in after three years of reporting).

- The AASB has retained Treasury's proposed exception where data for the immediately preceding reporting period can be used for Scope 3 disclosures and is also more lenient in reframing the 15 categories of Scope 3 emissions included in IFRS S2 as examples rather than mandated criteria against which an entity must report.

- Reporting entities will need to apply the methodologies set out in the National Greenhouse and Energy Reporting (NGER) Act 2007 (Cth) (unless impracticable), using Australian-specific data sources and factors for the estimation of GHG emissions.

- Financial activities and superannuation entities - The Exposure Draft has relaxed the requirement for asset managers, banks and insurers to disclose their financed emissions (as will be required under IFRS S2), and instead, proposes that those entities "consider the applicability of those disclosures related to its financed emissions". The AASB has also explicitly asked for feedback from superannuation entities on whether there are circumstances specific to the industry that would prohibit compliance with the regime (or result in undue cost or effort).

- Not-for-profit entities – The Exposure Draft proposes to extend the ASRS to not-for-profit entities that meet certain monetary and employee thresholds, and are otherwise required to report under Chapter 2M of the Corporations Act or that are registered as a "controlling corporation" reporting under the NGER Act. While this will not impact charities registered with the ACNC, we anticipate this will primarily impact large not-for-profit industry groups and organisations. The Exposure Draft specifically requests feedback from these groups.

Next steps

The Exposure Draft identifies three ways in which stakeholders can provide feedback by 1 March 2024:

- submit a comment letter on the AASB website;

- complete an online survey; or

- attend a roundtable discussion.

How can we help?

Given the lengthy consultation process and the intention for the Australian regime to commence from 1 July 2024, it is unlikely that 'Group 1' reporting entities will have a significant window for preparation between the finalised Australian regime and the start of the reporting window.

With this in mind, we are helping clients to assess the extent of uplift required ahead of time, including by conducting a 'gap analysis' between their current processes and disclosures and the expected future state. The review outputs can then form the basis of a bespoke roadmap to compliance in FY25 (and beyond...).

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.