Answer ... (a) What taxes are levied and what are the applicable rates?

Tax on investment income is based on how the investments are owned. For example, assets may be owned by an individual, a company or a trust structure.

For investments owned in a personal capacity, the investment income is added to the individual’s overall income, including employment income, and taxed at the marginal income tax rates.

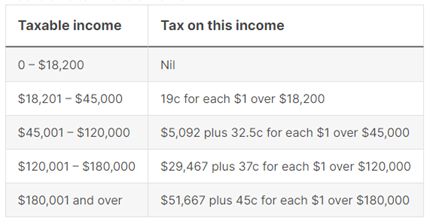

The marginal income tax rate increases according to the level of income earned. For the 2023–2024 financial year, the marginal income tax rates are as follows:

For the 2024–2025 financial year, the proposed changes to marginal income tax rates are as follows:

- Reduce the 19% tax rate to 16%;

- Reduce the 32.5% tax rate to 30%;

- Increase the threshold above which the 37% tax rate applies from A$120,000 to A$135,000; and

- Increase the threshold above which the 45% tax rate applies from A$180,000 to A$190,000.

Any income generated by a company is taxed at a marginal rate of 30%; and for trusts, any income accumulated (not distributed to beneficiaries) is taxed at a marginal rate of 45%.

(b) How is the taxable base determined?

The taxable base of investment income is calculated by classifying the investment income and deducting any related expenses incurred to earn that income.

(c) What are the relevant tax return requirements?

In the case of investment income for assets owned by an individual in his or her personal capacity, the individual must allocate such income to his or her individual tax return. An Australian tax resident must file an income tax return where his or her gross income exceeds the tax-free threshold of A$18,200. A non-resident earning more than A$1 of Australian-sourced income must file a tax return. There is no joint assessment or joint filing in Australia.

The tax return is due for filing by the following 31 October, unless an extension is available.

Once a tax return is lodged, the ATO will issue an income tax assessment of the taxable income/tax loss and tax payable (if any) to the individual based on the income tax return. If there is a tax liability, it is usually payable by May before the commencement of the next financial year.

A corporation – which includes the parent company of a tax consolidated group – can lodge a tax return under a self-assessment system that allows the ATO to rely on the information stated on the return. However, the ATO conducts audits to ensure that corporations are compliant with their tax requirements. If a corporation has doubts as to its tax liability regarding a specific item, it can request the ATO to consider the matter and issue a binding private ruling.

Generally, the tax return for a corporation must be filed with the ATO by 15 January or such later date as the ATO allows. Additional time may apply where the tax return is filed by a registered tax agent.

(d) What exemptions, deductions and other forms of relief are available?

As with a person’s income, in Australia, the first A$18,200 of income earned is considered tax free. Every A$1 earned over this threshold is taxable. There are certain deductions and reliefs available, such as for:

- income from rental properties – only income earned after the deduction of costs and expenses for operating the rental property is taxed;

- other expenses, such as the costs of managing one’s tax affairs; and

- dividend and other investment income.

Further deductions and relief are available for corporations, such as:

- depreciation and depletion for the decline in value held by the taxable entity;

- start-up expenses such as incorporation costs;

- interest expenses;

- bad or forgiven debts; and

- charitable contributions.

Losses can also be carried forward indefinitely, subject to certain compliance requirements.